Mining

Monsters of Rock: BHP's $60 billion Anglo American gambit far from a done deal

Mining

Monsters of Rock: MinRes has 'seen the bottom' in lithium prices, Lynas tightens the screws on rare earths supply

Mining

Pic: MF3d/E+ via Getty Images

Mining

A big dive for bulk commodities and timidity in the base metals complex dominated the negatives for mining investors over the past month, with all signs pointing to further demand side pain in the outcome of China’s National Congress.

Xi will continue for at least another term (and possibly for life), with strict adherence to his aggressive anti-Covid strategy seeming to be baked in for the time being.

That has sent iron ore prices to multi-year lows, with steel and property on the nose in China.

On the flipside, the cupboards are looking astonishingly bare when in comes to metal in the pantry for EVs, whether that is dwindling exchange stocks in copper, nickel, aluminium and zinc, or simply a shortage right now of lithium, which continues to scale to new record heights.

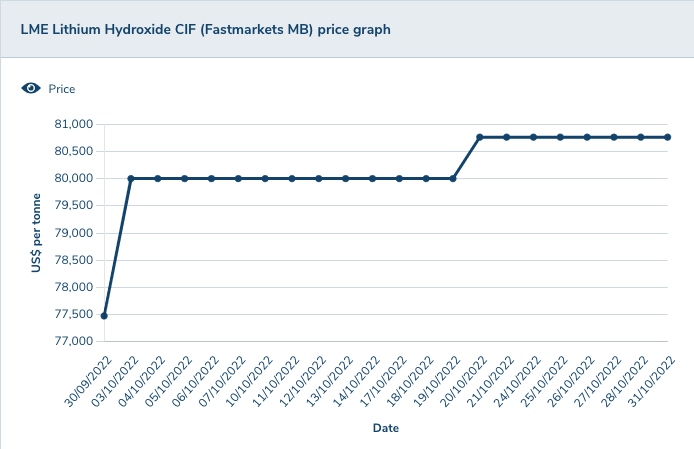

Price (Fastmarkets Lithium Hydroxide): US$82,000/t

%: +5.84%

There are few words to describe this year’s lithium boom, with prices reported by Fastmarkets for sales in China, Japan and Korea lifting a further 5.84% to US$82,000/t for lithium hydroxide.

Even at those prices many converters will be scratching at their margins, given the rollickingly high prices they are paying for spodumene, the raw material produced by WA miners.

Pilbara Minerals (ASX:PLS) is shipping at least one cargo at a price equivalent to US$8000/t for a 6% Li2O product, a 16 times lift on prices it was selling the product for two years ago.

It pulled in $8.5 million a day in the September quarter.

Is demand destruction going to come for the battery metal? Prices cannot be this high forever, but EVs remain a luxury item.

Ergo, until production lines to develop to sell general consumer EVs en masse, the wait list for Tesla et. al. is long enough that affluent early adopters will be willing to cop a price increase for the good feeling of cruising around in a vehicle that isn’t spewing exhaust fumes in the air.

It has made lithium, the commodity at the centre of the EV revolution, relatively recession proof – for now at least.

“If we were a few years down the line, during the mass-market adoption phase, then this downturn would likely be of greater concern to the EV sector,” Fastmarkets senior price development manager Peter Hannah told our Reuben Adams last month.

Hannah warned new supply will be coming eventually, with high levels of volatility as raw materials supply remains the big concern in the sector.

“Fastmarkets’ forecast is for the market to move between periods of small surpluses and deficits throughout the decade, driving continued price volatility,” he said.

“The price floor of the market is also likely to move considerably higher than historical norms as the production costs of the marginal operations inevitably increase – especially as producers have to take on board more ESG considerations.”

