Canberra forecasters slash prices on nickel and lithium in new forecasts as resources earnings tipped to fall

Sierra Rutile fights back in mineral sands takeover tussle

Materials sector surges led by lithium companies and record gold price ahead of long weekend

Like a rug wholesaler in a cramped Malaga warehouse, Canberra has been forced to slash its predictions for Australia’s earnings on battery metals after a mammoth price slump that brought the sector to its knees in the back end of 2023.

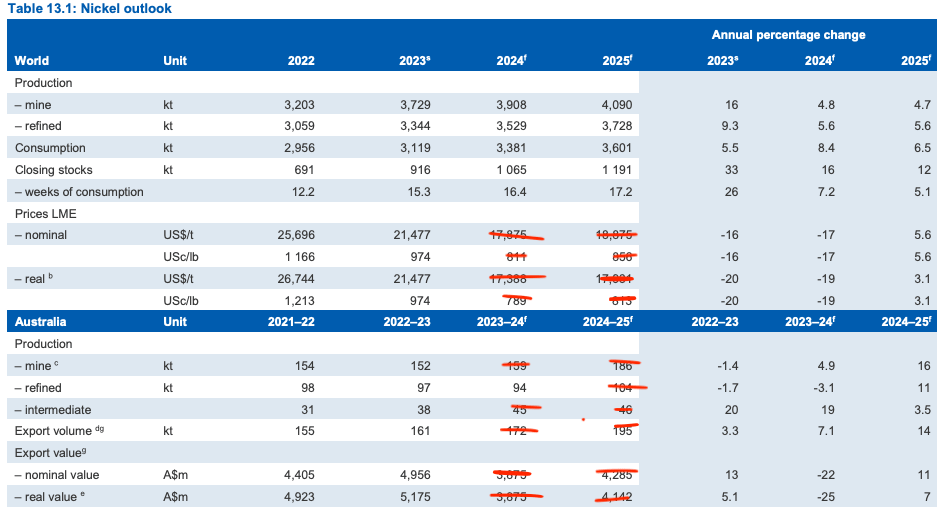

Nickel and lithium have borne the brunt of the revisions, slashed just months after pulling in record sales for the resource rich nation.

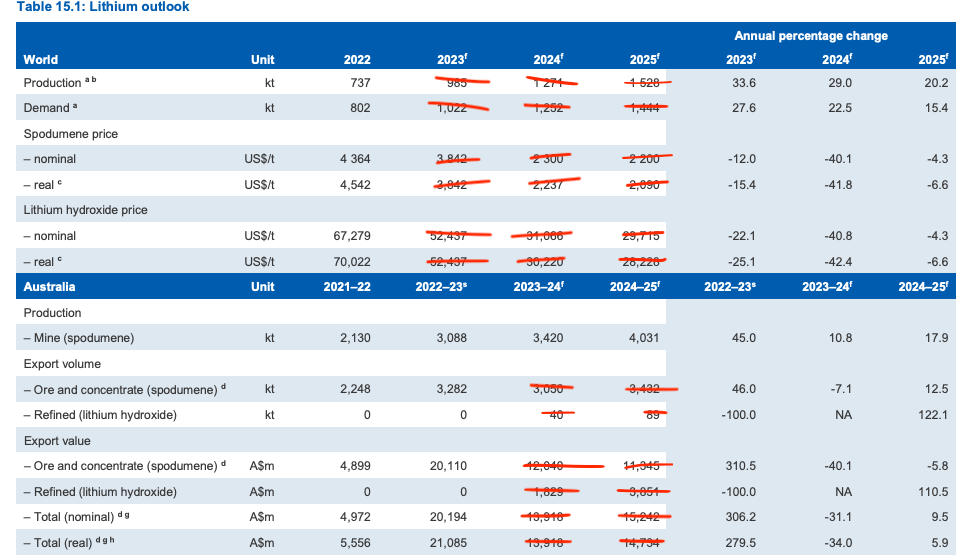

Lithium miners in WA earned over $20 billion from selling their wares in 2022-23, with nickel producers pulling in close to $5b.

