Uncategorized

ASX April Winners: The best 50 stocks as inflation and Middle East tension cloud markets

Mining

Up, Up, Down, Down: Everyone's a winner in an astounding April for major metals

Uncategorized

Picture: Getty Images

Mining

We take a look at which metals were winners and which were losers over the past 12 months in this special edition of Up, Up, Down, Down.

2023 Start: US$48.63/lb

2023 Finish: US$91.50/lb

High: US$91.50/t (December 25-29)

Low: US$48.63/lb (January 1-3)

% Change: +88.15

You should never talk to uranium bulls at parties. But 2023 may have been the year their endless premonitions of a yellowcake breakout finally came to fruition.

Prices have since risen higher, scaling up to US$92.50/lb, something that will no doubt have dozens of uranium explorers on the ASX and TSX delirious at the thought incentive prices could soon be here to dust the cobwebs off low grade projects which have sat dormant for decades.

Contracting by nuclear power plants hit a decade high in 2023 as prices rose to levels not seen in 15 years, well before Fukushima and the subsequent shuttering of the Japanese reactor fleet in 2011 took more heat than Oppenheimer faced from the United States Atomic Energy Commission out of the market.

From lows of under US$18/lb a few years ago, prices have now run sufficiently high for producers to call it a new-clear renaissance and refire the first of the dormant assets to come back on the market — notably Boss Energy’s (ASX:BOE) Honeymoon mine in South Australia and Paladin Energy’s (ASX:PDN) Langer Heinrich in Namibia.

“There’s no doubt that there’s been more contracting this year than previous years. It’s a sign that utilities don’t want prices to run away from them,” Boss … boss Duncan Craib said last month as prices topped US$90 and the $1.6 billion developer signed a first supply deal.

“So they’re desperately trying to fill all their contractual needs.

“There’s not a lot of inventory available. And the key now is, where’s the new production going to come from? So it’s a fantastic time to be bringing on a new uranium mine; it’s the start of a new bull run really.”

The question mark hovering over the industry is whether the resumption of production from major players like Canada’s Cameco, Kazakhstan’s Kazatomprom and increased secondary output from BHP’s (ASX:BHP) Olympic Dam copper business could see production catch up to demand and keep new players out of the supply game.

UP

DOWN

2023 Start: US$109.30/t

2023 Finish: US$140.08/t

High: US$141.24/t (December 27)

Low: US$84.72/t (May 24)

% Change: +28.16%

Iron ore has fallen sharply to start 2024, but if the lessons of the past three or four years are to be taken as gospel, there’s reason to believe it could rise again.

The commodity that made Australia’s bogan bed and trebled our per capita ownership of jetskis (citation needed) in the 21st Century continues to be the bedrock of our perpetually over performing merchant economy.

Australia’s export earnings are projected to rise from $124b to $131b in 2023-24, with stubbornly high prices through the second half of 2023 propelled by low iron ore port stocks in China, high Chinese steel exports and speculation the Chinese Government will stimulate its increasingly fragile economy.

This is all happening despite the frailty of the Middle Kingdom’s property market, the growth engine for iron ore miners over the past 20 or so years.

On the supply side Fortescue (ASX:FMG), which charged to a record high valuation in excess of $80 billion despite the flotsam and jetsam around its green energy business, delivered the first product from its US$4bn Iron Bridge magnetite mine and Belinga asset in Gabon after setting a record 192Mt of hematite sales in 2022-23 — though both new projects will be slower to ramp than initially indicated.

Rio Tinto laid out a pathway to 345-360Mt in the Pilbara, which will require the delivery by decade’s end of the long tied up Rhodes Ridge deposit in partnership with WA mining royalty Wright Prospecting.

BHP (ASX:BHP) meanwhile has a long term target of upping its Pilbara output to 330Mt, while we will see the introduction of a new relatively large producer in MinRes’ (ASX:MIN) low grade 35Mtpa Onslow Iron project this year, which will use private roads and automated road trains to simulate the port and rail supremacy of the established Pilbara iron ore majors.

Whether this, along with the introduction of supply from Africa and Brazil could send the market into surplus is a matter of discussion between analysts, though recent high prices have seen price forecasts get increasingly bullish.

One thing is for certain — we’ll see some chunky profits from the big three in the first half of the financial year (Rio’s full year second half) — and prices are sufficient right now to support smaller players like Mt Gibson Iron (ASX:MGX), Grange Resources (ASX:GRR), Champion Iron (ASX:CIA), Fenix Resources (ASX:FEX).