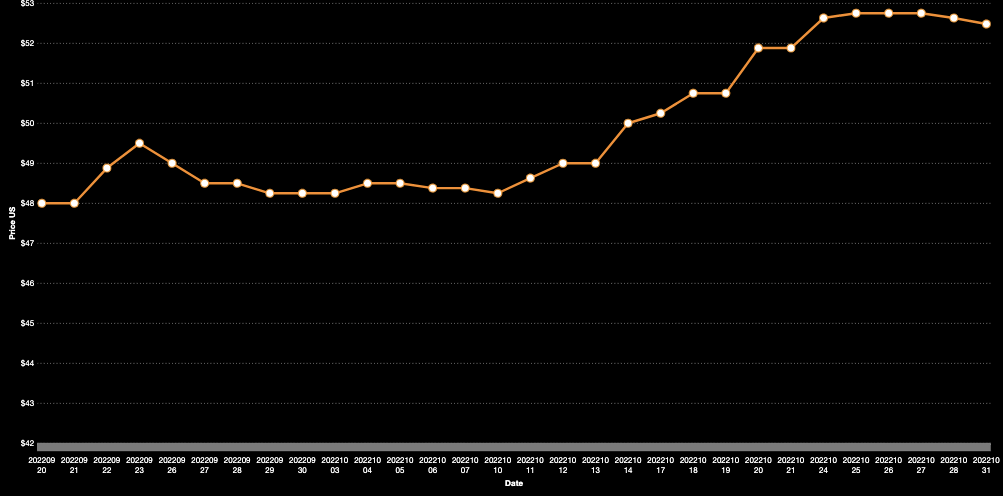

Price (Numerco): US$52.48/t

%: +8.77%

Uranium prices have had two mini-booms over the past 12 months or so, one driven by Sprott’s incessant vacuuming of spot yellowcake supplies last year and a second immediately after Russia’s invasion of Ukraine.

We’re seeing plenty of ebb and flow now on a month to month basis, but the leaders of the industry are pretty bullish around future demand.

Sprott’s ~$400 million Australian investment portfolio is now dominated by uranium players, where just three years ago it was almost entirely devoted to gold.

Cameco, the West’s biggest listed uranium producer out in Canada, still reported a $20 million loss in the September quarter, but has seen average realised prices lift 27%.

Its contracting has been rabid as well, indicating nuclear facilities are getting more serious about securing new sources of supply, especially with large Russian volumes of enriched uranium taboo.

Cameco has added 77Mlb of contracts in 2022, including 27Mlb in the September quarter.

“Nuclear energy is back in durable growth mode and Cameco is back in durable growth mode,” CEO Tim Gitzel said on an earnings call last week.

“We’re still operating well below capacity and our continued contracting success is setting us up for further growth as it lays the foundation for our transition back to a tier-one run rate.”

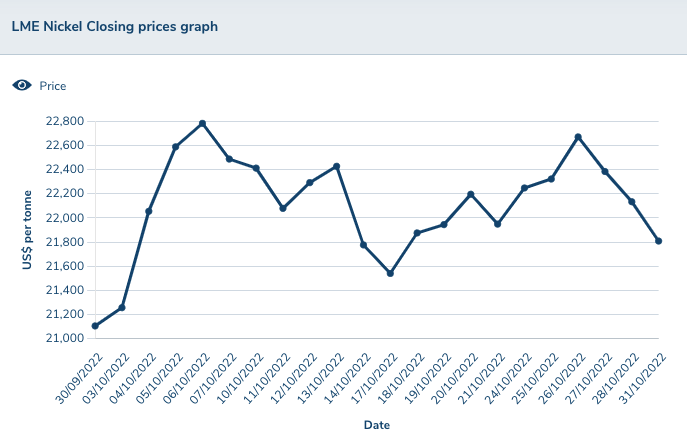

Price: US$21,809/t

%: +3.33%

Nickel is one of a host of commodities currently running at very low global stock levels some market watchers view as scary, representing just a handful of days of global supply.

That, along with demand from EV batteries, has supported prices for the metal, where miners are currently making tidy profits.

Nickel Industries (ASX:NIC) and IGO (ASX:IGO), which also produced lithium, both posted strong September quarterly reports, with the former delivering record production of over 20,000t from its RKEF nickel pig iron lines in Indonesia.

The China-backed ASX-listed $2 billion miner and processor is shifting into the battery space by converting two lines at its Hengjaya plant into nickel matte, with a deal to supply ore from its Hengjaya mine for a new HPAL project at the Weda Bay Industrial Park.

IGO meanwhile showed its acquisition of Western Areas would be an immediate money-spinner, with high nickel prices and a 50% lift in production to 9761t, making up for higher costs from its Forrestania operations.

It has some concerns on the horizon though, with a review of the Cosmos Nickel Complex acquired in the WSA deal showing it could cost around $400 million more to build than initially thought.

