Pic: Via Getty

Guy on Rocks: Who’s ready to ride the porcelain bus with Dundas Minerals?

Experts

Pic: Via Getty

Experts

‘Guy on Rocks’ is a Stockhead series looking at the significant happenings of the resources market each week. Former geologist and experienced stockbroker Guy Le Page, director, and responsible executive at Perth-based financial services provider RM Corporate Finance, shares his high conviction views on the market and his “hot stocks to watch”.

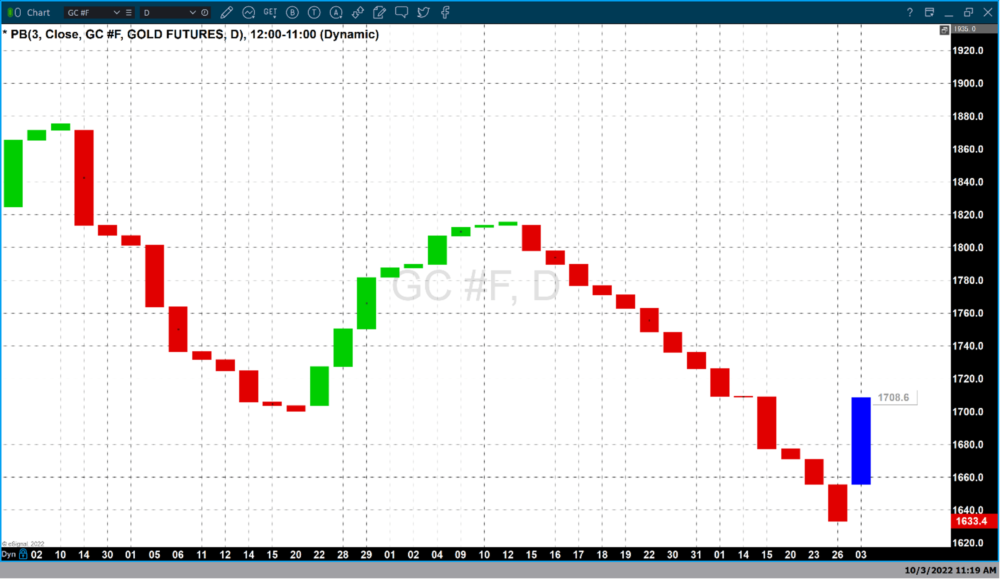

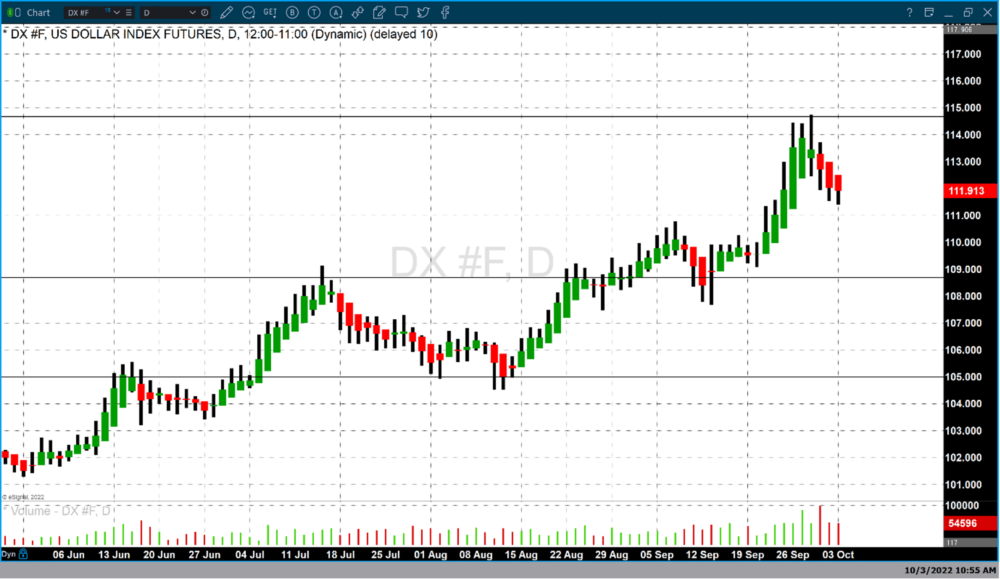

Gold has rebounded strongly over the last few days bouncing off its recent lows and is now trading at just over US$1,700/ounce (figure 1) after a week of extreme volatility that saw the USD index hit a 20-year high of 114.6 (figure 2).

