Mining

Monsters of Rock: BHP's $60 billion Anglo American gambit far from a done deal

Mining

Monsters of Rock: MinRes has 'seen the bottom' in lithium prices, Lynas tightens the screws on rare earths supply

Mining

Pic: John W. Banagan/Stone via Getty Images

Mining

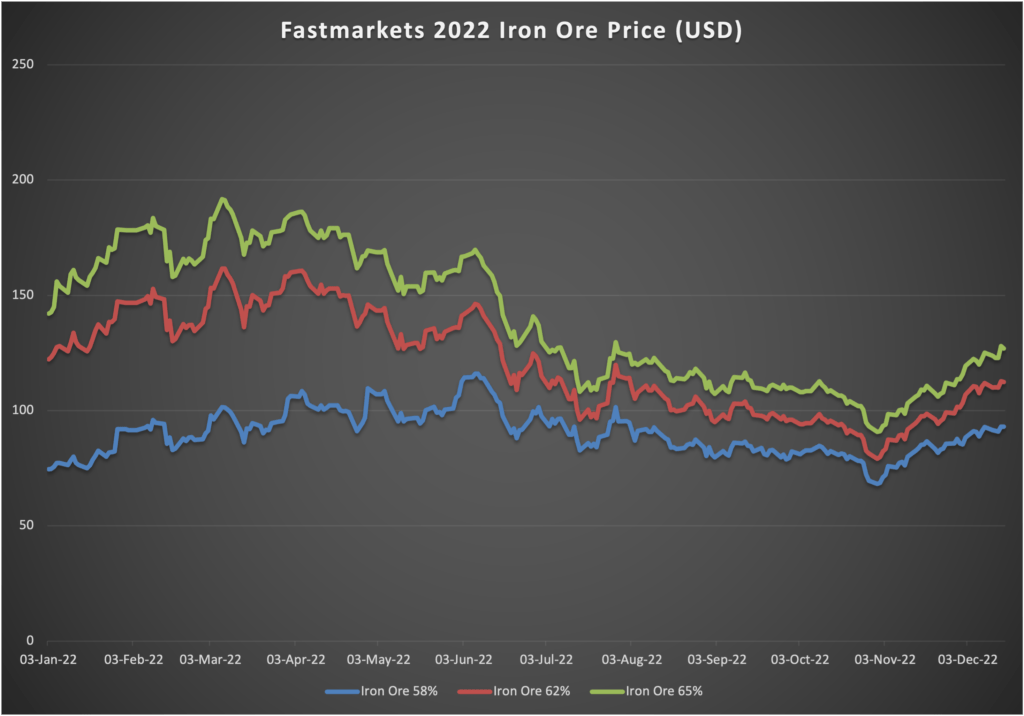

Iron ore has had another topsy turvy year, with its propensity for volatility and seasonality on full show.

The big question coming into 2022 was whether the environmental restrictions which saw steel production in China — home to almost 60% of the world’s output — fall to their lowest levels in five years in the second half of 2021 would continue after the New Year.

Despite China constraining factory activity to provide “blue skies” for the Beijing Winter Olympics and Paralympics, steel production soared in the months that followed and prices rose to over US$160/t in the wake of Russia’s invasion of Ukraine.

Then the lockdowns began, with China’s Covid Zero policy stifling demand for Australia’s top commodity.

Prices halved by the end of October before a late year rally fuelled by China’s sudden paring back of Covid-19 containment strategies sent them back beyond US$110/t, up around 40% in the six weeks from November 1.

Check out this chart for every winding moment of iron ore’s wacky year:

Remember, 2021 was even wilder. Prices peaked at a record of US$237/t, powering incredible profits and dividends for the largest miners on the ASX, before tumbling US$150/t to US$87/t by late November, as China went from its quickest steel production rate ever to its slowest in five laps round the sun.

Given China’s predictable unpredictability, is 2023 going to be a repeat of this unique brand of semi-planned economy chaos?

Fastmarkets Asia Ferrous Editor Paul Lim tells Stockhead the coming year is likely to be a more stable one when it comes to prices.

“In terms of prices, I do not expect the prices to see very large fluctuations, I do not think it will shoot up like how we’ve seen in the past,” he says.

