Pic: Via Getty

Ride the Cycles: Where does your favourite ASX lithium project sit on the cost curve?

Mining

Pic: Via Getty

Mining

According to OG battery metals pricing agency Benchmark Mineral Intelligence, average prices for lithium as of January 11 were:

These prices are down +80% over the past year. At this point in the cycle only the best mines make money.

“If you are at the low end of the cost curve, all is good,” says Joe Lowry, one of the world’s foremost lithium market experts.

He is talking about operational expenditure (or OPEX), the ongoing costs associated with operating a mine.

OPEX includes both direct and indirect costs related to the day to day running of the business; mining, processing, and selling the ore.

If this number is a lot lower than the price a miner is getting for its metal, “all is good”, as Lowry says.

If not, a miner is probably losing money. Longer term, this could lead to expensive shutdowns, cap raises done at a deep discount, or bankruptcy.

Below are some emerging lithium project developers and their expected OPEX profiles.

Only use these numbers as a starting point and do your own research.

Mining project studies, even the most detailed ones, are historically ambitious.

Recoveries and product grades are often far lower than what miners originally assume, and full ramp up takes longer than expected.

A recent example is Core Lithium (ASX:CXO), which put the Finniss hard rock mine into mothballs less than a year after its maiden shipment.

A stage 1 definitive feasibility study – the most advanced of project studies — released July 2021 predicted cash operating costs of US$364/t, and all in sustaining costs of US$441/t.

In the September quarter last year CXO’s cash cost was US$1270/t.

Cash costs include mining and processing, but often do not include things like sustaining capital, exploration, corporate overhead, or any other costs not related to production.

All In Sustaining Cost (AISC) is more representative of a company’s financial health. All In Cost (AIC) is even better.

However, unlike gold companies, lithium stocks do not consistently use the same measures. Investors must join the dots.

There are other things to consider. Producers would receive less than the Benchmark prices mentioned above if they sell:

With that in mind, can your favourite lithium stock ride the cycles?

Geothermal lithium play Vulcan (ASX:VUL) says its Phase 1 24,000tpa lithium hydroxide operation would boast OPEX of €4,022/t (A$6667/t), making it “one of the lowest on the industry cost curve”.

This is due to smart use of waste heat to drive the process, VUL says.

“Combined with offtake agreements with tier one customers, [this] supports stability during payback period, and protection from lithium price fluctuations.”

European Lithium’s (ASX:EUR) small 8800tpa Wolfsberg hard rock-hydroxide project in Austria has OPEX of US$17,016/t, according to a 2023 DFS.

The company is currently trying to get its NASDAQ listing via special purpose acquisition vehicle (SPAC) over the line.

Piedmont’s (ASX:PLL) 30,000tpa Tennessee lithium project would purchase spod at market rates from 3rd parties, mostly Sayona’s (ASX:SYA) NAL operation and Atlantic Lithium’s (ASX:A11) Ewoyaa start-up.

It expects OPEX of US$14,600/t based on conversion costs of US$2952/t, plus spod purchase costs of $10,700/t of hydroxide produced.

