Pic: Andrii Zastrozhnov/iStock via Getty Images

The commodity where prices have become ‘unsustainable’… and it’s not nickel or lithium

Mining

Pic: Andrii Zastrozhnov/iStock via Getty Images

Mining

A mining expert who has followed the platinum group metals industry for 25 years says PGE prices have to rebound to incentivise new production with over half of the world’s producers bleeding cash.

Bridge Street Capital’s Chris Baker says prices for palladium, platinum and rhodium — used in catalytic converters to reduce toxic emissions from gasoline and diesel powered automobiles — are not sustainable.

Major producers are now cutting staff and curtailing projects in the face of prices that have crumbled from all time highs in excess of US$3000/oz for palladium two years ago to around US$966/oz today, having sunk as low as US$875/oz earlier this month.

Platinum, which is largely produced in South Africa, never received the post-Ukraine bump of Russian dominated palladium, but is also trading at a subdued level of US$893/oz. Rhodium, meanwhile, which threatened US$30,000/oz in 2021 and has become an important co-product for platinum and palladium producers, is fetching around US$4500/oz.

“I wouldn’t be forecasting sub US$1,000 platinum and palladium. I think the sort of numbers I’d be looking at, would be somewhere north, probably up around US$1200-1300/oz sort of levels for both platinum and palladium,” Dr Baker told Stockhead.

“I think that it just reflects the cost curve. The industry is not sustainable at current levels.

“So I think it’s quite reasonable to expect that we will see — as with nickel, as we’re seeing with copper — we will see prices normalise.

“As we’ll see with lithium. Clearly spodumene prices just are not sustainable.

“So I think to see a modest recovery (in PGE prices) is reasonable and we then have to think ‘well, OK what is the most likely project to see the light of day?'”

PGM mining is highly concentrated and relatively opaque, with production dominated by South Africa and Russia, where it is mainly a by-product of base metals produced by Norilsk Nickel.

Anglo American, which runs four major operations at Mogalakwena, Amandelbult and Motololo in South Africa and Unki in Zimbabwe, mines or processes in the order of 25-30% of the world’s PGM ounces.

After a 71% dive in profits, Amplats announced plans to retrench 3700 jobs or 17% of its workforce in South Africa to cut costs.

Its 2024 guidance of 3.3-3.7Moz at US$920/oz is down from 2022 (4.2Moz) and 2023 (3.8Moz) and has Anglo has warned that number remains subject to load shedding from beleaguered South African power provider Eskom.

Sibanye-Stillwater has, with union intervention, agreed to reduce job cuts at its South African mines from over 4000 to 2600.

South Africa’s mining lobby thinks as many as 7000 jobs could be lost across the industry, the sign of a sector reaching its tipping point on prices.

They have been shielded in part by two years of extraordinary profitability after palladium prices surged in the wake of Covid and the Russian invasion of Ukraine, Baker said.

“Ordinarily, at this point in the market, these guys might have fairly weak balance sheets, because they’ve been supporting marginal operations,” he said.

“They’ve been undertaking capex where perhaps they shouldn’t be. But in fact, all the balance sheets are pretty good.”