That has been slashed in half with lithium miners now expected to draw $11.3b in revenue this financial year and just $9.4b in 2024-25 (though the full working out isn’t clear with conversion of spod to lithium hydroxide complicating things, it could be less).

Near and medium term price forecasts for 6% Li2O spodumene have been chopped from US$2300/t and US$2200/t in 2024 and 2025 in the December update of the Department of Industry, Science and Resources’ Resources and Energy Quarterly to US$1139/t and US$1379/t respectively.

Prices are forecast to fall to US$1210/t by 2029, with hydroxide projections pulverised from US$31,666/t and US$29,715/t in 2024 and 2025 to US$15,870/t and US$18,393/t respectively, falling to US$15,394/t by 2029.

It came after real world prices crashed in late 2023 and early 2024, with spot spodumene falling from US$8000/t in early 2023 to US$850/t before a recovery to ~US$1150/t in recent days, assisted by auction results from miners like Albemarle, Pilbara Minerals (ASX:PLS) and Mineral Resources (ASX:MIN) of small uncontracted cargos in a bid to achieve more ‘price transparency’.

Prices slashed across the board. Pic: Department of Industry, Science and ResourcesThe March outlook. Pic: DISR

It’s a similar story in nickel, where tumbling prices will not only hit miners’ bottom lines, but have already prompted around 40,000tpa of mined production to be shut down.

There remains a question mark over the future of BHP’s (ASX:BHP) Nickel West division, which contributes more than half of the nickel tonnes produced in Australia.

Canberra wasn’t as bullish on nickel, but it’s still copped a hiding with the red pen. Pic: DISRPic: DISR

Is there much hope for a turnaround?

Canberra forecasts nickel prices to stay below US$19,000/t due to excess global supply, promoted by a rush in production from State and Chinese supported miners and refiners in Indonesia.

Higher prices could support stronger production volumes, according to analysts from DISR’s Office of the Chief Economist, though at US$19,000/t or below prices would still be under the US$20,000/t BHP’s CEO Mike Henry recently cited as the break even point for the 80,000tpa Nickel West.

“Recent price falls have seen mine closures and reduced output announced by several Australian producers, as well as delays in planned projects,” analysts said in today’s report.

“This includes the closure of BHP’s Kambalda nickel concentrator, with the company update in mid-February indicating it was continuing to study a potential for a period of care and maintenance for its Nickel West operations.

“Australia’s mined output is expected to fall by 16% in 2024–25 to reach 129,000 tonnes, while refined output is projected to remain flat.

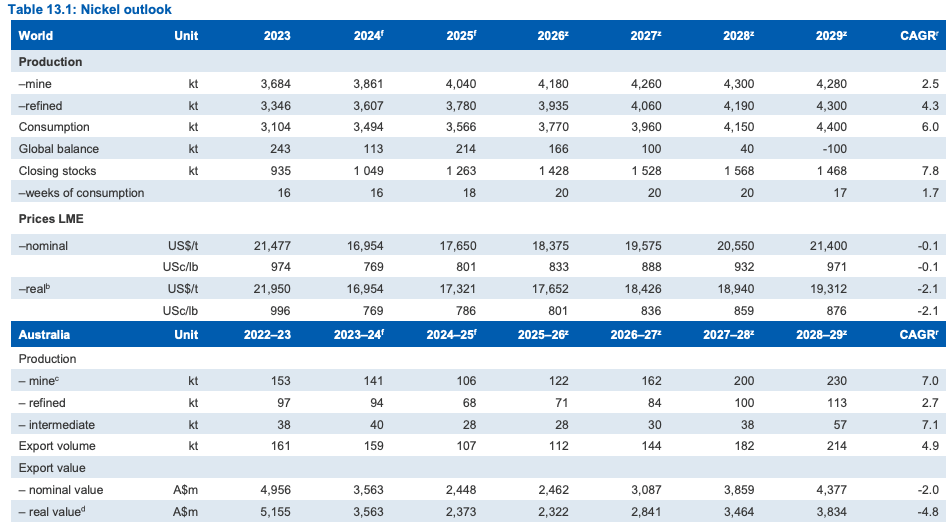

“Higher prices projected from 2026 are expected to support higher production volumes, with a number of projects set to come online in coming years. By the end of the outlook period, Australian mined nickel production is projected to grow to 230,000 tonnes in 2028–29, with new output from a number of large and mid-tier producers.

