Mining

Monsters of Rock: MinRes has 'seen the bottom' in lithium prices, Lynas tightens the screws on rare earths supply

Mining

Monsters of Rock: Canberra takes a bright red pen to nickel and lithium earnings forecasts

Mining

Pic: Image Source/DigitalVision

Mining

Uranium has headed to the substitute bench in recent weeks, with enthusiasm for copper, record gold prices and hopes of a lithium price rebound taking over from the glowing metal as the stories of the day.

A speculative bull run for uranium peaked at US$107/lb in January.

But despite claims from within the industry that a structural shortage of material would make rising spot prices hard to stop, new mine starts and murmurs of production upgrades from Canada’s Cameco have combined to send U3O8 prices back to US$85.50/lb yesterday.

Is this the sign yellowcake’s cheerleaders got ahead of themselves, or just a bump in the road for the nuclear renaissance?

Sprott’s Jacob White is well and truly in the latter camp.

“This retreat follows a historic rapid run for the uranium spot price, which increased nearly 80% in seven months from July 2023 to January 2024. We believe the February price action marks a natural and healthy pause in the current uranium bull market,” he said.

“Before retreating to the current price, February saw the uranium spot price hit a recent high of $107. Subsequently, a pause in buying activity has lowered

trading volumes in the spot market.

“Prices were also negatively impacted by reports of profit-taking by hedge funds. Despite this, the uranium spot price remains at levels not seen in 16 years, and the recent weakness does not indicate deterioration in the market’s strong underlying fundamentals, which are characterised by a structural supply deficit.

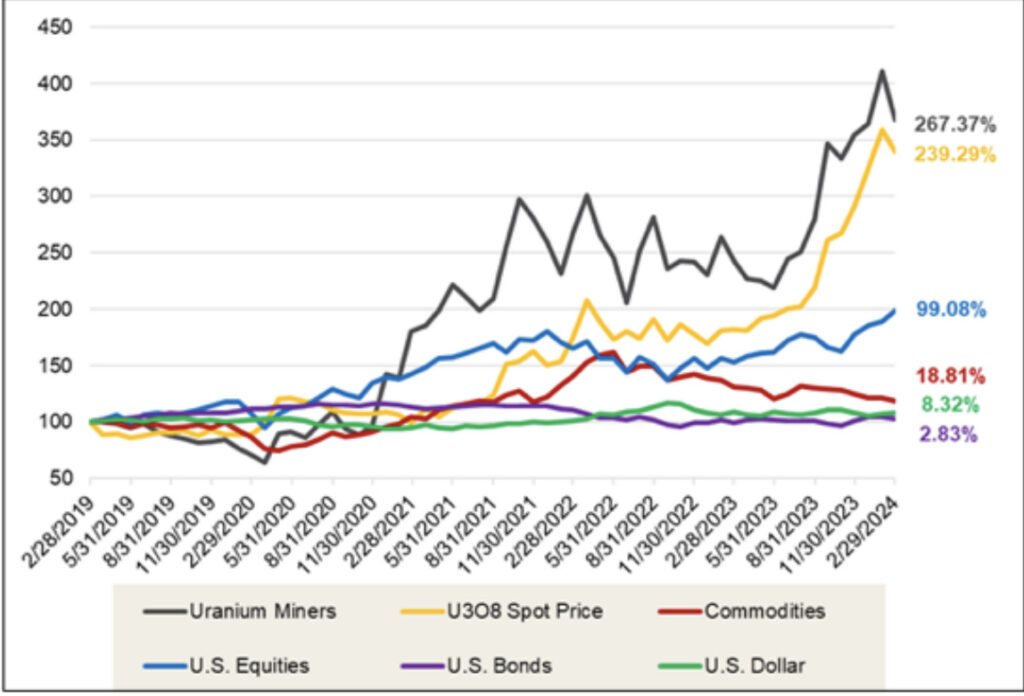

“Over the longer term, physical uranium and uranium miners have demonstrated significant outperformance against broad asset classes, particularly other commodities. For the five years ended February 29, 2024, the U3O8 spot price has risen a cumulative 239.29% compared to 18.81% for the broader commodities index.”

While spot prices dictate the headlines, term prices are arguably more important when it comes to uranium since they are the primary way utilities acquire materials from miners.

In other words, the term price more accurately reflects the prices producers will get paid for their uranium oxide.

White said that a term price of US$75/lb was a level not seen in 16 years, long before the Fukushima disaster, with ceilings at US$120/lb.

“This indicates strong future demand for uranium,” White argues.

On the supply side, an announcement the the world’s biggest producer Kazatomprom would fall 14% below its previous 2024 guidance was undercut by news Cameco was evaluating the expansion of its McArthur River mine in Saskatchewan from 18Mlb this year to 25Mlb when the time is right.

