Pic: Via Getty

Remember 2019? The next boom for gold stocks could be just around the corner

Mining

Pic: Via Getty

Mining

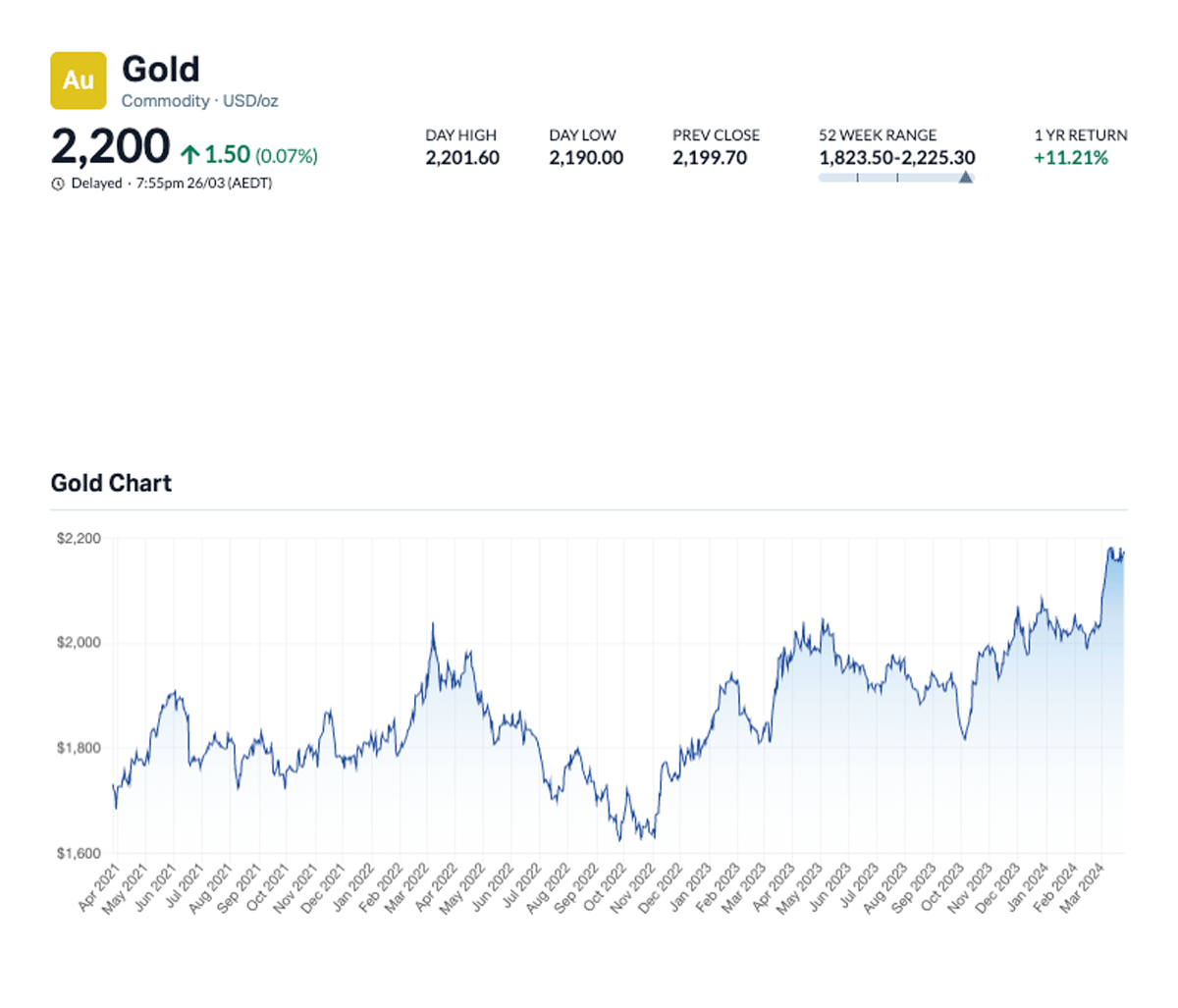

The mini gold boom between late 2018 and mid-2020 sparked a 70% increase in prices, from ~$US1200 to a peak of ~US$2050/oz.

Gold, and to a lesser extent silver, is used as a hedge in times of economic uncertainty.

During this period precious metals fervour was stoked by a troubled macro picture dominated by COVID, Brexit, trade wars, Hong Kong riots, and weakening global growth.

This was a wild time and frothy time for ASX miners, junior goldies, and their investors.

There were numerous success stories, like $2m capped, ‘bottom-of-the-drawer’ spec stock Spectrum Metals which, in Feb 2019, stumbled on bonanza grade gold at its Penny West project.

