Mining

Monsters of Rock: Northern Star defends hedges as gold prices spike; Metals Acquisition bats off M&A talk

News

ASX Small Caps Lunch Wrap: Arise Sir Risk-On, as punters leave gold to flail and oil to ail

Mining

Via Getty

Experts

Guy on Rocks’ is a Stockhead series looking at the significant happenings of the resources market each week. Former geologist and experienced stockbroker Guy Le Page, director, and responsible executive at Perth- based financial services provider RM Corporate Finance, shares his high conviction views on the market and his “hot stocks to watch”.

Gold closed the day at US$1,912/ounce off US$10 during the day ahead of the Federal Reserve meeting on Tuesday (ends Wednesday) with the market pricing in a 25-basis point interest rate rise following on from the 50 basis point hike last December. Gold remains in a three-month uptrend with US$2,000 the next hurdle.

Aside from this, not a great deal of economic data out this week however OPEC is meeting on Wednesday with crude oil trading just under US$80/bbl to close at US$79.50/bbl. The USD index was also slightly weaker with US 10-year Treasuries trading at 3.551%.

All eyes remain on China to continue driving base metals and bulks in the near term with 4Q GDP last week beating expectation, growing 2.9% YoY (consensus: 1.6%), with Morgan Stanley (Morgan Stanley research, 25 January 2023) projecting above-consensus growth of 5.7% in 2023, with greater alignment between economic, regulatory and Covid policies driving growth.

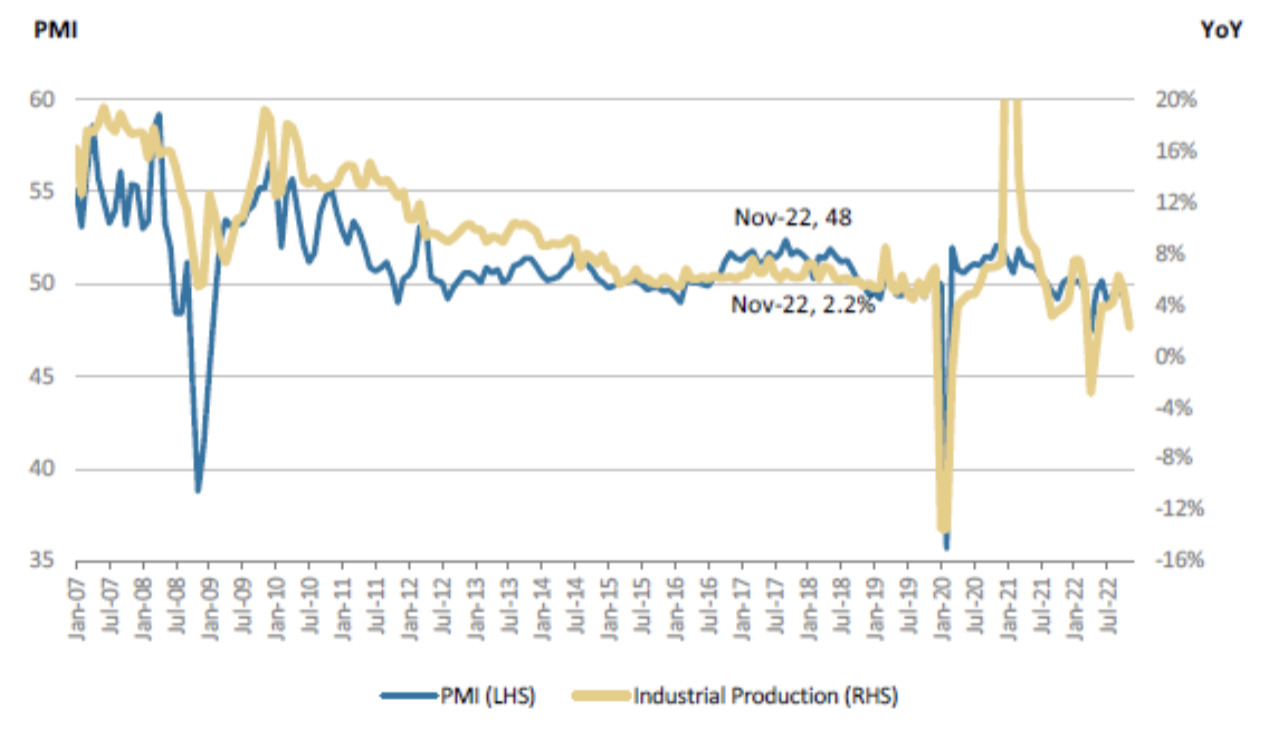

The property market, one of the big Chinese economic drivers, remained subdued however rising 1.3% YoY in Dec (Nov:+2.2%), with PMI at 47.0 (figure 1) (Nov: 48.0) and fixed asset investment (FAI) rising 3.1% YoY in December (November: +0.7%).

