Via Getty

Closing Bell: The local market just got its ASX handed back to it

News

Via Getty

News

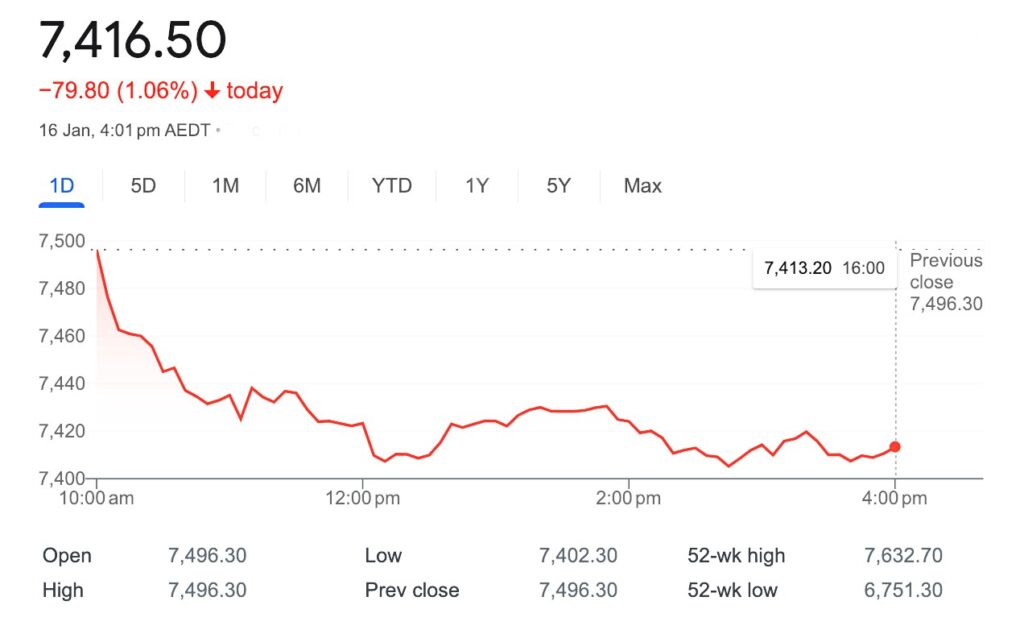

The ASX benchmark has ended Tuesday as it began, which is badly.

Just after lunch, the ASX200 ran into the teeth of a one-month low, after spending the last five fruitless sessions of trade at or near parity.

At 4pm on Tuesday, the S&P/ASX200 closed down 80 points or 1.05% to 7,416.5

There was, however, some winning going on somewhere – because at about the same time in Iowa, USA, ex-president Donald Trump was looking a shoe-in to set a record for securing that states’ Republican caucus with a margin of victory exceeding the circa 13 percentage points Bob Dole won Iowa by way back in 1988.

Back to local business. As soon as the bell rang Aussie stocks got back to the kind of broad based, agnostic selling which heralded the new year.

Aussie consumer sentiment is at profound lows, the Westpac-Melbourne Institute index says.

And it showed out there on the park today fellas.

An absent US lead left local traders in the hands of European markets where the central bank spent the evening busily assuring markets not to hope for any change to the ECB’s hawkish outlook.

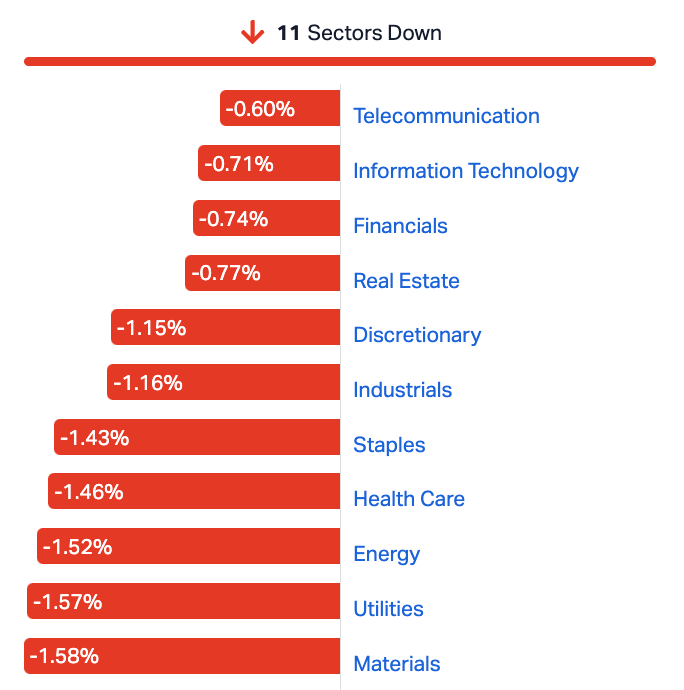

The benchmark began taking in water as the heavyweight names in the heavyweight Materials sector floundered, dragged down by commodity prices and hitting levels last seen in early December.