Ongoing drilling success (and some parabolic share price action) culminated in a friendly $230m takeover by Aussie mid-tier Ramelius Resources (ASX:RMS) early the following year.

Also in 2019, MetalsTech recorded the biggest one-day gain for an ASX stock – 500% — after announcing that it had signed an option agreement to acquire a gold project in Slovakia.

That was surpassed April 15 the following year by Predictive Discovery (ASX:PDI), which gained 733% on a new gold discovery in Guinea.

This time, investors are displaying a complete lack of interest in Aussie gold stocks even as the prices scaled all-time highs.

The divergence between the metal, which is up +30% from its November 2022 low of US$1640/oz, and stocks performance is puzzling the experts.

With prices expected to go higher in the mid-term, most agree this is a buying opportunity.

“I haven’t seen a greater disconnect between the #gold price and gold stocks in my career since the early ’70s. I have also not seen as much investor hostility to gold stocks, nor have I seen gold stocks at these valuation levels relative to book or relative to free cash flow.”

— Rick Rule Rhetoric (@RickRuleRulz) March 13, 2024

‘75% of advisors have little to no exposure in gold (<1% of assets) and low interest in adding any’ https://t.co/sfztODS9dc via @dailychartbook pic.twitter.com/W6KHhRnYv2

— Jesse Felder (@jessefelder) February 25, 2024

The ratio of gold stocks to gold just dipped below 0.1 for only the 3rd time in ~50 years. pic.twitter.com/Wd66E3uSUg

— Jason Goepfert (@jasongoepfert) March 5, 2024

“The malaise seems to be indiscriminate,” says Far East Capital Analyst and veteran stock picker Warwick Grigor.

“Many companies with interesting projects continue to fall in the market. Why is that?

“There is a strong probability that the market has a low level of confidence in many of the management teams, but the doesn’t explain why a well-managed company like Astral Resources is also being shunned.”

Maybe the market is tired of the same old stories and the failure of management to achieve commercial success, he says.

“Maybe investors should be looking for new stories without stale bulls who fill in buyers whenever they stick their heads up above the trenches.

“Maybe there are just too many companies to choose from, and not sufficient investable funds to take them higher. The frustration comes because there are more questions than answers.”

MineLife senior analyst Gavin Wendt says something similar.

“I think investors, to some degree, are still nervous about resource equities, including gold,” he says.

“The gold sector has disappointed over a period of a couple of decades in terms of investor returns and investors have a long memory,” he said.

WA broker Euroz Hartleys says escalating production costs could be to blame for lack of interest in the miners, but expects that to change very soon.

“We continue to see good value in gold equities currently lagging the gold price in both US$ and A$ terms,” it writes.

“This is somewhat explained by cost inflation severely impacting margins (wages, oil price and reagents), but more recently CY24 we are seeing gold price rise at the same time cost pressures appear to be easing.

“Expect equities to re-rate as stronger quarterlies are released for the MarQ.”

These production reports are by April 30.

Meanwhile the share prices of junior explorers, which often follow the lead of the producers, should benefit from expected strong profit margins.

In theory.

Sprott managing partner John Hathaway calls this disconnect between gold and share price performance “the greatest I’ve ever seen”.

He blames in increasing popularity of ‘passive investing’, whereby investors purchase a representative benchmark like the ASX200 index and hold it over a long time. Set and forget.

“…passive investing dominates the markets today and doesn’t favour smaller sectors,” Hathaway says.

“The market cap in the gold mining sector is about the same as that of Mastercard or Home Depot.”

Hathaway says gold miners should be buying back stock because they are “so ridiculously cheap”.

Stock buybacks can increase a company’s share price by reducing available shares on the market.

“There’s a better return on capital from share buybacks than investing in a big new mine,” Hathaway says.

“It’s a way of taking advantage of the fact that nobody cares.”

Who knows?

“One of my partners, way back when we started the gold fund 25 years ago, said, ‘The only reason anybody should own a gold stock is because they expect the gold price to go up’,” Hathaway says.

“He was right until now when that hasn’t been right. How much higher does the gold price need to go? I don’t know the answer.

“Is it $2,100? Is it $2,500?”

One thing is certain: at some point, higher gold prices “will lead to incredible cash flow and profitability so that even this tiny little space will catch somebody’s eye”.

“I noted recently that Stanley Druckenmiller, the legendary investor, has started to sell his Magnificent Seven stocks, and he’s starting to buy big-cap names like Newmont and Barrick,” Hathaway says.

“I’d like to think he’s right. He’s usually been right. I guess that there are still some value investors out there.”

The views, information, or opinions expressed in the interviews in this article are solely those of the interviewees and do not represent the views of Stockhead. Stockhead does not provide, endorse or otherwise assume responsibility for any financial product advice contained in this article.

Get the latest Stockhead news delivered free to your inbox.