And recovering iron ore prices appear to have drawn Chinese investment back into the sector. Baowu, China’s largest steelmaker, has backed MinRes’ Onslow and Rio’s Western Range JV, while Chinese backed Miracle Iron was revealed as the mystery buyer of CZR Resources’ (ASX:CZR) Robe Mesa project and Strike Resources’ (ASX:SRK) Paulsens East, both aiming to export out of the Port of Ashburton, in two deals valued at a combined $122 million.

UP

DOWN

2023 Start: US$1812.35/oz

2023 Finish: US$2078.40/oz

High: US$2078.40/oz (December 29)

Low: US$1810.95/oz (February 24)

% Change: +14.68%

Gold finally, finally, broke the top of all time highs just as 2023 came to a close. Only to revert to type by tripping back down below its near impregnable resistance again in early 2024.

Outrageous projections continue to abound, musing that gold could flip its recent narrative of wax and wane and climb to previously unthinkable heights of US$3000/oz.

Ukraine and Gaza have given a big lift to gold prices as a safe haven investment in recent times, along with hopes the US Fed could change course and begin cutting interest rates next year, something that would make gold more attractive for investors to hold.

CME Group’s Fedwatch Tool is currently factoring in a more than 60% change of a 25bps rate cut in March. Central bank buying, especially from nations like China, were another tinder fire for the price of bullion — at 800t YTD, central bank gold buying rose 14% on 2022 levels up to September 30.

The Australian gold miners enjoyed prices at spot levels in excess of $3000/oz for much of 2023, with a number of miners closing out of the money hedgebooks early to capitalise on the stabilisation of costs that ran out of control during the inflationary Covid years.

Among the top performers on the ASX were mid-tier gold miners like Westgold Resources (ASX:WGX) and Ramelius Resources (ASX:RMS), while Newmont completed the largest corporate takeover in Australian mining history with a scrip merger that consumed Australia’s largest gold producer Newcrest Mining (ASX:NCM).

UP

DOWN

2023 Start: US$8400/t

2023 Finish: US$8559/t

High: US$9372/t (January 26)

Low: US$7901.50/t (May 24)

% Change: +1.89%

Copper prices could well have gone the way of other base and battery metals, which suddenly found themselves in oversupply this year despite warnings of long-term deficits if more is not found and developed to match demand from the energy transition.

But a late year rally salvaged a near 2% gain for the red metal after Panama’s decision to curb First Quantum’s Cobre Panama mine — around 1.5% of global copper metal supply — and Anglo American’s revelation its copper output for 2024-2026 would come in as much as 19% below consensus estimates.

After a 434,000t deficit in 2022, the International Copper Study Group projects there was a 51,000t refined copper deficit through the first 10 months of 2023.

But eternal copper bulls Goldman Sachs think Cobre’s shutdown and other supply chain issues will blow the deficit back out to over 500,000t in 2024, with prices to rise above US$10,000/t within 12 months, saying prospects of a rerate to unforeseen levels of US$15,000/t or above in 2025 were now rising.

At the very least, long term copper prices will need to rise if we actually want to have any chance of doubling production by 2050 — a prediction S&P Global has floated if the world wants to hit renewable energy and transmission targets by mid-century. UBS last year upped its long term price estimate from US$7700/t to US$8800/t on higher incentive prices.

Even the latter would struggle to get all bar the highest grade copper deposits built.

More and more big miners are punting on copper as the metal of the future though, with BHP’s $9.6 billion deal to acquire OZ Minerals in the hope of building a 500,000tpa business in South Australia the key move.

Gold focused Barrick announced plans to ramp up its Lumwana mine in Zambia and invest in the Reko Diq project in Pakistan while closer to home Evolution Mining (ASX:EVN) moved on an 80% stake in New South Wales’ Northparkes mine in a ~$600 million transaction with owner China Molybdenum.

