Pic: Via Getty

Resources Top 5: Lithium M&A, more nuggets, and a ‘career-best’ gold hit

Mining

Pic: Via Getty

Mining

Here are the biggest small cap resources winners in morning trade, Monday January 9.

After soaring to record levels in 2021, the global merger and acquisition (M&A) market slowed in 2022 against a challenging economic environment.

It is expected to rebound strongly in 2023, says Goldman Sachs, which is good news for investors.

First cab off the ASX rank in 2023 is small but advanced lithium explorer ESS, which received a takeover offer from Tianqi Lithium Energy Australia (TLEA), a JV between $US19bn capped Tianqi Lithium (51%) and $10.5bn IGO (ASX:IGO) (49%).

Growth-hungry TLEA currently owns an integrated lithium business in WA, including a 51% interest in the Greenbushes lithium operation and the Kwinana lithium hydroxide refinery.

The deal values ESS at ~$136m, or 50c per share –a 44.9% premium to the last closing price.

The offer is well below ESS’ high of 69c per share reached in April last year, but the board has unanimously recommended the deal in the absence of a superior proposal.

Managing director Tim Spencer says it provides certainty for ESS shareholders in the context of an uncertain economic outlook.

“We believe this transaction is a great outcome for Essential shareholders and for other stakeholders including employees, suppliers, the Ngadju people and the State of Western Australia, all of whom will benefit from the Pioneer Dome Lithium Project being developed by a large, well-financed and experienced lithium sector participant as is TLEA,” he says.

“The Board is extremely proud of the hard work and achievements of the Essential team and the significant progress made in advancing the Pioneer Dome Lithium Project to its current pre-development stage.”

The Scheme is subject to various conditions including approval by ESS shareholders at a meeting proposed to be held in April 2023.

ESS’ Pioneer Dome lithium project in WA contains an actual resource (more than most ASX explorers can boast) of 11.2Mt at 1.16% lithium.

A scoping study on the project had kicked off September 2022, with first lithium production pencilled in for 2025.

ESS says in light of the above proposed scheme, all project financing and off-take discussions will be paused until further notice.

Sprott-backed explorer TMR is pulling up super high-grade gold in drilling at the Elizabeth project in British Columbia, Canada.

Boss Jason Bahnsen calls the highlight 28.5m at 28.1g/t gold hit “extraordinary” and “one of the best intersections I have seen during a +30-year career”.

That would be impressive if anything close to true width, because the high-grade mineralisation at Elizabeth has so far presented itself in vein sets 0.5m to 6.5m wide.

This thicc paydirt came from the No. 9 Vein, which is now 150m long and counting.

“The bonanza and high-grade zones of both the No.9 Vein and the [nearby] Blue Vein have now been extended to over 150 metres each in strike,” Bahnsen says.

“Structurally it is possible that the No. 9 and Blue Veins join together with the potential for additional gold mineralisation to cumulate in the area of the intersection and with further extensions along strike to the south-west.”

Assays for six Elizabeth gold project drill-holes remain pending, including holes for No. 9 Vein, Blue Vein and West/Main Vein.

The combined 315sqkm Blackdome-Elizabeth project is a high grade past producer.

The Blackdome mine, which produced ~230,000oz at 10.5 g/t gold between 1985-1991, includes a fully permitted process plant and associated tailings storage facility.

Elizabeth, ~30km away, is relatively underexplored.

TMR says the high-grade quartz veins at Elizabeth show close geological similarities to the Bralorne-Pioneer system (~30km south), which was mined to a depth of 2,000m and produced more than 4Moz of gold from ~1900 to 1971.

TMR’s drilling program will culminate in a resource estimate in the current quarter.

Some good news from fresh-faced copper producer AR1, which is now “operationally cash flow positive” after achieving commercial production at its Mt Kelly crushing/processing facility in Queensland.

Following a steady ramp up over October and November, AR1 produced 33.3t per day of plated copper cathode during December (976t all up at a cost of $8.9m), with the ultimate goal being 33.5t per day.

It was a hard slog for AR1 in 2022, thanks to rising costs, covid-infected workers, and a bearish copper price.

Dec’s production was also hindered by wet weather, but it was enough for AR1 to record its first operational cash flow positive month.

Costs will soon decline as production hits steady state, it says.

The company expects to produce 40,000t of copper cathode over a four-year period from mid-2022.

READ: OZ is all but gone, so where to thrift some quality ASX copper?

SBR reckons there’s potential for a significant upgrade to the existing 110kt NiEq sulphide resource at the Sherlock Bay project in WA.

Great news for the junior, which already believes the project would be profitable to build.

A new EM survey at Sherlock Bay has detected a strong conductor extending for 1km at the western end of the current nickel sulphide resource, representing a major drill target.

“The detection of a major new, untested, EM conductor extending west of the current nickel sulphide resource at Sherlock Bay highlights the potential to expand and upgrade the existing nickel-copper-cobalt sulphide resource and enhance the project’s economics.,” SBR CEO Jon Dugdale says.