But White says contracting levels are a better pointer for future term price increases.

“While these potential production increases will help address the uranium supply deficit, they will not likely have an impact until many years from now,” he said.

“Cameco also highlighted a significant shift in the uranium market, with term contracting increasing from 124.6 million pounds of U3O8e in 2022 to 160.8

million pounds of U3O8e in 2023.”

This represents the highest global contracting rate in over a decade and nears “replacement rate contracting,” which aims to meet annual nuclear reactor fuel needs. Long-term contracting figures could climb further, as the previous cycle’s peak was 250 million pounds.

“Notably, Cameco also indicated that it has never been this early in the contracting cycle with prices as high as they are today. Finally, investors reacted negatively to Cameco downplaying the importance of the spot market, which many view as critical for pricing signals and transparency and where sellers and buyers meet continuously to contract.”

White views the recent dip as an ‘attractive entry point’ in light of the expected uranium supply deficit and a ‘moving target’ incentive price, saying restarts and new mine developments were needed to restock reactors in the coming years.

“The uranium price target as an incentive level for further restarts and greenfield development is a moving target, and we believe that we will need higher uranium prices to incentivise enough production to meet forecasted deficits,” he said.

“Over the long term, increased demand in the face of an uncertain uranium supply may likely continue supporting a sustained bull market.”

How’s this for your Wednesday? Not one but two M&A battles are heating up with Perseus Mining (ASX:PRU) finally getting the tail to wag the dog on its bid for OreCorp (ASX:ORR).

It’s placed the ball into TSX-listed Silvercorp’s court to match its bid after OreCorp’s board endorsed an upgraded offer from ORR from 55c to 57.5c a share — all cash — upping its valuation from $258m to $269m.

It comes after months of endorsements from the ORR board for a Silvercorp offer that comprised of 19c in cash per share and the balance paid in Silvercorp scrip.

The news comes one day after Perseus announced it had received Tanzanian competition approval for the bid, as long as it upped the Tanzanian Government’s stake in the actual prize — the proposed 200,000ozpa-plus Nyanzaga gold project — from 16% to 20%.

Crucially, Perseus has finally managed to turn two of the biggest and most influential players on the OreCorp register — mining bigwigs Nick Giorgetta and Tim Goyder — who collectively hold 15.6% of the company.

If Silvercorp can’t come up with something better, ORR’s board now intends to recommend people take the Perseus dough.

And it has a a lot of it. PRU is flexing its muscle after its 500,000ozpa-plus assets in West Africa propelled its cash balance to a wallet-splitting US$642m at December 31.

Speaking of West Africa and (not) flexing, one of the ASX’s saddest tales of 2024 is fighting an opportunistic takeover offer of its own.

Iluka Resources (ASX:ILU) spinoff Sierra Rutile (ASX:SRX) looked to be set for big things when it floated in 2022.

But a request from the Sierra Leone Government to end sweetheart tax agreements and revert its Area 1 natural rutile mine to previous standards the company said would make the mine uneconomic prompted the mothballing of its operations this year.

That has cast a shadow over its capacity to develop the longer life Sembehun discovery, expected to enter production later this decade.

Sierra Rutile is now subject to a 9.5c per share on-market takeover bid from PRM Services, an 11.46% shareholder of the company led by Craig Dean, the CEO of metals trading company and miner Gerald Group, which operates iron ore mines in Sierra Leone.

PRM, which has tapped Canaccord Genuity for the bid, said the bid represents a 21.79% premium for the distressed company, which has weathered a 66% share price decline in the past 12 months.

It has $41m capped SRX up over 30% today to 10c, having hit a high of 37c in August 2022 shortly after its demerger from Australian mineral sands and rare earths exponent Iluka.

SRX was acquired by Iluka in a disastrous 2016 transaction for $375 million along with $18m in transaction costs and the assumption of $80m in debt.

It booked a $421m impairment only three years later.

The SRX board have told shareholders to take no action in response to the bid, with King & Wood Mallesons and Gresham Advisory on board as its legal and financial advisors.

A continued rebound in iron ore prices to over US$106/t provided the steam for a 0.24% lift this morning for ASX materials stocks, with Fortescue (ASX:FMG) and Rio Tinto (ASX:RIO) among the top performers.

Uranium and coal stocks also lifted as higher gas and oil prices sent investors looking for cheaper alternatives.

New Hope Corp (ASX:NHC), Whitehaven Coal (ASX:WHC) and Deep Yellow (ASX:DYL) were all among the top large and mid-cap performers.

Mining

Mining

Mining

Get the latest Stockhead news delivered free to your inbox.