The USD index is now sitting at 111.58. US 10-year treasuries also came off from 3.829% to 3.642% during the week.

Other currencies were equally volatile with the British pound last week being thumped to just over $1.03 representing an all-time low against the USD as the UK government averted a liquidity crisis.

The Bank of England implemented a two-week purchase program (£45b) for long dated bonds with a deferral of gilt sales to late October 2022.

The sell off in the bond market followed the government’s announcement of what appears to be unfunded tax cuts. One can only imagine what this is going to do for inflation.

UBS see a mixed outlook for commodities with base metals and bulks likely to drift lower but lithium, coal, aluminium, zinc, and lead on changing to remain elevated due to supply tightness.

Not surprisingly they are anticipating commodity demand to slow over the next six months.

The mixed supply outlook over the next 12 months however is likely to see copper, iron ore & PGMs to lift. They consider iron ore miners such as Rio and BHP are pricing in ~US$78-86/tonne (62% fine) implying further near-term price falls.

Copper was up last week over 2% to US$3.49/lb but remains heavily in in backwardation despite record low inventory levels in Shanghai and aggressive copper restocking in China.

Uranium was down 2% last week at US$48.5/lb with the Democrats last week attempting to block US$1.5 billion of funding for a US stockpile for enriched uranium which is currently 25% dependant on imports from Russia and 40% dependent on enriched uranium from Russia.

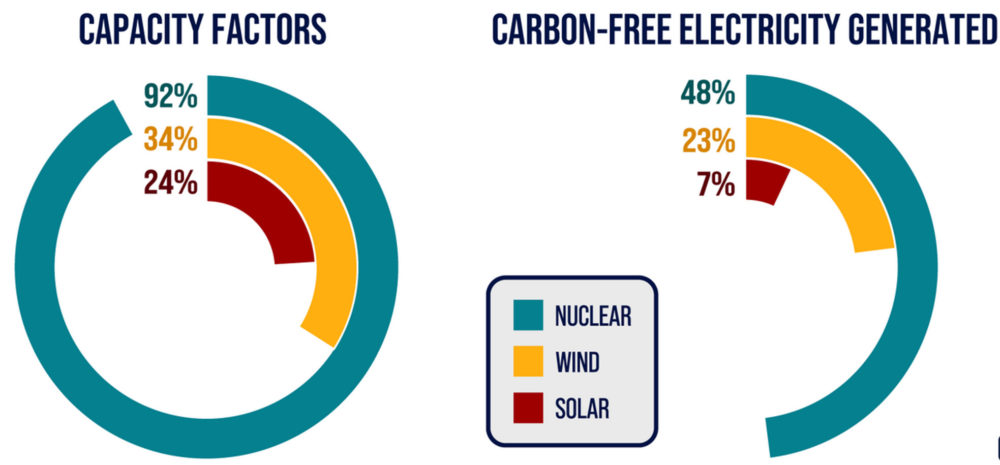

For those who have been brainwashed by bad science into thinking carbon free is the way to go, nuclear looks like a good option (figure 3).

It’s worth taking note of my Doomsday Prepper friends in such markets to get a taste of what is in front of us particularly when you see the Federal Reserve looking to tame inflation to 2% while still buying their own debt.

One of my colleagues from Adelaide University, Douglas Orr, CFA from Endeavour Equities, is one such prepper.

Doug was a standout at University (drank in moderation, went to lectures and was respectful towards other binary and non-binary wildlife at the University college).