“When prices move in such a big movement especially there is a sense of traders being involved in supporting these prices.

“So that has started to be less common now, especially after China started looking into the iron ore markets.

“Pricewise due to government intervention I also do not expect the prices to move up a lot and we may well see a kind of rangebound or smaller fluctuations in the spot prices in 2023.”

Given the heft of Australia’s producers, iron ore prices have a massive impact on the ASX and its key indices, as well as the broader economy.

Its fortunes are important to every trader, regardless of whether they are an active investor in the space.

A one dollar fluctuation in the price of the bulk is worth 10s of millions of buckaroos to the WA and Commonwealth Governments, while $230 billion capped BHP (ASX:BHP) alone makes up more than a 10th of the ASX 200 since the unification of its British and Australian domiciled entities early in 2022.

To get a gauge on what iron ore prices may do in 2023, there will be a handful of key themes.

“So the main indicators that we are looking for will be clearer after the new year,” Lim said.

“And namely, these indicators are steel demand, iron ore supply and shipments from Australia and Brazil.

“These are the main things that people know, but other things they want to look at is the start of Chinese housing and construction, the money flowing into new investments in construction and real estate.” (NB: Real estate and infrastructure in China each account for 30-40% of steel demand)

“Some other things to look out for would be how the Chinese real estate industry recovers, whether they start generating sufficient cash flow again.

“A very big factor will be the Two Sessions meeting in March and after that we will have a clearer idea of how the fundamentals will be.”

Just as it provided a vail for inflation and cost increases which have proven to be more fundamental than temporary, Covid has been a handy excuse for iron ore producers like BHP, Fortescue and Rio Tinto to explain China’s lacklustre economic performance and weak downstream demand.

That, especially double-digit falls in new property sales amid an industry debt crisis, has seen a massive drop in steel prices and profitability.

At the end of June, as prices really started to feel the gravity of China’s lockdowns, falling from early year highs above US$160/t, steel mills were shedding an average of US$70 on every tonne they produced.

After a brief return into the black the outlook dimmed in October. By the end of that month, with iron ore prices falling to US$79/t (their lowest level since Vale’s Brumandinho dam collapse sparked a temporary supply shortage), more than 80% of the Pilbara’s customers were losing money.

Chinese rebar is under 4000RMB/t (US$570/t) currently. It was trading at 5972RMB/t in May 2021 (iron ore US$237/t) before Evergrande’s near collapse brought debt concerns among China’s property developers to light and Covid Zero came into full focus as Xi Jinping tried to extinguish the Omicron wave.

BHP, FMG (ASX:FMG) and Rio Tinto (ASX:RIO) have all been positive on China, with BHP bullish about the idea a reopening China will provide Aussie miners a strategic advantage and hedge against a slowing global economy.

“We continue to believe that over the next 12 to 18 months, which is what we’ve said previously, China’s going to provide an underpinning of stability for the global economy,” BHP CEO Mike Henry told reporters at the world’s biggest miner’s AGM in Perth in November.

“So where other economies are turning down more strongly, we think demand out of China is going to be a positive.

“Now, as we move into the winter period, depending on what’s happening with COVID, could we see a bit of turn down in steel? Yes, of course.

“But again, the decisions in BHP and the way that we run the company really isn’t informed by what’s happening over the next three months, the next six months.”

With protests forcing Xi’s hand and China opening up, what if China’s strict Covid policy isn’t all to blame and steel demand in the Middle Kingdom is in genuine decline?

That question will be plaguing the minds of investors, politicians and companies whose livelihoods depend on the success of Australia’s largest export.

What if China’s decision to exit Covid Zero, without the heightened vaccine coverage of relatively successful managers of the virus like Australia, ends up causing the same problem the policy was wound back to solve.

The economy, ground to a near halt by lockdowns, could be in an even worse state if virus cases overwhelm Beijing healthcare system.

“One thing to note about the Chinese relaxation of COVID-19 restrictions is I feel personally that the relaxation policies are happening too much, too fast,” Lim said.

“So I feel that unless China has a very good plan in place to really manage COVID-19 outbreaks in in every part of China, then there’s a worry that a very strong resurgence in the COVID numbers and number of deaths in China may cause China to roll back the relaxations and become more strict again.