With a likely turnaround in the Chinese economy, it is timely to look at base metal inventories which Andy Holme from Reuters highlights are down more than 50% YoY since 2000 with the Shanghai Exchange at its lowest copper inventories since 2007.

Refined imports of copper concentrate are also running at record highs and it appears that China has been buying the dips and stockpiling scrap/concentrates.

Copper featured prominently in last weeks column and given its status as the bell weather for economic health it is worth revisiting some other recent developments which are likely to have medium to long term impacts on copper prices. Commentators like to call copper “Dr Copper” as its reputation as a leading indicator for forward looking economic activity, however “Dr Chaos” is also equally applicable.

To begin with, copper has spent much of the last two years in backwardation however front month premiums are back in contango with long positions now outnumbering short positions by a factor of 1.8x.

The performance of copper since September last year has been strong putting on 25% from US$3.35/lb to recent highs of US$4.20/lb and currently trading around US$4.17 with October 23 delivery remaining in contango at just over US$4.19/lb.

Citibank recently reported that around 7 billion has flowed into the LME/Comex copper this year which goes a long way to explaining the ratio of longs to shorts in the copper market. In physical terms this has translated to net buying of around 750,000 tonnes in the first three weeks of January.

I have talked at length about risks to copper supply in developing / higher risk jurisdictions however it appears the first world is playing catch up with the Biden administration cancelling the licenses of Antofagasta’s Twin Hills underground copper-nickel PGE mine in north-eastern Minnesota due to concerns with water ways.

With over US$500 million invested over 10 years this is a massive blow for the Company that was forecast to produce 5.8 billion lbs of copper, 1.2Blbs of nickel, 1.5Moz of platinum, 4Moz of palladium, 1Moz of gold and 25.2Moz of silver over a 30-year mine life.

Panama also announced recently that it will not allow Canadian miner First Quantum to expand its copper operations while at the same time lobbying for an increase in tax to US$375 million. Apparently the Panamanian government is looking for other potential developers of Cobre Panama raising concerns of a potential nationalisation of the company’s mine.

Micky Fulp (Mercenary Geologist, 28 January 2023) also points out that other base metal projects have also been knocked on the head including Trilogy Metals copper-zinc project in Alaska, a joint venture with S32. Chinese owned Las Bambas located in Peru, which accounts for 2% of world copper supply) is also considering a shutdown as local unrest becomes intolerable.

Fulp also points out that the world is consuming copper at an alarming rate of 20Mt per annum, equivalent to the entire output from the giant Bingham Canyon Mine in Utah since the early 1900’s.

Combined with ongoing political uncertainty in countries such as Indonesia and Chile and underinvestment in copper rich countries such as The Philippines, all bets are off when it comes to forecasting reliable supplies of copper.