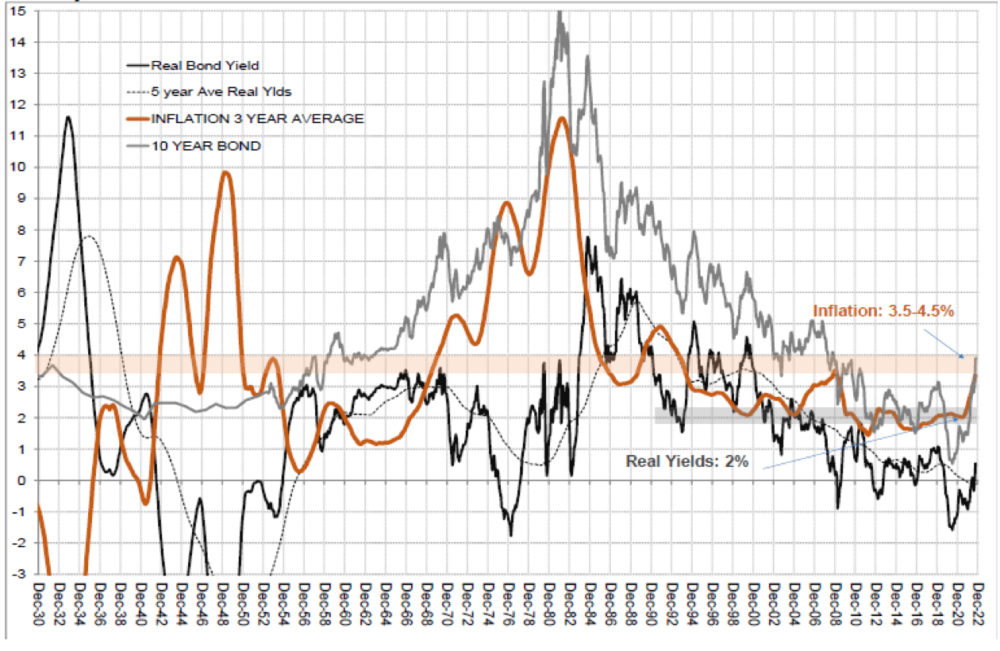

His base case scenario revolves around a hard landing which has been in the case in 7 out of 7 cycles since 1960 with inflation persisting/entrenched and projecting 10-year US Treasury yields to top out at 5% (figure 4).

And the news gets even better with a recession in the US, rent, wages and labour inflation, higher costs, a dramatic fall in housing affordability and 15% earnings downgrades moving into CY 2023.

Check out the following historical records:

So, does today’s lift in the ASX represent a bear market rally?

More than likely but the good news for the Stockhead faithful is that current resource valuations (at least across the large caps and mid-tier) are reflecting a 15% downward revision of earnings into next year; broker valuations from what I have seen are somewhat optimistic.

Some good quality small caps we have mentioned here also represent good value. KRM, NXM, RIE, SXR and the list goes on….

Many of the Stockhead faithful will have fond memories of some great nickel discoveries here in the West over the last 30 years or so including the Cosmos Nickel Project (Jubilee Mines Ltd – 1997) in the Yilgarn and more recently the Nova-Bollinger Ni-Cu-Co Project (Sirius Resources Ltd in 2012) in the south-west (Albany Fraser Range).

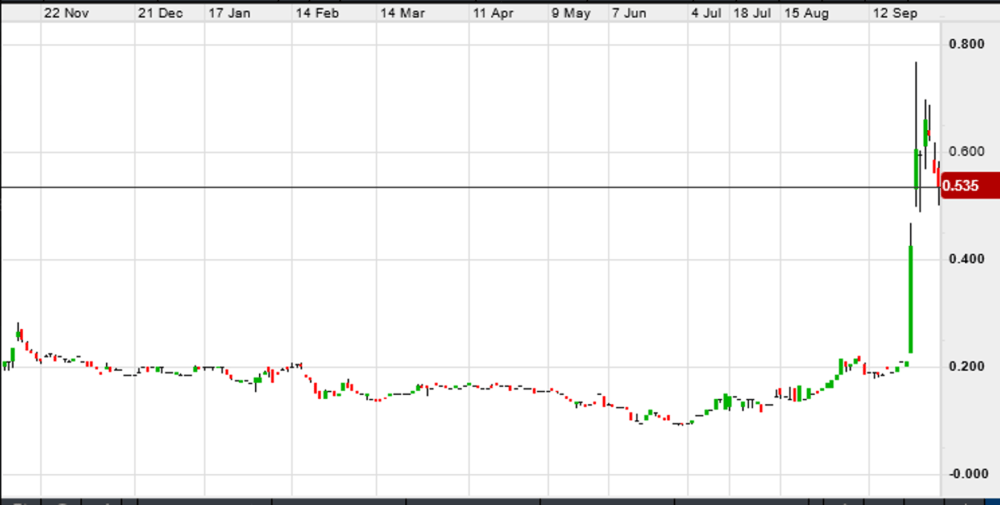

Dundas Minerals (ASX:DUN) (figure 5) looks like they have stumbled on some elevated copper-nickel-cobalt-silver mineralisation while drilling a long drop (or bush dunny to the uninitiated).