“Although there is a sense that if you’re infected and then you can recover at home for certain parts of the population, that’s easier said than done if a lot of people start going to hospital and China starts locking down again trying to restrict movements and all that.”

It’s not all tough questions and nervous nailbiting for iron ore believers.

Some analyst expectations are bearish. The Commonwealth Government’s forecasters see iron ore dropping 18% from US$102/t this year to US$85/t in 2023 and a further 14% to US$73/t (US$69/t) in 2024.

Westpac and Commbank adopted similar postures in November after iron ore prices tumbled, only to restore long-running forecasts after that proved to be a blip.

Commbank’s mining guru Vivek Dhar thinks China’s infrastructure support post-Covid will be less generous than 2021’s supercycle fuel and said in December that it was hard to see upside to US$120/t after a 38% bull run from the recent bottom.

“CISA (industry body the China Iron and Steel Association) estimate that the infrastructure construction sector accounted for ~23% of China’s steel demand last year,” he said.

“All in all, China’s steel demand growth will likely be modest in the 0‑2% range. Such a view brings into question the sustainability of the recent rally in iron ore prices.

“While we see upside risks to our iron ore price forecast over the next year (peak of $US100/t by Q3 2023), we think prices above $US120/t are unlikely to be justified by China’s steel demand impulse next year.”

Westpac went from a US$90/t end of 2023 price forecast to US$70/t and back to US$90/t in less than two months. Have some conviction please.

Some investment banks are more bullish. Citi thinks iron ore will hit US$120/t on a three month horizon (US$105/t end 2023) after China’s reopening, with upside of as much as US$150/t if Xi and Li Keqiang go bonkers on the credit easing.

Another factor that could be supportive for iron ore prices is a dearth of new supply hitting the market in the near-term.

Vale gave a leg up to the Australian miners after ditching its plans to hit long term targets of 370Mtpa and 400Mtpa over the space of 12 months. Its 2023 shipments will be unchanged from 2022’s 310-320Mt.

Iron ore prices are typically responsive to Vale’s production output. A massive shortfall after the Brumandinho dam collapse in early 2019 was the initial catalyst for iron ore’s big run during the pandemic.

Australian producers have promised longer term growth plans, with Rio targeting 345-360Mtpa from its Pilbara mines after it develops the long dormant 40Mtpa Rhodes Ridge operation in the late 2020s. It also expects to make a decision next year on participating in the development of the ~100Mtpa Simandou range in Guinea, long delayed due to infrastructure challenges, political instability and endemic corruption.

Meanwhile BHP sees a pathway to 300Mtpa and then 330Mtpa at its ~280Mtpa Pilbara ops, while smaller players MinRes and Gina Rinehart’s Hancock are planning smaller but still multibillion dollar developments to grow their profiles.

But short term those additions will be muted.

Rio, the world’s largest exporter is targeting 320-335Mt, also copy-pasted from this year. Any increases from BHP and FMG, which only expects 1Mt of production this financial year from its new US$3.8b Iron Bridge magnetite mine, will be incremental at best.

And while Chinese steel output is expected to be slightly above 1Bt this year, the second straight annual decline, it remains only the third year after 2020 and 2021 when it has hit that milestone.

Globally, with a number of countries staring down a potential recession, it is a bit worse. Steel output to October sat at 1.552Bt according to the World Steel Association, 3.9% down on 2020.

Another feature of the iron ore market in 2022 was the emergence of the China Mineral Resource Group, a centralised State buyer for China’s largest steel mills put in place ostensibly to put pricing power into the hands of the customer.

China has long complained the concentration of iron ore production among the major producers and “speculation” from traders has resulted in inflated iron ore prices.

The CMRG is expected to make its first purchases on behalf of companies including world’s largest steel maker Baowu as early as next year, and help coordinate Chinese investments in foreign assets like the long-mooted Simandou mine in Guinea (partly owned by Rio Tinto).

At over US$110/t all the major iron ore producers are making big margins, with the most marginal producer of scale, Mineral Resources (ASX:MIN), also back earning decent margins.

Kingsley Jones, CIO and founding partner of Jevons Global, thinks prices will settle in a trading range of between US$80-140/t, but says it is unlikely prices will reach their pandemic boom highs anytime soon.