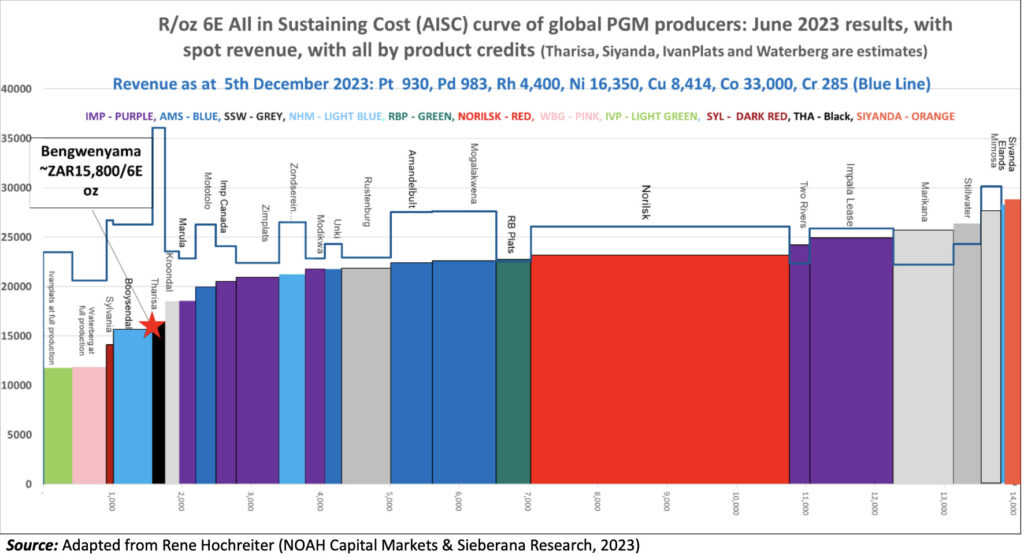

But there are big issues for the sector from a structural perspective because over 50% of platinum and palladium production is now being completed at depths of greater than 1000m.

“They are expensive, expensive old mines,” Baker said.

“Cost curves I’ve seen would suggest that probably half the industry on an all in sustaining basis is probably underwater.

“That doesn’t mean they can’t stay there for a while — they can because the usual sequence of events is they do the easy cuts and chop a bit out of head office and then they start cutting back on capital expenditure.

“They keep pruning and pruning and pruning until they just can’t stand it any longer. And then they have to start closing shafts.

“I couldn’t even tell you how long it’s going take but it could be a year before the big Western Limb operations really start cutting production back big time.”

Other factors are at play. South Africa is in an election year and the African National Congress, under more pressure from its voter base than it’s been since the end of the Apartheid regime, won’t want to see widespread job losses.

The devaluation of the Rand has also aided South African miners, who receive payment in US dollars.

The issue, as much as older mines curbing production, is the capacity of new miners to get up and running at current prices.

Demand for platinum and palladium is theoretically challenged by the rise of electric vehicles, but Baker doesn’t see that as the issue many believe it is.

He says rising demand for hybrids, a view held by the world’s largest carmaker Toyota, was bullish for palladium and platinum demand.

That means at some point new mines will need to be approved. Current prices won’t incentivise them, especially given the relatively complex nature of the PGM supply chain.

It’s not just enough to have the metals in the ground. You need to be able to sell them into a smelter, either one which relies on high grade PGM concentrate, or one which can handle PGM concentrates with significant base metal credits.

Ivanplats, backed by legendary mining entrepreneur Robert Friedland, is targeting first production this year from the first stage of its Platreef mine, which will produce 113,000ozpa of platinum, palladium, rhodium and gold along with nickel and copper credits.

It has a total cash cost of US$514/oz according to study results. But whether market conditions support the development of two concentrators that will take it beyond an initial 770,000tpa milling capacity to 5.2Mt by 2030 is up in the air.

Johannesburg-listed Tharisa Capital have pushed back the commissioning of the Karo open pit mine in Zimbabwe 12 months to mid-2025 in the hope of capturing higher prices once it is in production.

“You can see there’s a fair bit of stress that’s emerging, even for projects under construction,” Baker said.

Another mine on the Northern Limb of the Bushveld Complex — Waterberg — also looks marginal, its proponent now considering a processing deal with far-flung but big spending Saudi Arabia after part owner Impala Platinum baulked on offtake.

Baker said it illuminated an issue for platinum and palladium producers and showed why . To see the light of day you need to be able to find smelting capacity that can handle your product.

“I think the market sort of forgets and thinks it’s just like precious metals and mining gold. Well it’s not,” he said.

“It’s like nickel and it’s like copper, you’ve got to have smelters and refiners that can deal with this ore and they’ve got to give you appropriate payability so that you’re not just doing it for fun, you’re actually making some money and that I think is a big issue that’s yet to be fully understood by the market.”

PGE stocks on the ASX enjoyed a boom time a couple of years ago, not just from rising palladium and rhodium prices, but also from Chalice Mining’s (ASX:CHN) discovery of a magmatic nickel, copper and PGE resource at Julimar just 70km northeast of Perth in early 2020.

It rose quickly to become a rare thing — an ASX 200 company which was not only pre-revenue, but on inclusion was yet to even publish a resource.

Chalice now has what it boasts is Australia’s largest nickel sulphide discovery in two decades, though palladium will be the biggest contributor to revenue.

Once worth over $3 billion, however, the Tim Goyder backed explorer is now worth $490 million — including a surprise 25% lift yesterday — after it was hauled over the coals for a scoping study which used a commodity price deck well above spot levels supporting a bulk, high capex development.