UP

DOWN

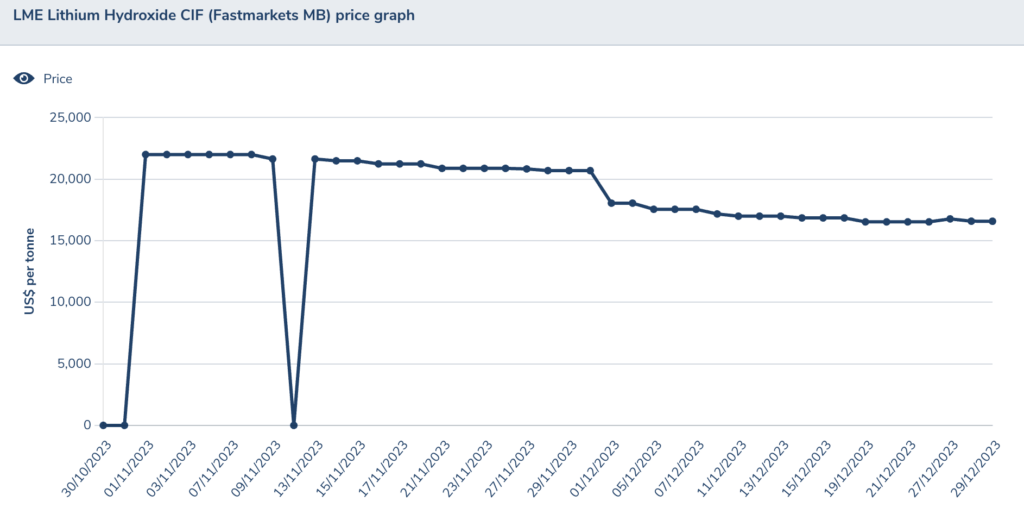

2023 Start: US$83,500/t

2023 Finish: US$16,580/t

High:US$83,500/t (January 1)

Low: US$16,580/t (December 29)

% Change: -80.14%

Lithium prices could never stay where they were, a level even Pilbara Minerals (ASX:PLS) chief Dale Henderson said no one ever predicted or thought imaginable.

But it was the velocity of 2023’s price fall, which helped drag lithium-ion battery pack costs to a record low price of US$139/kWh in late 2023, that caught everyone off guard.

In September, Core Lithium (ASX:CXO) was toasting a maiden profit, a reward for kicking its Grants lithium mine and broader Finniss project in the Northern Territory into gear in quick speed despite recovery issues and changes that would see it produce a little over half of the spodumene concentrate it initially planned.

By the start of January mining had been halted off the back of what Core said was an 85% fall in prices.

Initially Australian producers were shielded from a fast collapse in chemical prices. Lagging contract measures and a shortage of raw materials vis-a-vis processing capacity in China ensured the spodumene price remained profitable through most of the year.

But even the mighty Greenbushes mine was forced to curtail production amid a price fall as 6% Li2O spodumene prices fell from over US$8000/t (more in the US$4000-6000/t range as far as contracted volumes were concerned) to spot levels of a little over US$1000/t. For producers selling product below the benchmark — pretty much all of them as higher prices incentivised lower product grades which improved overall recoveries — prices are certainly pushing on cash costs.

Will there be a shakeout of the lower quality producers? That remains to be seen. The majors certainly have the cash now to pounce if M&A becomes attractive again.

But there could be wariness given the historical volatility of the sector and the premiums even pre-development and exploration plays have commanded. Liontown Resources (ASX:LTR) was set for a top of the market — $6.6 billion — sale to America’s Albemarle last year before Gina Rinehart’s Hancock Prospecting built a $1.3 billion blocking stake that scuppered the sale and pushed its share price back to $1.48 (against the $3 bid price) yesterday.

Hancock has also partnered with SQM in a $3.70 per share bid — $1.7 billion — for pre-resource Pilbara explorer Azure Minerals (ASX:AZS), a sign the big dogs will still pay top dollar to own the yard in preparation for a future boom.

UP

DOWN

2023 Start: US$404.15/t

2023 Finish: US$136.95/t

High:US$404.15/t (January 1)

Low: US$117.50/t (November 1)

% Change: -66.11%

Like lithium, and for completely different reasons, coal was one of the big winners in 2022.

2023 was a complete reversion, with the demonised fuel pulling a roughly two thirds loss as concerns about perpetual shortages were allayed.

A milder than expected northern winter meant gas stores were more than enough to supply European energy needs. That saw discounted coal flood the market, pulling prices back to Earth.

Certain metallurgical coal grades, notably PCI, also saw big price falls after mooning in the wake of Russia’s invasion of Ukraine. Cheap Russian material flooded the market for PCI in 2023.

At the same time high quality premium hard coking coal, where supply chain issues saw muted exports out of Queensland, was a beneficiary of both rising Indian and Chinese steel production, as well as the end of an unofficial two year ban on Australian coal imports in China.

With iron ore prices also surging on higher than expected Chinese steel output, Aussie met coal futures remain above US$330/t.

A 243 day run where Newcastle thermal coal carried a premium to coking coal was halted in early 2023, with both reverting to type.

It saw thermal coal producers look for ways to move into the met coal sphere, inspiring major competition for two BHP met coal mines hived off from its BMA JV with Mitsubishi. The winner was NSW-based Whitehaven Coal (ASX:WHC), which saw off opposition from an activist hedge fund to secure the up to $6.4 billion deal for the Blackwater and Daunia mines.

Once complete it will see around 70% of WHC’s earnings come from met coal, and make it more attractive for financiers loathe to support fossil fuel producers.