When BHP falls 1.1%, the broader market gets wet.

Iron ore futures remain near six-week lows, despite the spot price in Singapore and Dalian making incremental gains during the Tuesday seesion in Sydney.

On this, CBA’s Vivek Dhar knows much.

The last time that steel margins in China ‘s mills were this negative, Vivek says, was June 2022, when iron ore prices eventually fell below $US100/t.

“The current downward correction in iron ore prices could threaten the same level temporarily, too.

“However, once steel mill margins stabilise, we think iron ore prices are likely find support in the $US100‑$US110/t range, waiting in anticipation for China’s policy direction for 2024,” Mr Dhar adds.

“We think it is likely that China’s property sector, which likely accounted for 30‑35% of China’s steel demand last year, will continue to face headwinds in 2024.”

That’s also hit the Aussie dollar, everyone’s least favourite proxy for commodity markets. It’s down about 1% against the greenback and about 5% over the last 12 months.

Finally, unnamed supermarkets are being told that they mustn’t make so much money from bleeding suppliers and customers.

Two random stocks which may’ve been caught up in that particular regulatory tweak include Coles Group (ASX:COL) and Woolworths (ASX:WOW), both shorter about 2%.

Around the ‘hood, the Shanghai Composite was flat and the tech heavy Shenzhen Component slightly lower at around lunchtime on Tuesday.

That’s not the progress Beijing would like to see with both the mainland benchmarks wallowing at multi-year lows.

It’s a big week for China’s economic recovery which remains pregnant with potential but little as thanks to policy uncertainty and investor scepticism ahead of Wednesday’s GDP drop.

Getting her 2 cents in on China from the safety of the World Economic Forum in Davos, Switzerland, was Kristalina Georgieva, the head of the International Monetary Fund (IMF) who told China to go get some structural reforms unless it wants “a fairly significant decline in growth rates”.

Speaking to CNBC, Georgieva said China was facing both short-term and long-term challenges.

In the short-term, she said China’s property sector still needed “fixing,” along with a high level of local government debt. Longer term, Georgieva noted demographic changes and a “loss of confidence”.

“Ultimately, what China needs are structural reforms to continue to open up the economy, to balance the growth model more towards domestic consumption, meaning create more confidence in people, so [they] don’t save, they spend more,” Georgieva said.

On Monday, the PBOC kept its one-year medium-term lending facility rate unchanged at 2.5%, disappointing markets, developers and various investors hoping for further policy easing.

And hey, in Tokyo, The Nikkei 225 has retreated about 0.5% on Tuesday at lunch, which means goodbye to the ridiculous 34-year high the major Japanese benchmark’s hit on Monday.

They’ll be back despite Japanese traders feeling the angst as global economic uncertainties weighed on sentiment.

Meanwhile, well over 60% of Iowa Republican caucus-goers told a Reuters poll that they don’t believe US President Joe Biden actually won the 2020 presidential election.

Only 30% of respondents believed Biden won the election fair and square, while 65% said they think Biden didn’t win legitimately, according to the survey of 551 GOP caucus attendees.

64% of caucus-goers reckon Donald Trump would be fit to return to the White House even if he were convicted of a crime, according to an NBC entrance poll.

Just 31% of respondents said Trump would not be fit to serve in the White House if convicted of a crime.

US media has projected that former president Donald Trump has already won.

After the Martin Luther King Day break, US Futures for the three major Wall Street indices fell rather precipitously after the long weekend as investors prepared themselves for reruns of higher-for-longer interest rate trading conditions and ahead of key retail sales data.