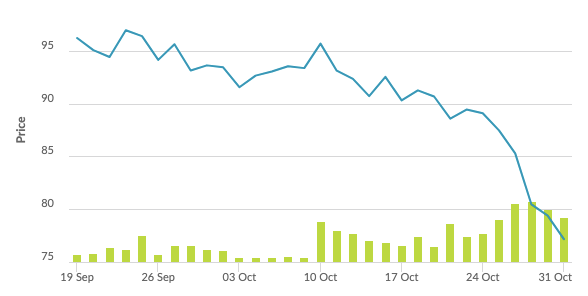

Price (SGX 62% Fe Futures): US$77.17/t

%: -18.11%

Iron ore hasn’t looked this tired since a tragic dam collapse at Vale’s Brumadinho operation in Brazil prompted the New York listed major’s production to tumble, ceding its role as the world’s largest iron ore exporter to Rio Tinto (ASX:RIO).

That sparked an all time run for iron ore, which peaked at US$237/t in May 2021, fuelled by a rush in steel production and demand around the world, but especially in China.

Support has waned though, with Covid lockdowns and a weak property market killing hopes of a second half recovery for China’s economy, a strategic aim which seems to be sliding in Xi’s pecking order.

Iron ore majors are still making big sums of cash at current prices, if not super profits, and the past couple of months have seen BHP, Rio Tinto, MinRes (ASX:MIN) and Fortescue Metals Group (ASX:FMG) all progress plans that will expand production.

While it is facing pressure right now, BHP’s big wigs still think steel and in turn iron ore will be big winners from the decarbonisation of the world’s electricity grids and transport networks.

Andrew Forrest’s FMG, which is committing US$6.2b to rid its Scope 1 and 2 emissions completely by 2030, Rio, and BHP are all plotting to spend billions in capex stripping emissions out of their mines in the coming years.

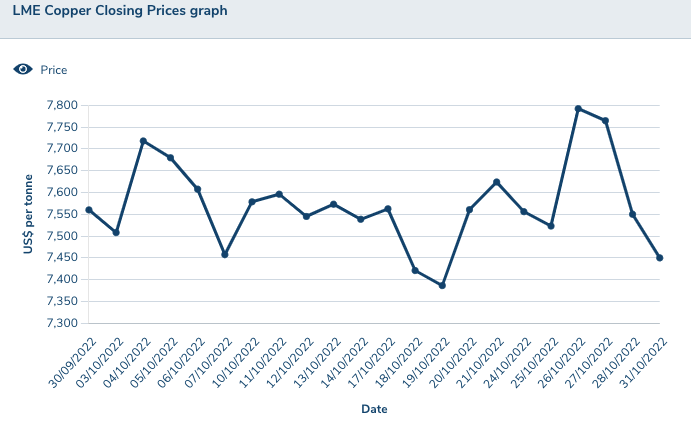

Price: US$7450/t

%: -1.45%

According to ANZ there is less than two days of copper supply in the LME’s warehouses, something propping up commodity prices while demand in its biggest market China remains spotty.

Freeport McMoran boss Rick Adkerson, in the American giant’s recent quarterly spiel, noted the backwardation seen in the copper market, indicating how desperate customers are to get their hands on physical forms of the commodity.

Mined supply is also trailing expectations, with big gaps in expected supply out of Chile and Peru, the world’s two largest copper producing nations. Chile’s state copper company Codelco reduced 2022 guidance last week from 1.49-1.51Mt to 1.435-1.465Mt just two months after updating its forecasts.

Its production year to date has slid around 10%, a factor along with lower prices in a 50.4% drop in pre-tax profit to US$2.606b so far this year.

Price (NdPr Oxide): US$89.23/kg

%: -5.23%

All the buzz is normally around the magnet rare earths neodymium and praseodymium.

But a rare niobium discovery in South Australia’s remote Arunta province has flipped the ASX’s rare earths story on its head over the past week.

WA1 Resources(ASX:WA1) is now up over 1000% in the past month and was placed in a trading halt after the minnow soared another 60% yesterday.

Now worth $1.99, WA1 stock was worth just 14c before announcing the discovery of a mineralised carbonatite containing a 142m interval of niobium rich rare earths mineralisation, headlined by a hit of 54m at 0.62% Nb2O5, 0.18% TREO2 and 3.85% P2O5 from 162m.

There are just three producers of the rare metal globally, a low temperature super conductor which is used in – among other things – particle accelerators like the Large Hadron Collider. The primary niobium product on the global market, ferroniobium, which has a niobium content of around 65%, sells for over US$45,000/t.

Meanwhile, NdPr, the most watched magnet market, has been relatively ho-hum, dropping slightly after a rebound in September.

Major non-Chinese producer Lynas Rare Earths (ASX:LYC) had a rough but still profitable September quarter after a water supply issue crimped production at its Malaysian processing plant.