“This will include a number of new projects aiming to produce intermediate products (such as Mixed Hydroxide Precipitate) and nickel sulphate (an emerging alternative for feeding into the production of cathode materials for lithium-ion batteries).”

That projection would appear to factor in BHP’s on the nose $1.7b West Musgrave development as well as a number of uncertain laterite and sulphide projects. Ironically, high prices and enthusiasm about nickel’s value in EV batteries saw nickel and cobalt exploration hit a 15-year high of $325m in 2023, 55% up on 2018 spending.

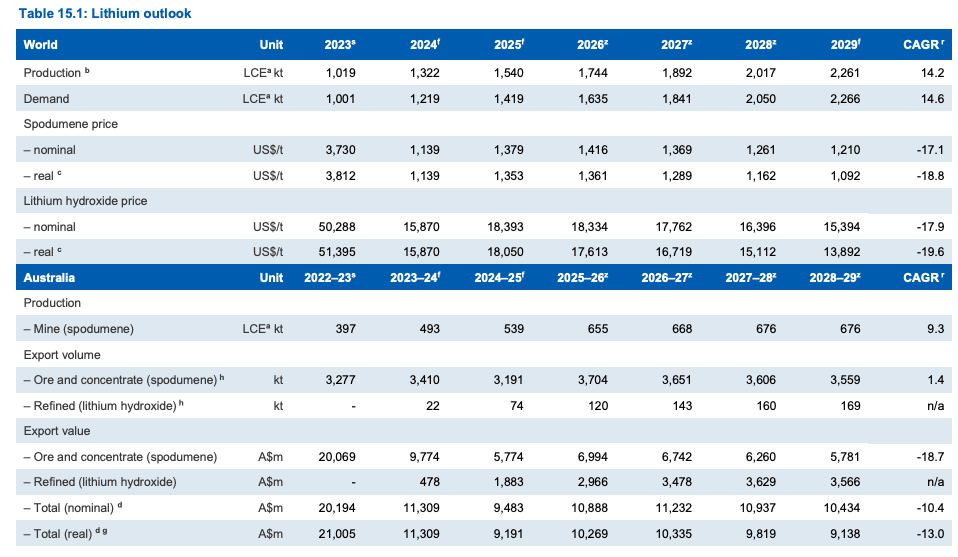

Despite lower prices, the office analysts still see a 70% rise in lithium production to 2029.

“Global lithium demand is projected to more than double between 2023 to 2029, driven by the rising adoption of electric vehicles,” they said. “However, evolving battery technologies could reduce lithium usage in batteries.

“Global lithium supply is projected to broadly keep pace with rising demand, with sizeable project pipelines among large producers (such as Australia and China) as well as among new and emerging producers (such as Argentina and Zimbabwe).”

By 2029 they say Australia will add more lithium supply than any other country, but rising competition will see its share of production fall from 46% to 32%, with Argentina and Zimbabwe to claim the greatest lift in global market share over the period.

What about the bigger picture?

When it comes to the bigger picture, the office’s analysts project resources and energy exports will fall in value from $466.3b in 2022-23 to $417.1b in 2023-24, $368.9b in 2024-25, $338.7b in 2025-26 and $336.1b in 2028-29, a CAGR of -5.3%.

In real 2023-24 money terms that’s $294.4b, a CAGR of -8%.

A big part of that is sliding energy earnings, with the end of post-Ukraine price spikes seeing oil, gas and coal earnings revert to normality.

Mined material earnings will stay relatively stable, rising from $227.6b in 2022-23 to $233.7b in 2023-24, before dropping to $205.2b by 2028-29.

Iron ore prices are projected to fall from US$103/t in 2023-24 to US$75/t by 2028-29, though Australian output will rise from 900Mt to 983Mt over that period, with export values falling from $129m last year to $83m by the end of the forecast period.

