Up, Up, Down, Down: Which commodities won and lost in July?

Pic: Tetiana Lazunova/iStock via Getty Images

- Thermal coal was the big commodity winner in July and the world is probably screwed, idk

- Industrial metals like nickel, iron ore and copper recovered from a mid-July blip as optimism returned around Chinese metals demand

- Uranium spot price falls but excitement on future demand bubbles in the background

WINNERS

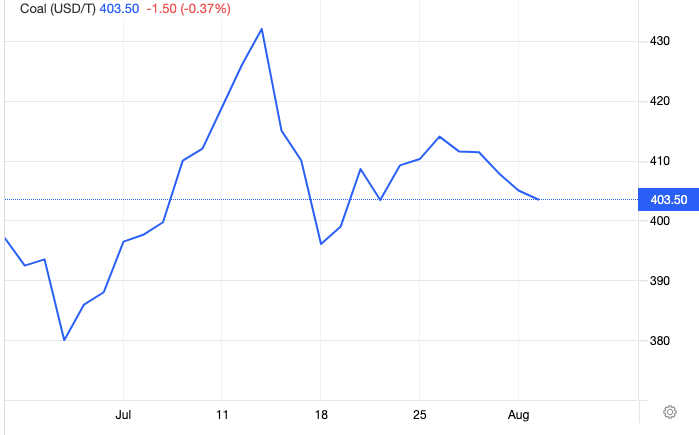

Coal (Newcastle 6000kcal)

Price: US$405.50/t

%: +5.06%

If you want to get a sense of how remarkable thermal coal prices are right now, look no further than Glencore’s latest half year report.

Virtually every inch of its massive rise in profits was down to surging prices for energy, with its Australian and Colombian thermal coal operations and energy trading powering massive lifts in mining and marketing revenues.

How massive?

A stunning 800%+ lift in earnings per share from US0.10c to US0.92c in the first half of 2022, with coal sales the backbone of a jump of 119% in adjusted first half EBITDA to US$18.9b.

Coal earnings rose like a phoenix from the CO2 emitting ashes, climbing from US$912m in the first half of 2021 to – wait for it – US$8.9 billion in the first half of 2022.

Margins in Glencore’s coal operations rose a staggering 760% in the past year to US$160.8b. At spot levels, it will generate US$20b in earnings in 2022 at a margin of US$165/t.

Glencore will pay US$4.5 billion back to shareholders including a US$3 billion share buyback, taking its capital returns for 2022 to around US$8.5b.

With an energy shortage still in train, and a looming ban on Russian coal purchases arriving this month in the EU, it’ likely to continue pulling in the coin.

According to Bloomberg, Glencore has inked an agreement to supply thermal coal to Nippon Steel in Japan until March next year at a crazy US$375/t, an indication customers are expecting high spot prices to continue.

Coking coal for steelmaking has looked a bit different with steelmakers in China and elsewhere tightening the purse strings amid falling margins.

Met coal futures are paying US$208/t, continuing an unusual discount that has seen energy coal prices nearly double those in the premium met coal market.

Coal miners share prices today:

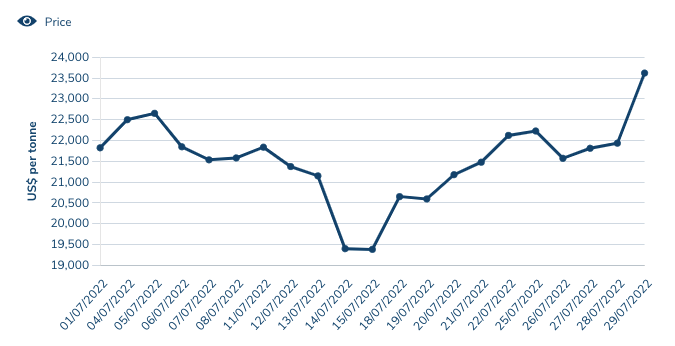

Nickel

Price: US$23,619/t

%: +4.05%

Nickel prices recovered as tight supplies and improved demand in China helped arrest a turn in fortunes that had sent prices down towards the US$20,000/t level.

Current prices are supporting strong margins for producers, and we could need a lot more nickel in the years to come as electric vehicle take-up increases.

The IEA predicts we’ll be after 60 more nickel mines by 2030. Yikes.

BHP (ASX:BHP) Nickel West boss Jessica Farrell says 90% of car sales will be electric by 2040, with demand for nickel to rise three times over the next 30 years.

The largest nickel producer in Australia, Nickel West plans to spend more on exploration this year than any since BHP’s takeover of Western Mining Corporation in 2005.

There could be some challenges for nickel prices in the short term from rising Indonesian supply, however, with Macquarie tipping surpluses of 137,000t and 149,000t over the next two years.