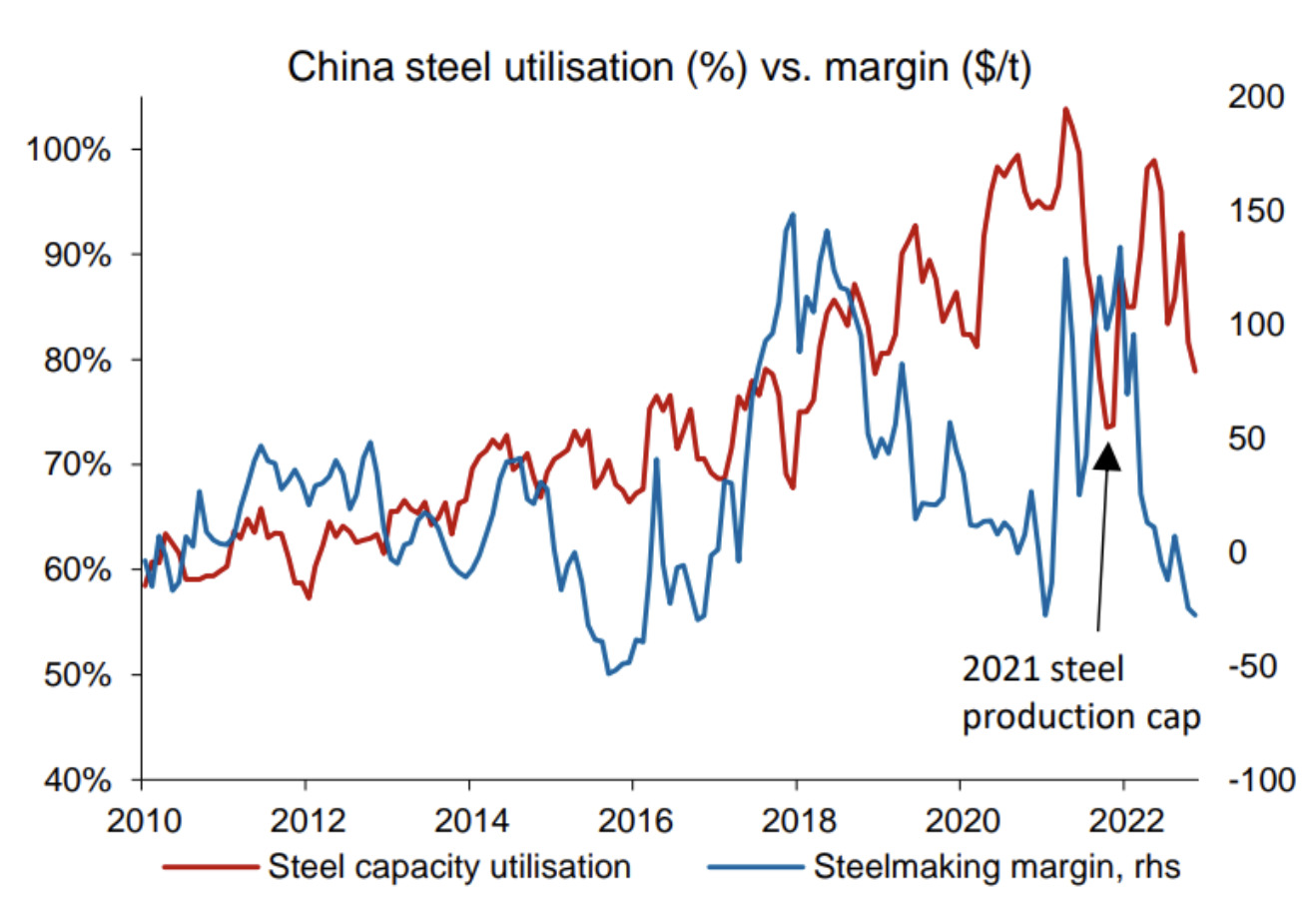

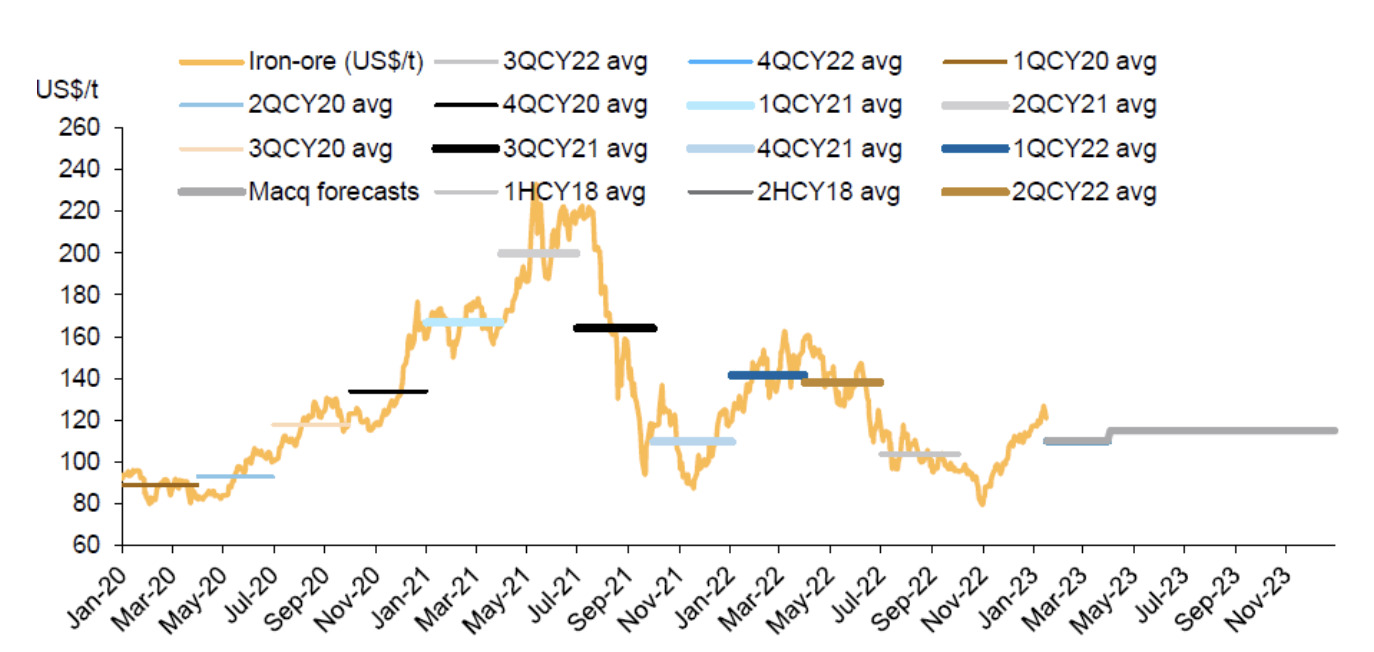

The other bell weather to keep an eye on is of course iron ore. While steel production declined over 2023 (figure 2), benchmark (62% fines) have remained well above US$120/tonne this year (figure 3) and up 50% since November 2022.

Steel exports however are making a comeback up 7% YoY in December with net exports increasing 17% YoY to 4.7mnt.

December saw an 8% MoM decline in iron ore imports to 91Mt. No doubt this was due to weaker demand in line with a 2.4% MoM decline in steel production. At the same time Australia’s iron ore shipments expanded by 8% MoM over the same period. 2022 iron ore imports were down 2% YoY to 1,107Mt.

The newly founded China Mineral Resources Group (CMRG), an organisation that will be responsible for sourcing raw materials for China’s steel mills, aims to obtain more control over iron ore pricing using this centralised purchasing system. In theory the net effect would be to make it more difficult for iron ore miners to have Chinese steel mills bidding up prices.