UP

DOWN

2023 Start: US$104/kg

2023 Finish: US$62.50/kg

High:US$110.30/kg (January 31)

Low: US$61.12/kg (December 20)

% Change: -40%

Rare earths entered 2023 at levels that, while well down on early 2022’s extraordinary highs, still delivered strong support to burgeoning producers.

But China’s indifferent economic performance and its quota system for rare earths production, which is highly concentrated among the country’s major producers, combined to chill prices to the point Lynas (ASX:LYC) — the only major producer of NdPr outside of Chinese control or influence — began stockpiling for sunnier times.

China’s total rare earths mining quotas were raised 14% in 2023 to 240,000t, and China Northern Rare Earths announced cuts to prices across its commodity suite for this month, suggesting the trend around rare earth element pricing will continue in the near term.

Until Chinese New Year buyers could stay out of the market or expect lower prices. But the long term dynamics are certainly there to support an uptick in rare earths production.

The big question is where will it come from and will there be enough support to help producers in the west emerge and diversify the market for the metals, the most prominent of which are used in the permanent magnets essential to wind turbines and electric vehicle motors.

Peak Rare Earths (ASX:PEK), based in Tanzania, has taken a can’t beat ’em join ’em approach by linking up with China’s Shenghe Resources to set up its Ngualla project for production. But closer to home Northern Minerals (ASX:NTU) has been fighting off Chinese interlopers on its share register, while Gina Rinehart backed Arafura Rare Earths (ASX:ARU) and Andrew Forrest supported Hastings Technology Metals (ASX:HAS) have advanced projects waiting for a turnaround in pricing.

Some of the most exciting projects on the market though have been identified over in Brazil, where Meteoric Resources (ASX:MEI) and newly-listed Brazilian Rare Earths (ASX:BRE) are sitting on ionic clay style resources which eclipse the grades of similar deposits mined for years in southern China.

UP

DOWN

2023 Start: US$30,550t

2023 Finish: US$16,603/t

High:US$31,000/t (January 4)

Low: US$16,079/t (November 27>

% Change: -45.65%

The first casualty of 2023’s dramatic near halving of the LME nickel price has already been seen in Panoramic Resources (ASX:PAN), where administrators have made the cut-throat decision to halt production at the Savannah nickel mine in WA’s Kimberley region.

Around 140 staff were stood down, less than a month after FTI moved in to take over the operations of the flailing nickel, copper and cobalt producer, which was a significant mid-tier miner in nickel’s halcyon days in the mid-2000s when the former Sally Malay Mining ran Savannah and the Lanfranchi asset near Kambalda.

The price dive, which has operations like Panoramic’s and First Quantum and POSCO’s Ravensthorpe mine under water, came as Indonesian producers dramatically up-scaled in 2023.

In 2022, Indonesian nickel output recovered from its Covid era blue, lifting 32% to 1.16Mt. But that could have been as high as 1.65-1.75Mt in 2023, throwing the market into a 239,000t surplus according to the International Nickel Study Group.

There could be handbrakes placed on the sector. The country’s nickel miner’s association warned higher grade reserves could be depleted in six years if mining continues at its current pace at an INSG meeting earlier last year, according to Reuters.

An explosion at a Morowali industrial park plant late last year has also thrown the spotlight on safety concerns after 19 workers were killed in the industrial accident.

The other concern has been the steady creep of Indo producers into the battery metals space. Previously thought to only be able to produce Class II nickel in nickel pig iron suited for lower grade stainless steel, laterite deposits in Indonesia are being processed into nickel matte and mixed hydroxide, comparable products to Australian and Canadian refined nickel sulphides that can be used in electric vehicle batteries (though produced at a higher CO2 intensity.)

There is of course, a way for Australian investors to play Indonesia’s nickel supremacy in the form of Nickel Industries (ASX:NIC), which has linked up with Chinese stainless steel giant Tsingshan to become one of the fastest growing nickel producers in the world.

The $2.8 billion capped miner and processor produced 33,852t of nickel metal from its four Indonesian RKEF plants in the third quarter of 2023, generating US$97.6m in EBITDA on a 100% basis at a margin of US$3009/t on NPI and US$1971/t on nickel in matte at cash costs ranging between US$9467/t and US$11,379/t.

UP

\

DOWN

Prices correct as of December 31, 2023.

Silver

Price: US$23.79/oz

%: -0.66%

Tin

Price: US$25,415/t

%: +2.45%

Zinc

Price: US$2658/t

%: -10.58%

Cobalt

Price: $US29,135/t

%:-43.9%

Aluminium

Price: $2384/t

%:-0.33%

Lead

Price: $2068.50/t

%: -9.32%

Uncategorized

Mining

Uncategorized

Mining

Mining

Mining

Get the latest Stockhead news delivered free to your inbox.