Long term, demand is expected to spike from EVs and wind turbines, with Chinese producer Shenghe Resources inking supply deals with Tanzanian focusedPeak Rare Earths (ASX:PEK) and unlisted Aussie explorer VHM Limited during the quarter.

Closer to home Iluka Resources (ASX:ILU) announced a $78 million strategic investment in peer Northern Minerals (ASX:NTU) which could see it snap up the initial eight years of production from NTU’s Browns Range project as third party dysprosium and terbium feed for its Eneabba Refinery.

A DFS is due in Q3, 2023, with the mine expected to be operational in 2026.

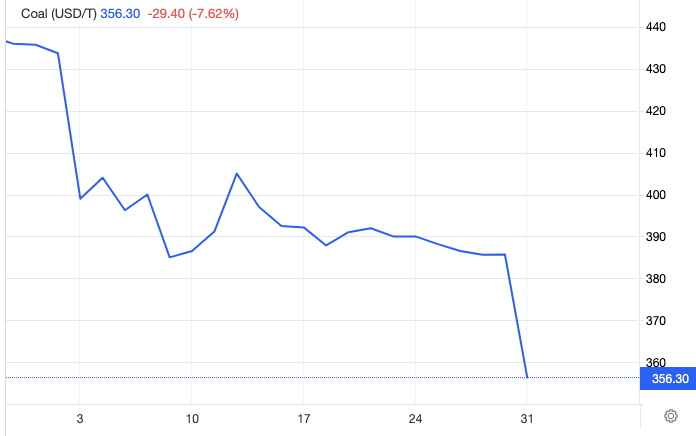

Price (Newcastle 6000kcal): US$355.50

%: -12.80%

Thermal coal prices have begun to moderate, with a big shortening of the rare arbitrage between thermal and met coal pricing in recent days.

High quality coking coal is fetching around US$311/t. At one point there was a more than US$150 gap between the two, something which saw met coal miners shift semi-soft and PCI coal to energy starved European power plants.

Prices remain heady in part due to industrial action and wet weather at Australian mines.

It’s not just ASX players like Coronado (ASX:CRN), which announced a US$225m special dividend this week, who are benefitting.

Privateers who have bet big on coal are booming, as are some of Australia’s international partners.

Japan’s J-Power, which owns stakes in a handful of steam coal mines in Oz, this week issued a record US$727 million profit forecast for the year to March 31, 61% up on the guidance it reported in May.

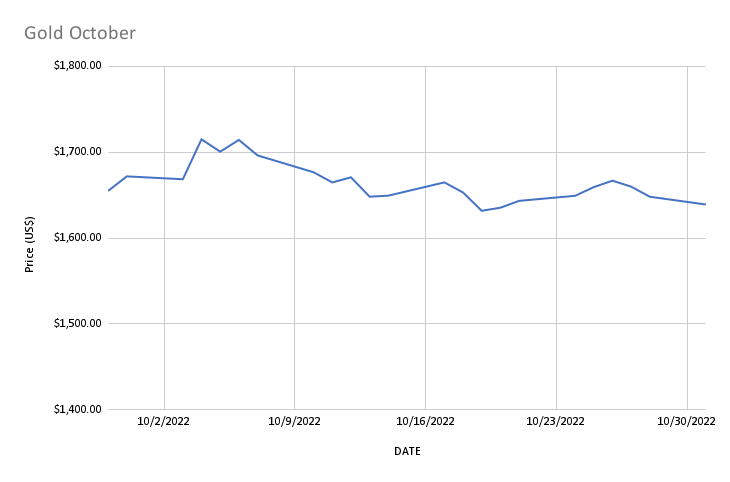

Price: US$1639/oz

%: -1.53%

Gold continues to be held in the vice grip of the US Fed’s rate decisions, the US dollar and bond yields in the world’s Yankiest economy.

Prices over here are improving thanks to the weaker Aussie dollar, but miners are facing headwinds with costs, labour shortages and borked supply chains.

Plenty are still doing a good job though. We broke down some of the top performers on all in sustaining costs in the September quarter.

Silver

Price: US$19.17/oz

%: +0.74%

Tin

Price: US$17,631/t

%: -14.55%

Zinc

Price: US$2697/t

%: -9.13%

Cobalt

Price: $US51,995/t

%:0.00%

Aluminium

Price: $2222/t

%:+2.78%

Lead

Price: $1973/t

%: +3.41%

Mining

Mining

Mining

Get the latest Stockhead news delivered free to your inbox.