Among the most bullish projections is in copper, where prices are forecast to rise from US$8259/t this financial year to US$10,061/t by 2029, with export values lifting from $12b to $17b.

Sierra Rutile moves to fend off takeover

Sierra Rutile (ASX:SRX) says an on-market takeover offer from major shareholder PRM Services implies there is no value attached to its Sembehun project, one of the few natural rutile mines being prepped for development globally.

Sembehun will cost US$301m to build according to a capex figure floated from an upcoming DFS. That is US$36m down on a US$337m estimate compiled for a 2022 PFS run by the project’s former steward Iluka Resources (ASX:ILU).

SRX is the subject of both a 9.5c a share on-market takeover offer from PRM, a company owned by the CEO of commodity trader and Sierra Leone iron ore miner Gerald Group, Craig Dean, as well as a section 249D notice to roll most of the SRX board.

Contractor Mano Mining is also part of a group holding more than 10% of SRX which wants to have a nominated director appointed in the vote — former Beny Steinmetz Group diamond executive Jan Joubert.

Sembehun is the great long term hope for the dilapidated Sierra Rutile.

Now trading at 12c, its shares hit a high point of 37c shortly after demerging from Iluka Resources in August 2022.

They’re down 57.41% over the past year, and fell as low as 6c after SRX revealed it would be forced to shut its Area 1 operations after the Government of Sierra Leone informed SRX it would revoke tax concessions that made the project economically viable.

Sierra Rutile has also been subject to a number of legal proceedings in Sierra Leone, including a class action from local landholders.

But in a statement that shareholders take no action on what it described as an ‘inadequate offer’ from PRM, SRX criticised the bid for implying no value for the future Sembehun development and its ‘opportunistic nature’.

“We have formed the view that the Offer is opportunistic, inadequate and undervalues the Company, following the Board’s preliminary review of the unsolicited on-market takeover offer from PRM,” SRX chair Greg Martin said.

“PRM has opportunistically timed its Offer ahead of key value catalysts, such as the Sembehun DFS, and we do not believe it reflects Sierra Rutile’s significant strategic value as a major participant in the global mineral sands industry.”

The premium came in at a 21.79% premium to SRX’s pre-bid close of 7.8c and 24.71% premium to its three-month VWAP of 7.6c, but SRX claims it was at a 38.28% discount to its 12-month VWAP of 15.4c, though much of that trading took place before negative including the Area 1 tax dispute and subsequent mothballing.

SRX says it increased its cash on hand from US$7.8m to US$13m between December 31 and February 29 through a sell-down of zircon and industrial grade rutile inventories, and had US$64.2m in working capital available.

Located around 30km from Area 1, Sembehun is slated to extend SRX’s mine life by 13 years once developed.

Sierra Rutile (ASX:SRX) share price today

And on the market

The materials sector ratcheted higher, up 1.82% in a rally led by lithium, steel and base metals stocks.

It comes a day after reports broke that Albemarle had sold a cargo of spodumene at up to US$1300/t. Spod prices had collapsed to US$850/t in January.

Gold miners lifted strongly as well as LBMA gold prices hit an all time high of US$2193/oz, with coal producers Whitehaven (ASX:WHC) and New Hope Corp (ASX:NHC) up around 5%.

Profits at Chinese companies were also up 10.2% year on year in January and February according to the National Bureau of Statistics, though a low base in early 2023 was a culprit there.

Fixed asset investment and factory output rose ahead of expectations, ANZ’s Catherine Birch, Brian Martin and Daniel Hynes said in a note.

Get the latest Stockhead news delivered free to your inbox

For investors, getting access to the right information is critical.

Stockhead’s daily newsletters make things simple: Markets coverage, company profiles and industry insights from Australia’s best business journalists – all collated and delivered straight to your inbox every day.

Markets coverage, company profiles and industry insights from Australia’s best business journalists – all collated and delivered straight to your inbox every day.

It’s free. Unsubscribe anytime.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.

I want the news:

Hear it first

Get the latest Stockhead news delivered free to your inbox.

Thanks! You’re subscribed, Stockhead news is coming your way soon.