“The major headwinds on the horizon are protracted slowness in Chinese real-estate. The boom is unwinding, and we are likely headed for a multi-year workout of the previous excesses,” he told Stockhead.

“However, we think construction related to energy and transport projects will continue. Thawing relations between China and Australia offer some promise for renewed trade in bulk commodities.

“The critical minerals sector may be less open to foreign investment due to national security concerns. Looking out over this decade, we think several related factors will play out to drive new business in iron ore.”

Jones thinks the rise of the CMRG will lead to a ‘more subdued pricing cycle’ for iron ore than the volatile market seen in the past couple years.

“Firstly, the formation of China Mineral Resources Group (CMRG), as a central buyer of iron ore for the largest steel mills will likely led to a subdued pricing cycle for blast-furnance feed-stock, which is the dominant Pilbara export,” he said.

“Prices will likely settle into a trading range between lows around US$80 a tonne, where domestic Chinese production is uneconomic, and around US$140 a tonne, where steel mill margins collapse.

“This world is likely good for BHP, since taking out the highs discourages new offshore sources, like Simandou. The cost of rail lines and ports is a major impediment to bringing on new supply.

“Paradoxically, the Chinese move to cap prices will work in favour of those incumbents who have built capacity, high grade reserves and a strong balance sheet.”

Jones also thinks the push to deliver green steel, which requires high grade iron ore for electric arc furnaces in North America, Europe and Asia, will be positive for formerly marginal players with modest reserves who can ship a high grade concentrate.

Jones says Jevons has a buy and hold on BHP, one of four major iron ore stocks it has a long position on.

“We expect iron ore to range trade between lows around $80 USD/tonne and $130 USD/tonne,” he said.

“BHP Group (is) the best placed major into a period of likely Chinese efforts to cap price on blast furnace feed stock.”

Jevons is also long on Mineral Resources, Grange Resources (ASX:GRR) and Rio Tinto.

Jones says MinRes has growth in lithium and stable cash generation in iron ore as long as benchmark prices stay above US$90/t.

It is worth noting MinRes did approve the construction of the 60% owned Onslow iron ore hub due to enter production in December, which at 35Mtpa and costs of around $30/t makes its long term iron ore prospects appear more stable.

He also likes high grade magnetite producers Champion Iron (ASX:CIA) and Grange Resources.

“Buy Champion Iron and Grange Resources GRR.AX for pellet iron ore production but be wary of their link to the non-China steel cycle,” Jones said.

“Europe is likely in recession with the US to follow. It may be shallow, but if steel demand comes off pellet prices will fall.”

With prices on the rise there are a number of iron ore juniors, some of whom had to shut down their small scale, marginal operations in 2021 and 2022 who could be looking at a new pathway to production.

CuFe Limited (ASX:CUF) temporarily halted mining at its JWD deposit near Wiluna in October, but was able to sell shipments and has kept its mine operationally ready after the late year price rise.

Fenix Resources (ASX:FEX) remains profitable for now at its high grade Iron Ridge Mine near Geraldton, consuming its haulage contractor Newhaul to bring down costs.

Chaired by former Resolute Mining (ASX:RSG) CEO John Welborn, Fenix has paid two consecutive fiscal year dividends and pioneered a hedging model to put a safety net under its operations.

Strike Resources (ASX:SRK) and Mark Creasy backed CZR Resources (ASX:CZR) have announced plans to progress approvals to share port space at Ashburton, previously known as a gas export hub.

Strike opened then dialled back activities at the Paulsens East mine in 2022, while CZR, one of the iron ore market’s top performers this year, has been building out its resource base at Robe Mesa, literally over the fence from where Rio is drilling at its Mesa F deposit.

In the high grade portion of the market, Mount Gibson Iron (ASX:MGX) was halted by a plant fire at its Koolan Island mine, but has attracted the attention of investors as it plans to ramp up production of the mine’s high grade 65%+ hematite DSO in the second half of FY23.

At Stockhead, we tell it like it is. While CuFe is a Stockhead advertiser, it did not sponsor this article.

Mining

Mining

Mining

Get the latest Stockhead news delivered free to your inbox.