“Significantly, the new EM anomaly is the strongest detected from surface to date and lies immediately west of the Company’s recent massive and breccia matrix sulphide intersections.

“This indicates strong potential for additional massive sulphide discoveries in this new target zone.”

SBR says the project is already lucrative at today’s nickel prices.

A Scoping Study completed in January 2022 highlighted “significant cash-flow potential” at a nickel price of US$10/lb (US$22,000t).

The nickel price has since increased by over 30% to around US$13.50/lb (US$29,00/t).

“The project economics of Sherlock Bay have already been shown to be cash-flow positive at a nickel price of US$10/lb,” Dugdale says.

“This would be significantly enhanced through further, higher-grade, sulphide discoveries on top of the more than 30% increase in the nickel price since the scoping study was completed – based on increased global demand for ‘future facing’ battery metals.”

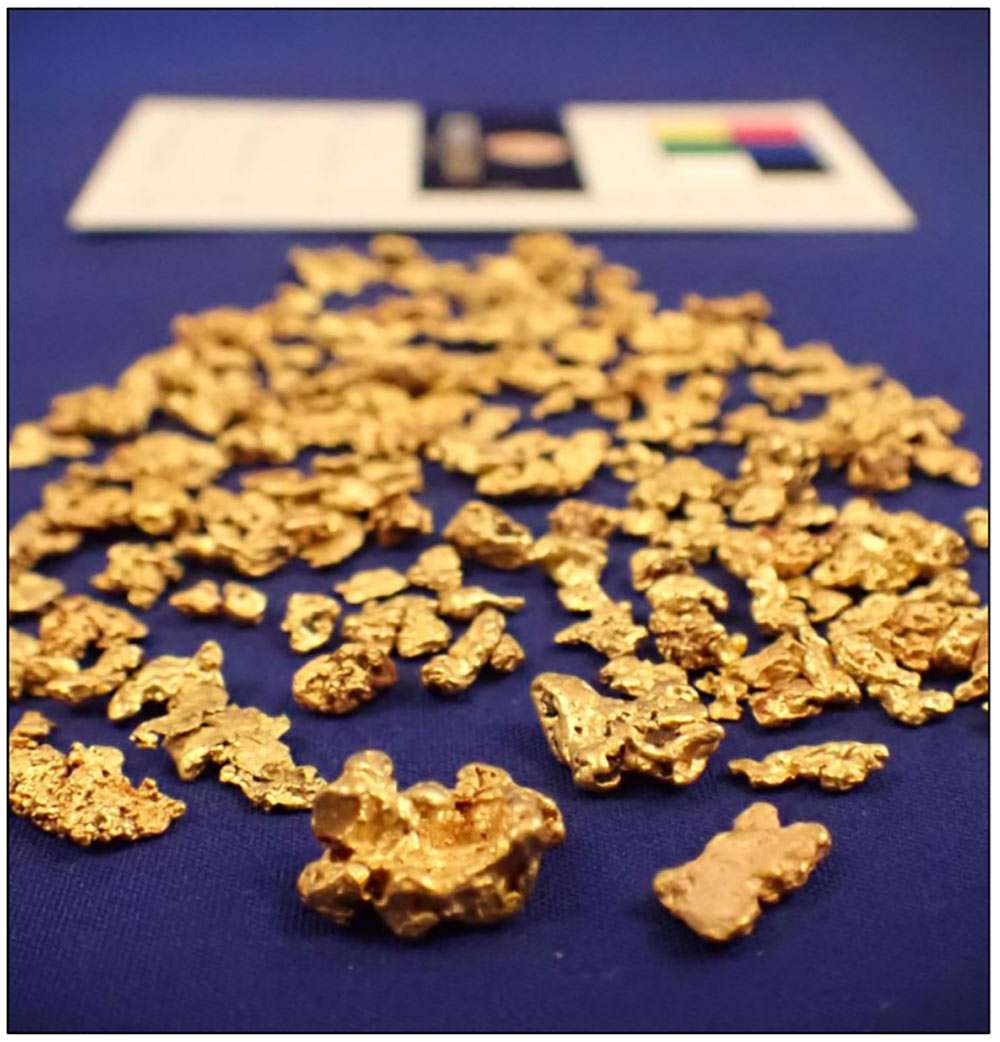

ICL has also uncovered a new target — this time at the Goose Well, part of the 14 Mile Well gold project in WA.

Metal detecting at Goos Well has discovered a surface gold nugget anomaly, ICL says.

Here’s a selection of gold nuggets from the parcel of >150 nuggets picked up:

Very nice. The target area hosts a so-called ‘syenite’ intrusion, which ICL says are linked to major regional gold deposits.

In November, ICL was picking up gold nuggs like this over several kilometres at the Guyer and Everleigh prospects at 14 Mile Well.

The shape and composition of the nuggets suggest primary sources are nearby, says ICL technical director David Nixon.

Metal detecting and geological field work will continue through 2023 at Goose Well and other developing target areas within the 14 Mile Well project.

Get the latest Stockhead news delivered free to your inbox.