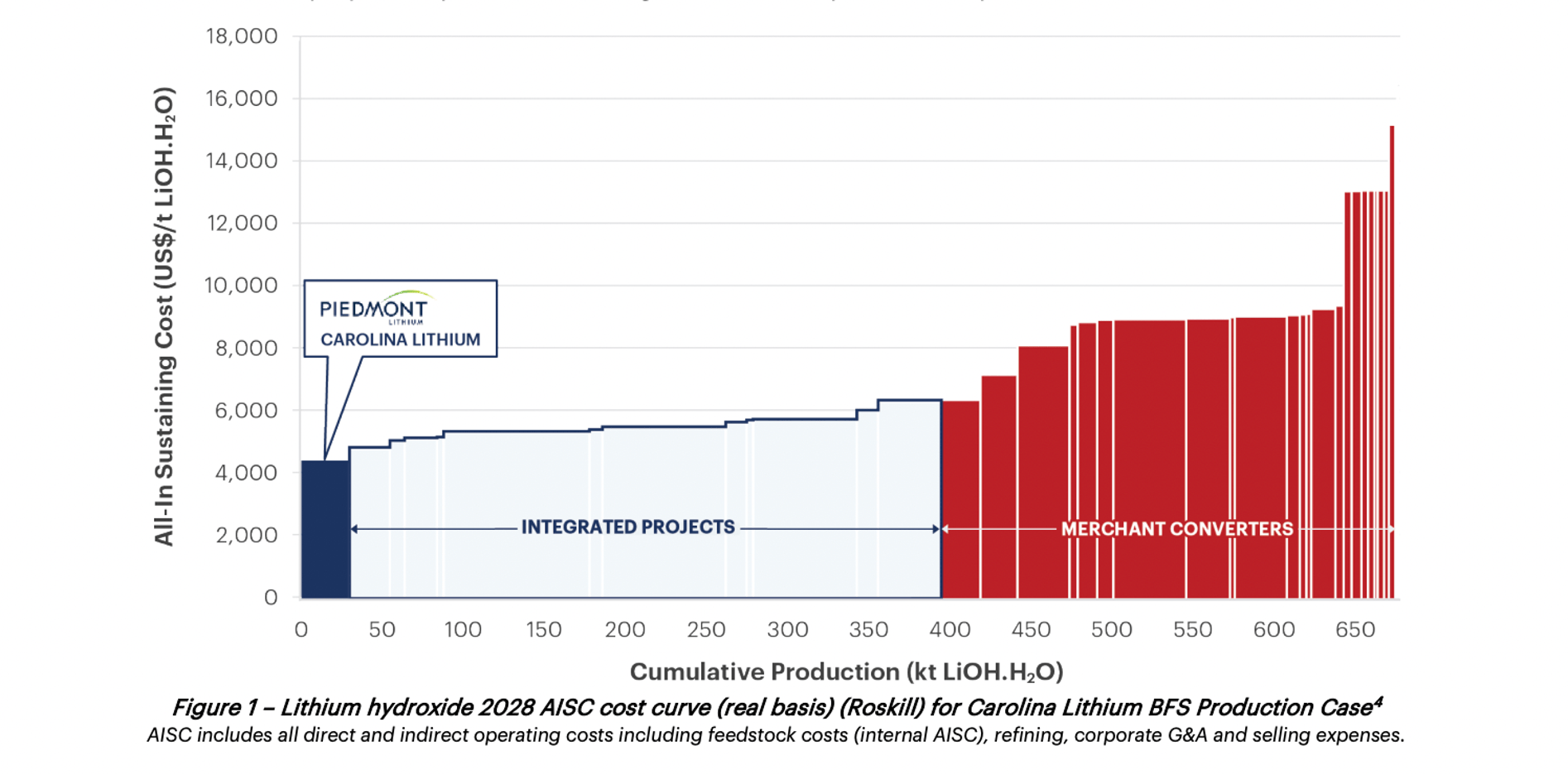

PLL’s 30,000tpa Carolina lithium hydroxide project would have steady-state hydroxide cash costs of US$3,657/t and AISC of US$4,377/t for the first 10 years.

This one is right down the bottom of the cost curve, PLL said at the time.

An updated PFS delivered January 2022 for European Metals’ (ASX:EMH) Cinovec hard rock and hydroxide project (49% interest) estimated OPEX at US$3,435/t after associated tin, tungsten, and potassium sulphate credits.

A DFS is coming Q1.

Infinity Lithium (ASX:INF) is attempting to build an underground lithium mine/hydroxide operation next door to the UNESCO World Heritage site of Cáceres, Spain.

A 2023 scoping study on the San José mine estimated cash costs of US$5,723/t hydroxide after by-product credits.

