Pic: Stevica Mrdja / EyeEm / EyeEm via Getty Images

This asset manager says post-COVID boom times ‘may be behind’ small caps

Experts

Pic: Stevica Mrdja / EyeEm / EyeEm via Getty Images

Experts

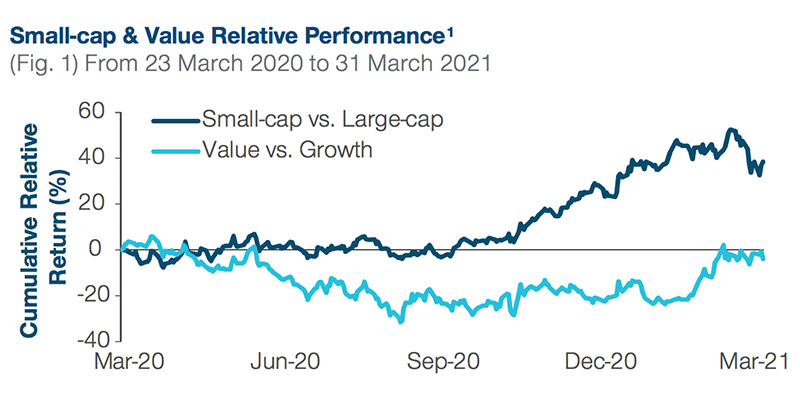

For small cap investors, asset manager T.Rowe Price has a useful chart on the post-COVID boom times:

The dark blue line shows small cap returns have outperformed larger stocks by as much as 50 per cent since the crisis hit.

Small-cap data is represented by the US Russell 2000 Index, but it’s been a similar story on the ASX leading up to the February peak.

And for now, equity markets are still “riding higher on unwavering optimism”, T.Rowe Price said as part of its April markets outlook.

There are plenty of reasons to stay bullish. All domestic indicators point to a strong economic recovery, while the RBA remains ultra-supportive.

Globally, investors are watching the US for any signs that the Biden administration will secure the passage of a major infrastructure spending package.

But with strong gains locked in across multiple small cap sectors over the last six months, T.Rowe Price also provided some insights around portfolio balance and risk management for the year ahead.

For starters, the analysts applied their sector view within the context of historic economic rebounds.

Smaller companies “tend to lead early in an economic recovery given their higher sensitivity to growth,” T.Rowe Price said.

And in the post-COVID snap-back, “the fast and furious pace of performance stands out”.

In contrast, larger companies typically require more concrete evidence of economic growth before climbing.

That situation has played out on the ASX, with larger players such as the big banks only starting to pick up steam in the early part of this year.

The trends that underpinned the small-cap surge — government stimulus, market liquidity and strong economics growth — are still in place.

But factoring in the capacity of small-caps to act as a leading indicator, “a lot of the outperformance may be behind” the sector, T.Rowe Price said.

“While smaller companies may continue to benefit from aggressive fiscal and consumer spending, valuations in some sectors are getting rich.”

Conversely, the prospect of higher rates — which first jolted markets in February — and a big new infrastructure push saw the fund manager pick a side in the growth vs value debate.

“After nearly a decade of underperformance, perhaps this cyclical rally may be enough for value to close the gap versus growth stocks,” T.Rowe Price said.

Elsewhere, the analysts said investors should at least factor in a copule of instances where things have gotten a little weird on global markets as part of their risk management framework.

House prices a surging, Bitcoin has gone parabolic while activity surged in SPACs — the latest finance invention to come out of US capital markets.

US stocks have also easily surpassed their pre-COVID highs, while the ASX is closing in.

Despite those “pockets of froth”, investors have show far shown “no concern” about a big pullback.

However, “it’s hard to ignore events such as the retail-based GameStop short squeeze and enormous losses at Archegos Capital, a large private family office, which may have historically shaken the confidence of equity investors”, TRP said.

So far, those market ructions have largely been viewed as “idiosyncratic”, the analysts said.

However, it will be worth paying attention whether that trend of unusual events continues in the year ahead, as a precursor to possible systemic market corrections.

“Perhaps the systemic risk is already here, with the threat of even higher rates, inflation, and now taxes,” TRP concluded.

Get the latest Stockhead news delivered free to your inbox.