Today’s best performing small cap stocks:

Swipe or scroll to reveal full table. Click headings to sort:

| Code | Company | Price | % | Volume | Market Cap |

|---|---|---|---|---|---|

| KNB | Koonenberry Gold | 0.081 | 47% | 394,906 | $6,586,200 |

| MHC | Manhattan Corp Ltd | 0.0055 | 38% | 118,615,693 | $11,747,919 |

| CYQ | Cycliq Group Ltd | 0.004 | 33% | 100,647 | $1,072,550 |

| PKO | Peako Limited | 0.004 | 33% | 95,000 | $1,581,254 |

| TAR | Taruga Minerals | 0.009 | 29% | 949,392 | $4,942,187 |

| MEL | Metgasco Ltd | 0.01 | 25% | 69,648 | $8,511,094 |

| AMM | Armada Metals | 0.031 | 24% | 184,250 | $5,200,000 |

| ERA | Energy Resources | 0.073 | 24% | 10,100,352 | $1,306,749,652 |

| BMG | BMG Resources Ltd | 0.016 | 23% | 24,479,499 | $8,239,363 |

| LVH | Livehire Limited | 0.051 | 21% | 127,945 | $15,305,392 |

| HTA | Hutchison | 0.036 | 20% | 30,200 | $407,175,257 |

| RDS | Redstone Resources | 0.006 | 20% | 105,000 | $4,606,892 |

| TSL | Titanium Sands Ltd | 0.013 | 18% | 1,136,507 | $21,931,032 |

| FFG | Fatfish Group | 0.04 | 18% | 16,269,620 | $47,268,149 |

| MHK | Metalhawk. | 0.14 | 17% | 146,072 | $11,929,734 |

| AD1 | AD1 Holdings Limited | 0.007 | 17% | 238,803 | $5,391,890 |

| AHF | Aust Dairy Limited | 0.014 | 17% | 57,714 | $7,870,402 |

| TX3 | Trinex Minerals Ltd | 0.007 | 17% | 4,022,234 | $8,922,148 |

| CHW | Chilwa Minerals | 0.1625 | 16% | 11,400 | $6,422,500 |

| ZAG | Zuleika Gold Ltd | 0.022 | 16% | 2,345,589 | $13,985,625 |

| L1M | Lightning Minerals | 0.115 | 15% | 4,950 | $4,222,506 |

| HLX | Helix Resources | 0.004 | 14% | 3,667,411 | $8,131,010 |

| KLI | Killi Resources | 0.064 | 14% | 64,930 | $3,336,203 |

| VMS | Venture Minerals | 0.008 | 14% | 14,361,379 | $15,470,091 |

| GW1 | Greenwing Resources | 0.125 | 14% | 60,792 | $19,167,663 |

Koonenberry Gold (ASX:KNB) dropped an announcement this morning that final approvals have been received for the maiden drilling program at its Atlantis Au-Cu Prospect, and “as soon as weather conditions permit” they’ll get the drills spinning to conduct first pass Air Core drilling at the site.

“The Atlantis outcropping copper-gold mineralisation, copper-gold soil anomaly, geophysical targets, structural and geological setting make Atlantis a compelling target,” KNB MD Dan Power said.

“Whilst this prospect has been known about for some years, Koonenberry Gold has advanced it to drill-ready status and will be the first ever exploration company to conduct drill testing.”

Presumably he means at that particular site, but you get the idea.

KNB also has assay results incoming from its Bellagio project, which the company says are “anticipated soon”.

Later in the day, White Cliff Minerals moved towards the top of the ladder again, following on from yesterday’s news that it’s all set to acquire a historical uranium project in the Northwest Territories of Canada called Radium Point.

The investor presentation it delivered this morning re-stating that news and giving a brief update on how the company’s travelling was just the shot in the arm it needed to resume its shuffling towards a nicely fattened purse.

BMG Resources (ASX:BMG) dropped a bit of a bombshell in the morning, fuelling a major surge in volume and pushing its price up more than 23% with news that long-time MD Bruce McCracken has resigned from BMG and all of its subsidiaries.

With McCracken gone, non-executive director John Prineas assumes the role of non-executive chairman, while non-executive chairman Greg Hancock transfers to the role of independent non-executive director.

Prineas steps into the role with a host of other responsibilities on his plate as well – he’s currently BMG’s largest shareholder (holding 9.8%), and is also the founder and executive chairman of St George Mining (ASX:SGQ) and founder and a non-executive director of American West Metals (ASX:AW1) .