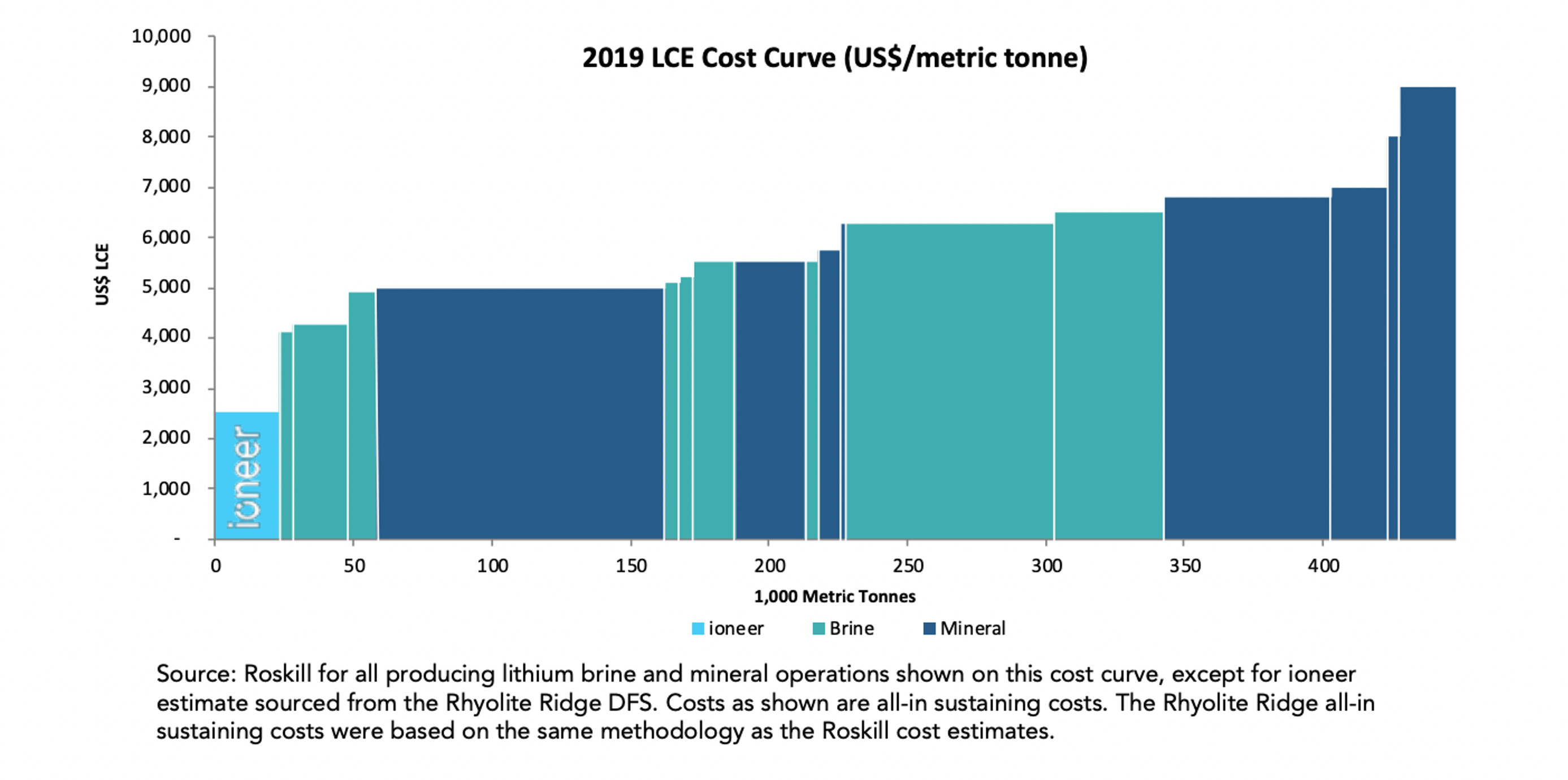

Ioneer (ASX:INR) has plans to produce carbonate and then hydroxide (with boric acid credits) from the Rhyolite Ridge project in the US.

The production of hydroxide would have estimated AISC of US$2510/t after boric acid credits (US$710/t), according to a 2020 DFS.

That would put Rhyolite Ridge right at the bottom of the cost curve, says the company, which continues to navigate an excruciatingly lengthy permitting process.

Galan (ASX:GLN) says its Hombre Muerto West (HMW) and Candelas projects are the highest grade, lowest impurity lithium brine assets in Argentina.

Under-construction HMW would be in the 1st quartile of industry’s cost curve, with a steady state average cash cost of production of US$3,963/t.

But HMW is producing lithium chloride, which would then go to a third party for conversion into battery grade carbonate.

This means GLN would receive ~72% of the long-term carbonate price, according to its estimates.

According to a December 2023 PFS Arizona Lithium’s (ASX:AZL) 6000tpa LCE Prairie brine project would have average OPEX of US$2,819/t, making it “one of the lowest cost global projects”.

However, “at this stage in the development of the Prairie project, Arizona Lithium does not intend to make battery quality lithium chemicals at the well pad,” it says.

An added conversion charge to get this to battery quality status means AZL would also receive a discount to benchmark prices.

A December 2023 DFS for Lake Resources’ (ASX:LKE) $1.4bn Kachi brine project in Argentina estimates OPEX of ~US$6,050/t LCE.