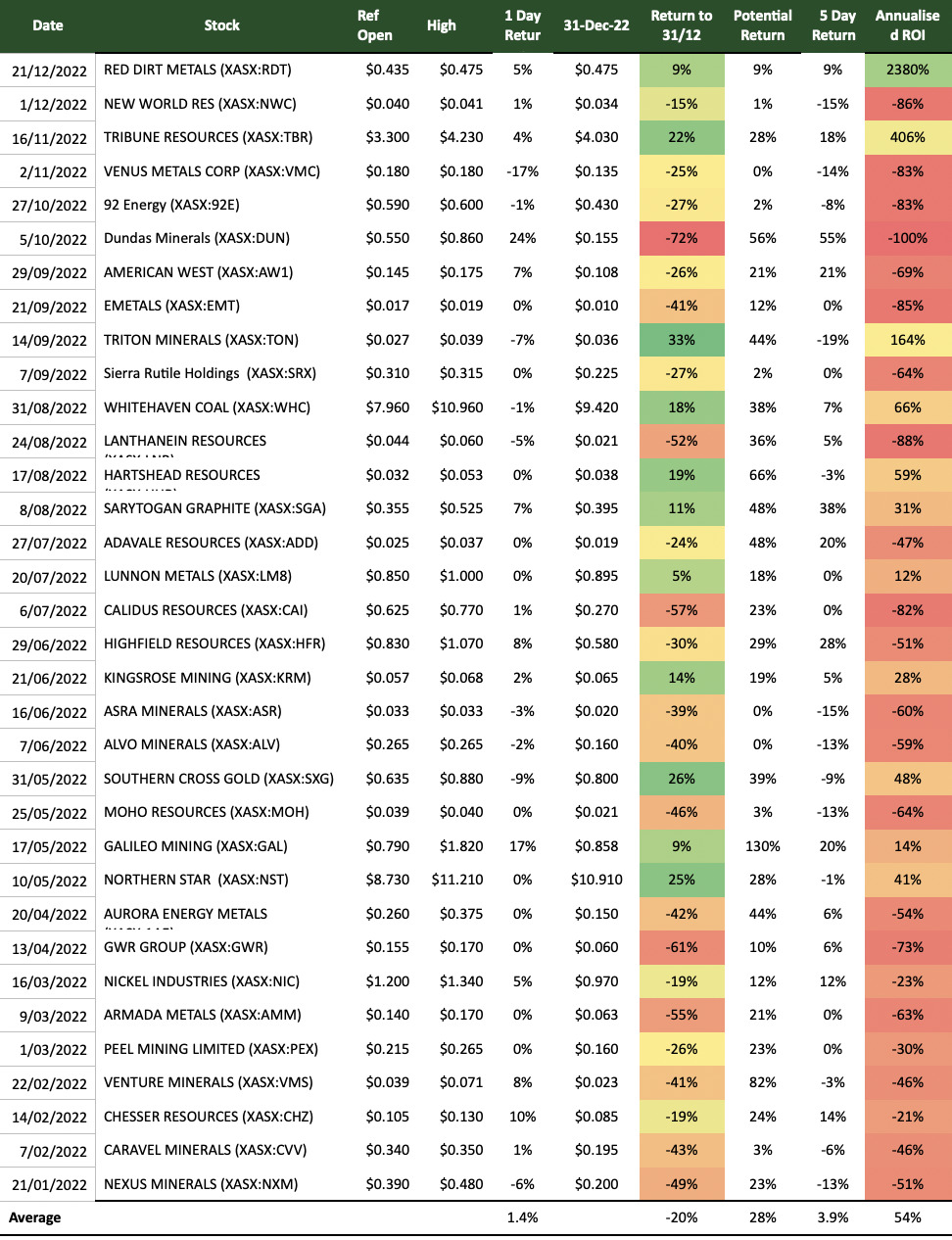

As always a mixed bag, however I should point out before the Stockhead Faithful Police come after me that some of the companies mentioned here were put on the watch list (Dundas Minerals) rather than having a buy or accumulate rating so the returns on an average basis were no doubt dragged down somewhat.

Anyway, that is my story, and I am sticking to it.

Some of the standouts were Northern Star Resources Ltd (ASX: NST) up 25% to 31/12, Tribune Resources Ltd (ASX:TBR) up 22% and Southern Cross Gold Ltd (ASX:SXG) up 26%, all strong conviction buys fortunately.

Sentiment towards junior resources in the second half of last calendar year was soft which dragged down many of the stocks mentioned here. One that was certainly disappointing was Nexus Minerals Ltd (ASX:NXM) off 49% year to date despite a number of successful drill campaigns at Wallbrook which I believe still has potential well above +1Moz, near surface at good grades .

At a market capitalisation of around $70 million, this Company has to be in the slot for one of the better value gold explorers on the ASX.

The wooden spoon goes to Dundas Minerals Ltd (ASX:DUN) who have recently convened a general meeting to change their name to Dunny Minerals Ltd to reflect the underlying quality of their Fraser Range exploration portfolio.

A spectacular miss at its Central Prospect that sent the share price on an impressive run to $1.55/share before retreating down the “S” bend to 17 cents. With executive ski holidays cancelled, the real estate agents number blocked, and the Bentley brochure ending up in the recycling bin it was a humbling experience.

The smartest person in the room turned out to be former Dundas geologist and University colleague Michael Northcott who left the building before the “discovery” and retreated to Byron bay to eat Kale and do yoga.

I will return with more stock recommendations next week as I recover from binging on champagne and skiing at Whistler over the Christmas period. In the interim I hope the stocks highlighted over 2023 continue to fund the decadent lifestyles of the Stockhead Faithful and lead you in to even more wasteful excess.

At RM Corporate Finance, Guy Le Page is involved in a range of corporate initiatives from mergers and acquisitions, initial public offerings to valuations, consulting, and corporate advisory roles.

He was head of research at Morgan Stockbroking Limited (Perth) prior to joining Tolhurst Noall as a Corporate Advisor in July 1998. Prior to entering the stockbroking industry, he spent 10 years as an exploration and mining geologist in Australia, Canada, and the United States. The views, information, or opinions expressed in the interview in this article are solely those of the interviewee and do not represent the views of Stockhead.

Stockhead has not provided, endorsed, or otherwise assumed responsibility for any financial product advice contained in this article.

Mining

News

Mining

Get the latest Stockhead news delivered free to your inbox.