As it stands with BMG, Prineas is set to assume day-to-day responsibilities for BMG matters, until a new CEO or MD is appointed to the role.

There were a bunch of small caps moving around for reasons probably known only to them – that included Firebird Metals (ASX:FRB), clawing back some of the ground that it lost late last week, and Fatfish Group (ASX:FFG) which was lurching around like it often does, so no huge surprise there, really.

Chilwa Minerals (ASX:CHW), PVW Resources (ASX:PVW) and Metal Hawk (ASX:MHK) were also heading north in the morning, without any announcements providing information about why.

And Aerometrex (ASX:AMX) delivered a quarterly before lunch, bearing upbeat news for investors – the company expects to deliver a record first half (1H) revenue outcome, driven by “strong ongoing performance of the LiDAR and MetroMap product lines”.

AMX reckons it’s likely to post a group revenue in the $11.8-$12.2 million range, which is a tidy climb from the previous years’ $10 million high water mark.

Today’s worst performing small cap stocks:

Swipe or scroll to reveal full table. Click headings to sort:

| Code | Company | Price | % | Volume | Market Cap |

|---|---|---|---|---|---|

| JAV | Javelin Minerals Ltd | 0.001 | -50% | 2,000 | $3,267,458 |

| CPO | Culpeo Minerals | 0.048 | -38% | 32,866,202 | $10,474,677 |

| PUA | Peak Minerals Ltd | 0.002 | -33% | 208,333 | $3,124,130 |

| 8IH | 8I Holdings Ltd | 0.012 | -29% | 63,145 | $6,075,052 |

| ME1 | Melodiol Global Health | 0.0015 | -25% | 17,200,277 | $9,457,648 |

| NVQ | Noviqtech Limited | 0.003 | -25% | 10,006 | $5,237,781 |

| YOJ | Yojee Limited | 0.003 | -25% | 2,949,534 | $5,223,941 |

| NKL | Nickelxl | 0.038 | -21% | 758,308 | $4,215,128 |

| BCT | Bluechiip Limited | 0.012 | -20% | 1,114,955 | $11,930,607 |

| ATH | Alterity Therapeutics | 0.004 | -20% | 8,449,187 | $19,056,631 |

| CHK | Cohiba Min Ltd | 0.002 | -20% | 581,310 | $6,325,575 |

| ESR | Estrella Resources | 0.004 | -20% | 55,500 | $8,796,859 |

| HCD | Hydrocarbon Dynamic | 0.004 | -20% | 1,263,400 | $3,848,330 |

| KPO | Kalina Power Limited | 0.004 | -20% | 651,045 | $11,050,640 |

| TMG | Trigg Minerals Ltd | 0.008 | -20% | 326,029 | $3,747,562 |

| BNR | Bulletin Resources | 0.105 | -19% | 1,242,667 | $38,169,732 |

| UBN | Urbanise.Com Ltd | 0.3 | -19% | 5,374 | $23,746,789 |

| A3D | Aurora Labs Limited | 0.027 | -18% | 1,568,877 | $9,557,066 |

| KOR | Korab Resources | 0.015 | -17% | 268,349 | $6,606,900 |

| SCT | Scout Security Ltd | 0.015 | -17% | 5,000 | $4,183,693 |

| 1MC | Morella Corporation | 0.005 | -17% | 30,087,931 | $37,072,797 |

| BPP | Babylon Pump & Power | 0.005 | -17% | 1,500,800 | $14,979,884 |

| HOR | Horseshoe Metals Ltd | 0.005 | -17% | 1,047,807 | $3,878,872 |

| HXG | Hexagon Energy | 0.01 | -17% | 225,400 | $6,154,991 |

| IEC | Intra Energy Corp | 0.0025 | -17% | 2,436,000 | $4,982,345 |

Rex Minerals (ASX:RXM) – pending an announcement by the company in relation to a proposed capital raising.

MetalsTech (ASX:MTC) – pending *deep breath* “detailed submissions (specifically ASX Listing Rules Chapter 11 – ‘Significant Transactions’) [to be] made to the ASX in relation to the potential transaction with Trans Metal Fund LP for the 100% acquisition of the high-tonnage, high-value underground-only Gold-Silver mining operation at the 100%-owned Sturec Gold Mine in Slovakia.

PhosCo (ASX: PHO) – pending an announcement by the company to the market regarding a capital raising.

Get the latest Stockhead news delivered free to your inbox.