“Great discovery, they’ve done a fabulous job there,” Baker said. “I think they’ve learned from the initial scoping study, which wasn’t perfect.”

There are other Australian exploration stories.

Mark Creasy-backed Galileo Mining (ASX:GAL) made a find a couple years back at Callisto near Norseman which caught the eye of the market, while Legacy Minerals (ASX:LGM) captured some love of its own for announcing AI exploration tools had helped uncover a first of its kind magmatic PGE prospect in New South Wales’ copper and gold-rich Lachlan Fold Belt.

Up in the Kimberley one of the longest known Australian PGE discoveries — Panton — is now in the hands of Future Metals (ASX:FME), which has some firepower literally on board with the recent appointment of former New Century Resources MD Patrick Walta as executive chairman.

He told Stockhead Panton, where around $50m has been spent by a succession of explorers to date, had the benefit of sunk capital and a known metallurgical processing route to achieve high grade concentrates.

A scoping study last year suggested it could produce 117,000oz of platinum, palladium and gold (161,000ozPdEq including copper, nickel and chromite credits) at second quartile costs of US$789/oz.

Walta told reporter Michael Washbourne prices would turn.

“The last thing you want to be is a PGM producer right now, we’re at about the 60th percentile on the cost curve, so there’s a lot of producers now that are just haemorrhaging cash,” he said.

“We’re seeing supply getting stripped out of the market and, ultimately, that’s going to lead to a price turn. Our strategy with Future is to be production-ready as soon as the price starts moving. We will rise first and we will rise fast. That’s our play, it’s a massive option on PGM prices.”

Given their not based on the doorstep of the smelters in the Bushveld, Baker said what he wants to see from Australian PGM stocks is clarity on what their path to market and payabilities are going to be.

That is especially in the case of Julimar, which has significant nickel and copper credits.

Also on the ASX are a couple of international players focused on the more established South African and Zimbabwean markets.

Southern Palladium (ASX:SPD) listed in 2022 and earlier this month released a scoping study on its Bengwenyama project on the Bushveld’s Eastern Limb.

It says mining on the UG2 Reef at Bengwenyama could be undertaken for 36 years based off mining 52Mt of ore containing 10.9Moz of palladium, platinum, gold, rhodium, ruthenium, iridium and osmium.

Extracting 2Mtpa from the UG2 reef at a mill feed grade of 6.55g/t, the junior says it could produce 330,000oz of 6E PGMs per annum with a capital cost of US$408m, life of mine all in sustaining costs of US$836/oz and 4.5 year payback at prices slightly above current spot levels of US$1200/oz Pt, US$1100/oz Pd and US$5000/oz Rh.

“The UG2 Reef is a chrome reef with about equal amounts of platinum and palladium, with rhodium at very low base metals and they’re not dependent on base metals for their revenue,” Baker said.

“They’ll get a bit of money for it but they’re not dependent on it. So what they call the prill split is about 44-44 for platinum and palladium, 10% rhodium, a couple per cent gold and then a few other bits and pieces, a bit of iridium too as well.

“If they got nothing for the base metals it wouldn’t matter, this should still be a commercial operation.”

On the production side there is $1.84 billion Zimplats (ASX:ZIM), a listed subsidiary of South Africa’s Impala Platinum.

Its shares tumbled 10% yesterday after revealing a 105% fall in profits after tax to a US$8.76m loss for its first half, down from a US$159.6m profit in H1 FY23. The Zimbabwean miner shaved its divided by 17% to 92.9 US cents.

That came despite a 9% lift in 6E production YoY to 327,810oz, with nickel tonnes up 7% to 3050t, silver production 16% higher at 25,934oz, copper 10% up to 2336t and cobalt tonnes 34% higher at 51.

Its accounts showed a 42% fall in received palladium prices and 70% drop in rhodium pricing, with nickel and cobalt sales also copping significantly lower prices.

As for the future of the palladium price, Baker thinks much will also depend on the attitude towards metals produced by Russia, the world’s largest producer with around 43% of the market.

READ ALSO

Something must give as “unsustainable prices” hit energy transition metals: Chalice

Sunk capital: Why Walta believes Panton will be the future king of PGMs

At Stockhead, we tell it like it is. While Future Metals and Legacy Minerals were Stockhead advertisers at the time of writing, they did not sponsor this article.

Get the latest Stockhead news delivered free to your inbox.