Pic via Getty Images

Top Resources 4: For this Kalgoorlie gold junior, being thick and shallow reaps rewards

Mining

Pic via Getty Images

Mining

Here are some of the biggest resources winners in early trade, Friday March 15.

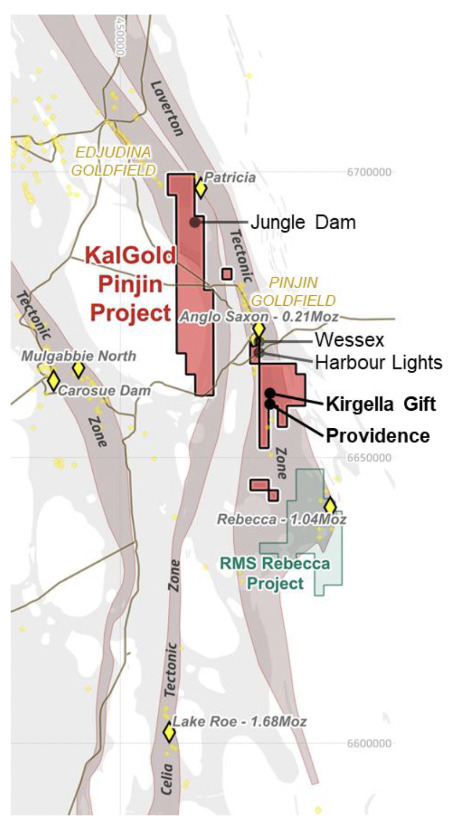

Sometimes in life, being thick and shallow reaps rewards. And it’s the case for minnow WA goldie KAL so far today.

It’s posting solid gains, thanks to thick and shallow gold intercepts at the Kirgella Gift and Providence prospects within the Pinjin project, around 140 km east of Kalgoorlie-Boulder.

Intercepts include: 32 m at 1.29 g/t Au from 3 m depth (containing 4 m at 3.29 g/t Au from 16 m); 35 m at 1.15 g/t Au from 11 m depth (containing 4 m at 2.91 g/t Au from 16 m); and 45 m at 2.36 g/t Au from 51 m depth (containing 33 m at 3.10 g/t Au from 51 m).

The gold hits are being compared with mineralisation hosted within larger, broader zones of anomalism at the Rebecca gold project 21 km to the south (of the KAL prospects), which is owned by Ramelius Resources (ASX:RMS).

This all comes amid a comprehensive appraisal of gold mineralisation completed at Kirgella Gift and Providence following successful drilling late 2023.

The company notes that three thick gold lodes have been recognised at Kirgella Gift, and two at Providence.

A program is now underway to advance to an initial JORC Code (2012) Mineral Resource Estimate at Kirgella Gift, with further drilling planned in Q2 at the broader Pinjin project.

Kalgoorlie Gold’s MD Matt Painter painted a picture with several words, including these ones:

“As gold prices surge, we believe that there is a clear pathway for KalGold to access its gold resources to realise maximum benefit for shareholders.”

KAL share price

BlackRock is busting up the local bourse. That’s right, not that BlackRock. The Tanzanian-focused, $76.8m market capped graphite player Black Rock Mining.

Why’s it double digits to the good this morn? It’s pulled in some pretty ginormous funding, in the form of a loan, for its flagship (84% owned) Mahenge graphite project in Tanzania.

Per a company release to the ASX, Black Rock has now secured key approvals for a targeted US$113m Term Loan for Mahenge, which it expects to comprise:

• US$59.6m from The Development Bank of Southern Africa (DBSA); and

• US$53.4m from the Industrial Development Corporation of South Africa (IDC)

It’s the IDC loan that it’s highlighting, however, and that’s a state-owned institution providing financial support to promote economic growth and development in South Africa. Clearly East Africa, too.

The DBSA, meanwhile is a prominent financial institution, wholly-owned by the government of South Africa.

In September last year, Black Rock signed an MOU with its POSCO International Corporation for a potential cornerstone equity position in Black Rock of up to US$40m. Approvals are reportedly closing in for this one.

Mahenge hosts a “multi-generational graphite resource” and, notes Black Rock, is one of the largest JORC-compliant flake graphite resources globally, with 213m tonnes at 7.8% TGC, and a reserve of 70m tonnes at 8.5% TGC.

Copper and gold explorer Xanadu Mines has several advanced exploration projects on the go in far-flung Mongolia, including in the South Gobi Desert.

According to it, it remains one of the few listed juniors that controls a globally significant copper-gold deposit – specifically at its flagship Kharmagtai project (a 3Mt copper and 8Moz gold Mineral Resource).

News sending it up and to the right today? Not seeing too much, although there was this post, which detailed a positive broker’s report on the stock from PAC Partners, who made a recent site visit to the company’s key project:

Post site visit, @PAC_Partners initiates on $XAM w 13cps target (26cps unrisked)#XAM continues 2 b fully funded @ both, corp lvl 4 discovery explor'n programs & Kharmagtai 50:50 JV lvl 2 complete PFS, with CF likely enhanced in early yrshttps://t.co/gLpuzcLp1q#ASX pic.twitter.com/3o2qoOVorY

— Xanadu Mines (@XanaduMines_ASX) March 14, 2024

The takeaways from that were…

It’s a “transformative year in prospect” at the company’s big South Gobi Copper/Gold project, with overall “robust value today” as well as the prospect of “project enhancement and corporate appeal in 2024”.

“We see Kharmagtai as a likely development project due to its large 1.25 billion tonne Resource at a grade of 0.27% copper and 0.21 gram/t gold,” wrote PAC Partners, adding:

“Over the life of mine, Kharmagtai is highly profitable with low all-in costs of US$1.87/lb on low strip ratio open pits and its South Gobi location’s surprising closeness to rail, power and to Chinese smelters.”

The broker’s investment view is: buy, with a $0.13 share price target in mind.

The current share price is below…

(Up on no news)

There’s not a lot doing in terms of news for this junior gold explorer.

It did deliver its half-yearly reports and accounts to market a few days ago, but it’s most recent news of importcame earlier this month and regarded its flagship Napié project in Côte d’Ivoire.

Two parallel artisanal mining sites named ‘Double Zone’ at Tchaga North within the Napié project have been seeing some good progress of late. It’s a target where high-grade rock chip samples have returned up to 22.46g/t.

Ongoing rock chip sampling program at the target area has pulled up another high-grade round of results – with the best of recent gold hits showing up to 79.5g/t in February.

Further rock chip sampling results at Double Zone has now expanded the drill target to 250m in strike length.

The very latest high-grade rock chip results include 22.46g/t Au, 16.78g/t Au, 12.85 Au, and 4.86g/t Au, which complement other recently announced results of 44.73g/t Au, and 6.29g/t Au.

Mako’s MD, Peter Ledwidge imparted the following thoughts:

“The newly named ‘Double Zone’ which is aptly named for the two parallel artisanal mining sites with associated east-west quartz veining, has expanded significantly.

“The consistent high-grade rock chip results at Double Zone along with its increasing strike length and width potential makes this a compelling high-priority drill target.”

At Stockhead we tell it like it is. While MKG is a Stockhead client at time of writing, it did not sponsor this article.

Get the latest Stockhead news delivered free to your inbox.