(JFC – a toilet, then.)

We have all heard the medical advice for over 50s after ripping one off to “look behind you”, however the reason we do that in mineral exploration is to see what is at the bottom of the hole.

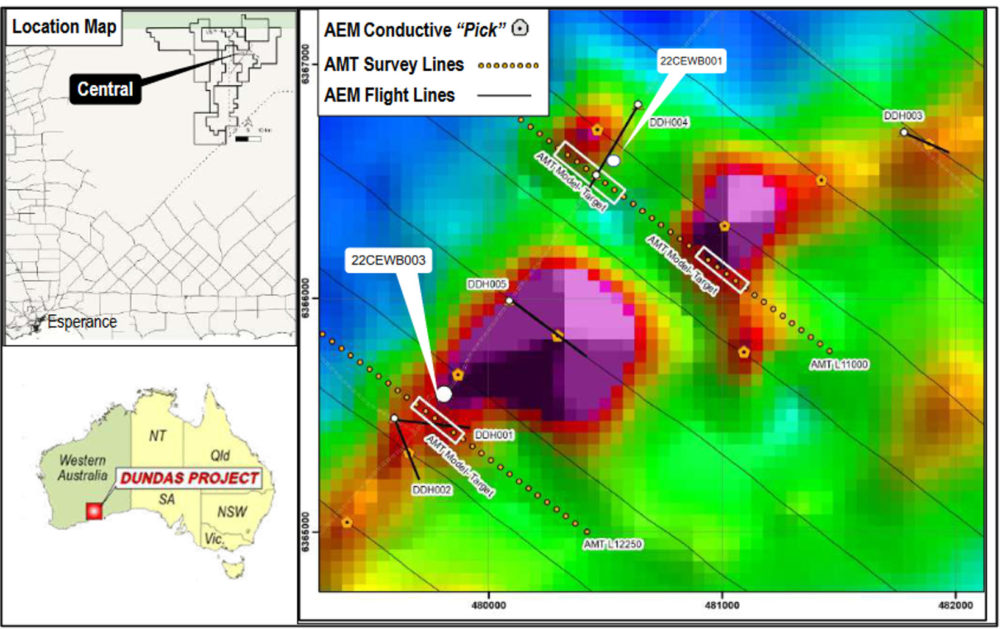

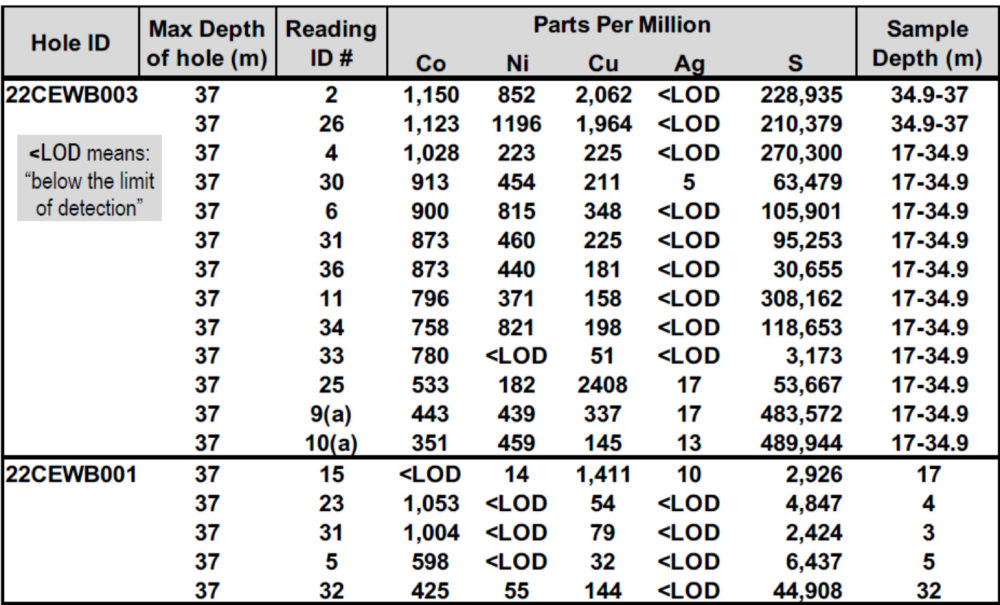

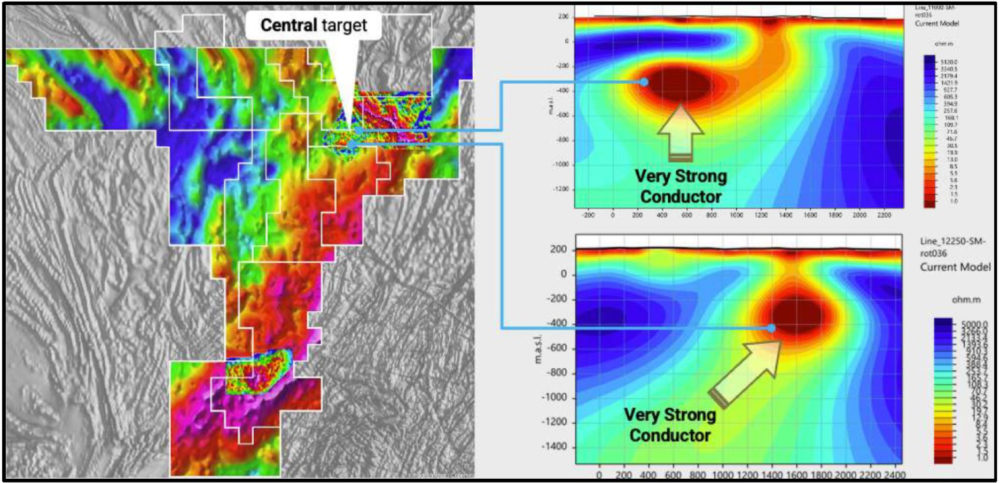

Turns out the Rotary Air blast “dunny hole” returned (table 1) some elevated grades (using a portable pXRF machine) from 17 metres downhole coincident with a 450 metre long AMT anomaly (audio magneto tellurics for the great unwashed).

Fortunately, this was identified before the dunny commissioning. I am not sure about the claim of massive sulphides however the rocks are at least blebby and disseminated, look like ultramafics and are full of sulphides so that is a good start.

What this metal assemblage means and how extensive the mineralisation remains to be seen is unknown, however I like the address, and the look of the rocks.

The company is due to receive assays on these two RAB holes shortly and is now in the process of RC and diamond drilling some of the AMT targets at the Central Prospect (figure 7).

Obviously the proof will be in the assays however at an enterprise value of $36 million (undiluted), circa $2.5 million in cash and 14 million in the money options to fund exploration over the next 6-9 months, the company remains in good shape.

DUN could be quite a ride in the short to medium term.

Spare a thought for former DUN geologist Mike Northcott (who was marginally less disgraceful than me at Adelaide University) who recently retired and was last seen eating kale and doing pilates in Byron Bay.

He might need to return and lay claim to a discovery before the year is out…

At RM Corporate Finance, Guy Le Page is involved in a range of corporate initiatives from mergers and acquisitions, initial public offerings to valuations, consulting, and corporate advisory roles.

He was head of research at Morgan Stockbroking Limited (Perth) prior to joining Tolhurst Noall as a Corporate Advisor in July 1998. Prior to entering the stockbroking industry, he spent 10 years as an exploration and mining geologist in Australia, Canada, and the United States. The views, information, or opinions expressed in the interview in this article are solely those of the interviewee and do not represent the views of Stockhead.

Stockhead has not provided, endorsed, or otherwise assumed responsibility for any financial product advice contained in this article.

Get the latest Stockhead news delivered free to your inbox.