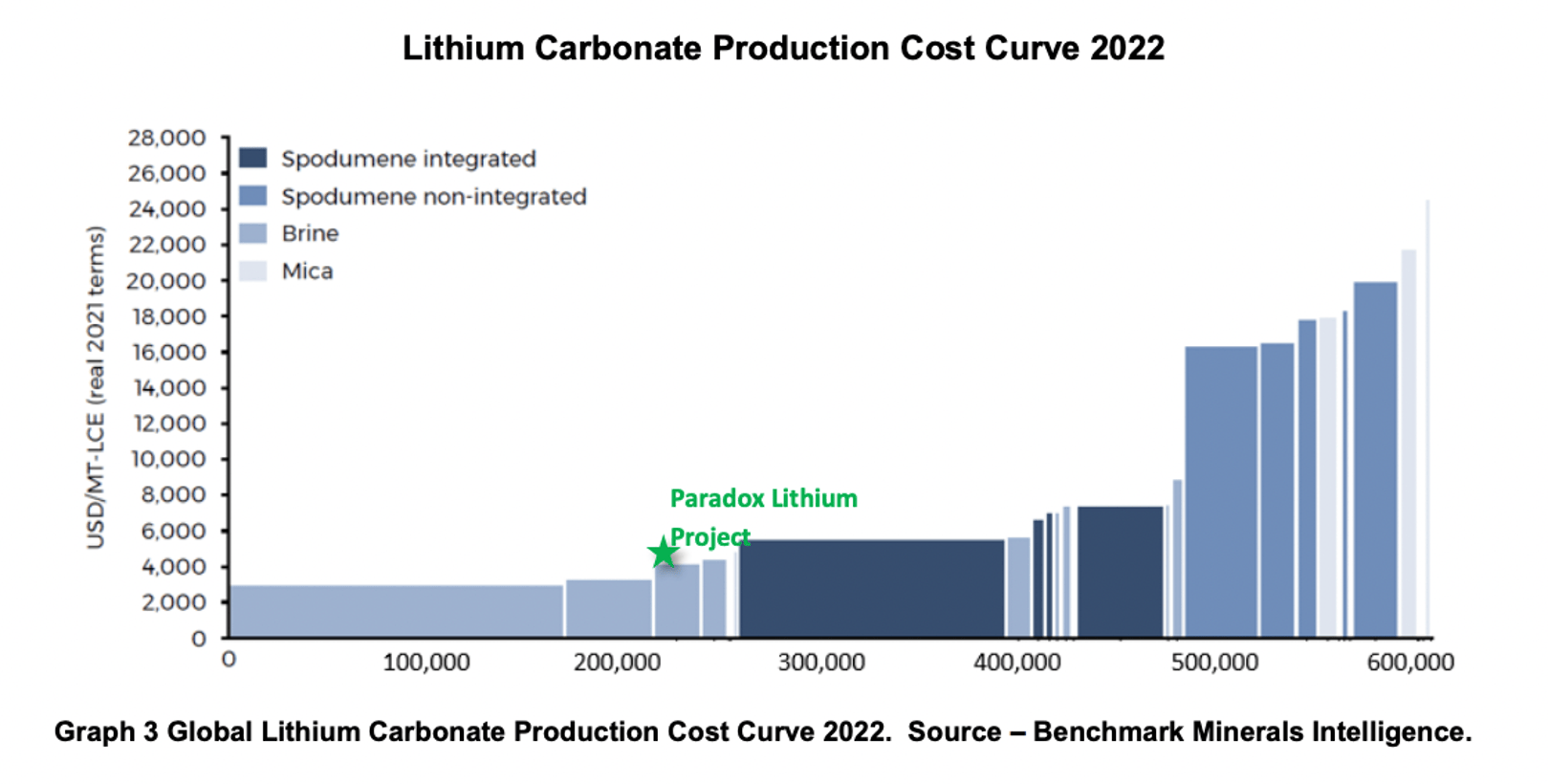

A 2022 DFS on Anson’s (ASX:ASN) Paradox brines project in the US envisaged cash costs of US$4,368/t LCE, which puts it right here on the cost curve:

Remember AVZ (ASX:AVZ)?

The monster Manono lithium-tin project in the DRC had a cash operating cost of US$371/t for a 6% concentrate, according to a 2020 DFS.

That would put it right at the bottom of the cost curve, if rampant inflation and battles over project control weren’t a thing.

Like AVZ, Leo Lithium (ASX:LLL) is having some jurisdictional dramas at the Goulamina project in Mali, where first spod is pencilled in for Q2.

However, LLL says US$365/t AISC SC6 provides solid profit at conservative long term pricing of ~US$900/t.

A 2023 PEA (equivalent of a scoping study) on Latin Resources’ (ASX:LRS) +70Mt Salina hard rock project in Brazil envisaged AISC of US$536/t.

A DFS is due late H1 this year.

Global Lithium’s (ASX:GL1) Manna project, 100km east of Kalgoorlie, has a cash cost of US$688/t for a 5.5% Li2O spodumene concentrate, according to a February 2023 scoping study.

The company has jumped straight to a DFS, which is in its final stages.

At the 207,000tpa Seymour project in Canada, Green Technology Metals (ASX:GT1) predicts cash costs of US$741/t for 5.5% spod concentrate, according to a late 2023 PEA.

A DFS is now underway.

Get the latest Stockhead news delivered free to your inbox.