Nickel miners share price today:

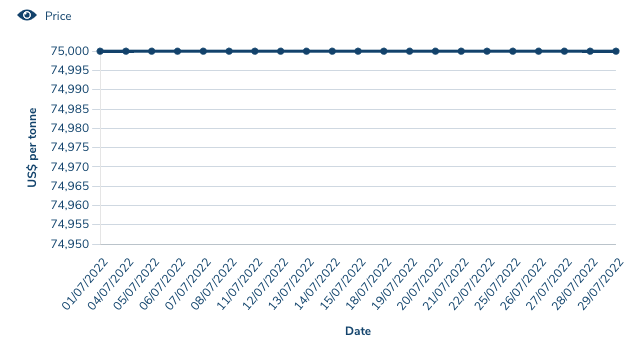

Lithium

Price (Fastmarkets Lithium Carbonate): US$73,000/t

%: 0.00%

There’s no accepted spot market for lithium, something that makes the movement of prices from month to month a tough one to quantify.

Fastmarkets, which provides lithium hydroxide pricing for the LME, reckons spot sales of lithium chemicals remain stable at very high levels, fetching in excess of US$70,000/t.

Spodumene producers are still in a purple patch as well. Pilbara Minerals (ASX:PLS), which has cultivated the start of a spot market with its Battery Materials Exchange, selling its latest cargo at a hefty price of US$7012/t on a 6% SC basis.

According to long-term industry monitor Battery Minerals Intelligence, prices continue to be heady for the electric vehicle commodity.

“Benchmark recorded an offer in South Korea for battery grade hydroxide at $70,000/tonne (CIF Asia), amid reports spot market pricing outside of China has begun to soften, beginning to erode the significant premium that has developed for international transactions compared to the Chinese domestic market,” they said.

“Nonetheless, contacts reported to Benchmark that small spot market volumes of lithium hydroxide in Europe or North America could fetch nearly $10,000/tonne more than an order for lithium carbonate, amid ongoing concerns over availability, with ex-China hydroxide prices still reaching towards $80,000/tonne (FOB North America).”

Lithium stocks prices today:

&nsbp;

LOSERS

Gold

Price: US$1753/oz

%: -3.5%

The recent Diggers and Dealers Mining Forum in Kalgoorlie-Boulder, a town known for its golden past, unsurprisingly brought gold bulls out of the woodwork once again.

None were as plain-speaking as Evolution Mining (ASX:EVN) boss Jake Klein, who boasted prices could rise to within US$2000-3000/oz next year.

“There has been a fear factor over the last six months, nine months,” he said.

“You know, the Fed has come out swinging and talking very strongly about their intent to raise rates until inflation is under control. I just don’t think that’s possible.”

Gold threatened a far larger drop in July, falling at one point beneath its long-held US$1700/oz support before rebounding because the world is kind of scary right now.

China ramping up its passive aggressive (or just aggressive aggressive) military exercises around Taiwan will do it.

Cue a run for bullion, which rose above US$1790/oz before a dampener on Friday as US jobs showed unemployment in the States is sitting at a 50-year low.

Gold miners share prices today:

Iron Ore (62% Fe)

Price: US$114.99/t

%: -3.73%

Iron ore prices have been floppy over the past month, falling under US$100/t for the first time in 2022 in mid-July after a bunch of Chinese property owners walked out on paying their mortgages on unfinished homes.

A bailout brought the market back, flitting between doom and gloom and unbridled positivity through the rest of the month.

The most absorbing story in the iron ore space is of course Simandou, where Rio Tinto (ASX:RIO) secured an infrastructure JV to progress the project with Chinese-backed Winning Consortium and the Guinean Government late last month.

It came after Rio slashed its half year dividend in response to weaker iron ore prices through the first half of the year.

Prices were also briefly stunted after the formation of a centralised iron ore buyer by China, a power play it thinks could give it the capacity to dictate prices with the Aussie majors.

We’re all in wait and see mode on that one.

Iron ore share prices today:

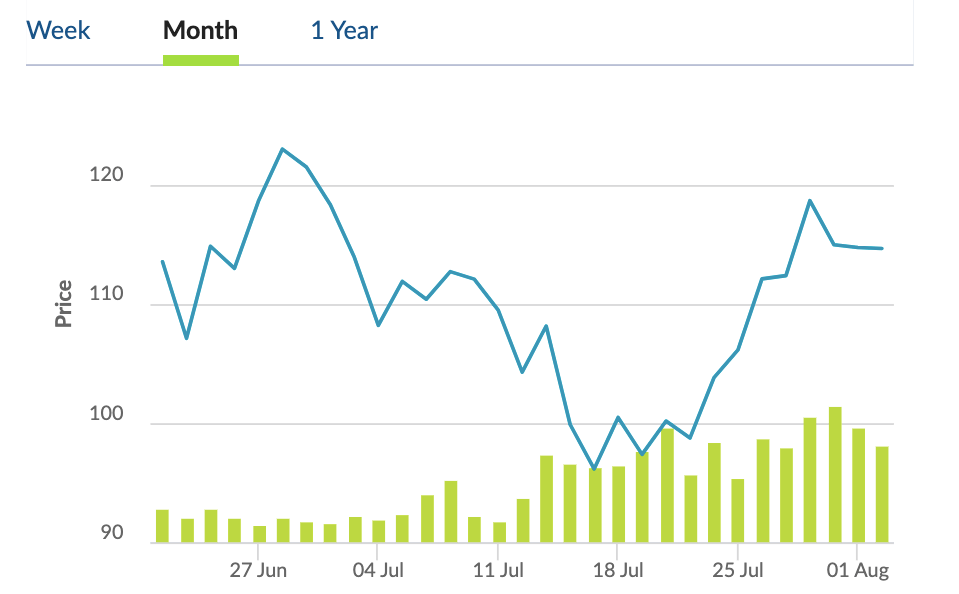

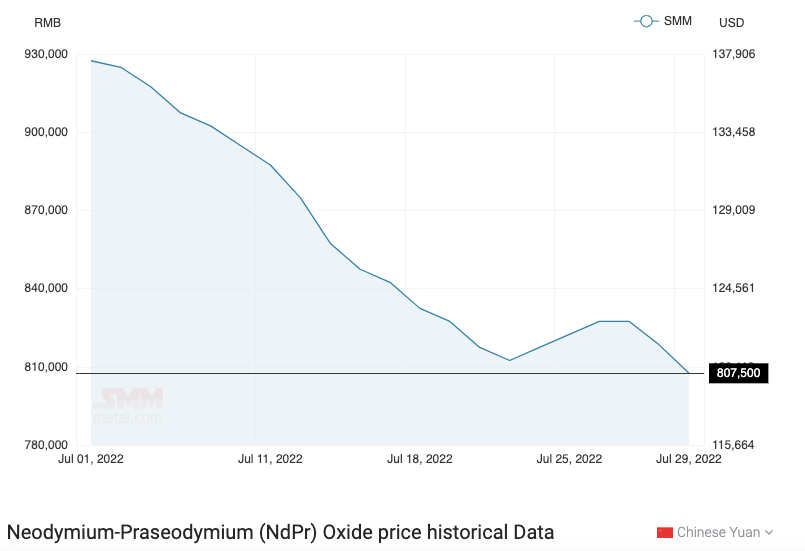

Rare Earths (NdPr Oxide)

Price: US$119.73/kg

%: -13.95%

Rare earths have become vo-la-tile, recording big swings month to month as spot markets in China deal with falling demand amid China’s pandemic response.

A near 14% drop in spot prices for NdPr oxide, a key component of permanent magnets, was the result.

Australia’s top NdPr producer Lynas Rare Earths (ASX:LYC) has a bundle of confidence in the long term outlook though, with its board sanctioning a $500 million expansion of the Mt Weld mine near Laverton to keep pace with demand from electric vehicles and wind turbines, a market which will double by 2030.

Boss Amanda Lacaze said falling short term prices, which remain at levels far higher than a year ago, are not a major concern.

“Every analyst in this sector will tell you that they will end up tearing their hair out if they tried to put together a perfect supply-demand price model,” she said on the sidelines of Diggers and Dealers last week.

“It is a feature of the fact that the market is so skewed towards a single supply source, the price tends to go up and down based upon rumour and what the industry thinks the Chinese Government wants.

“On the other hand, there certainly have been a couple of things, probably the most significant in why the spot price has been changing is because there’s very little product available for the spot market.”

Seasonality is also a factor.

“We see demand being very strong and the other thing is that at this time of the year, and don’t ask me why but there is seasonality in the rare earths market and August and September are generally pretty low and for two weeks around Chinese New Year the price is also pretty low,” Lacaze said.

“My sales team assures me that life should be looking up come October, but we’d never bet on the price. We never bet on the price. And I think that the idea of … people investing based upon today’s price is something I sort of discourage.

“My head of sales Bob, says, if you want to bet on that, go and buy a container of NdPr, put it in your garage because I can guarantee you will find a time when you will be able to sell it and make some money out of it.”

Rare Earths share prices today:

Copper

Price: US$7917.50/t

%: -1.62%

Copper has a bright outlook when it comes to its future as a battery metal, on account of the astonishing gap between forecast demand and emerging supply.

Some estimates say a replica of BHP and Rio Tinto’s giant Escondida mine would be needed each year for 20 years to service demand from a growing green economy.

Clearly that’s challenging. Far from the bullish projections of analysts like Goldman Sachs, however, copper has struggled of late.

True to its label as “Dr Copper” — the thermometer for the world’s economy — a recent slowdown in metals demand amid inflation, interest rate rises and Chinese pandemic lockdowns, have halted its run above US$9000/t in the past couple months.

But after sagging to a 20-month low in mid-July the prognosis is looking a little better amid signs of green shoots in the Chinese economy.

Additionally supply is looking challenged, with the world’s biggest producer Codelco in Chile announcing a 9.3% fall in copper production in the June quarter.

Copper miners share prices today:

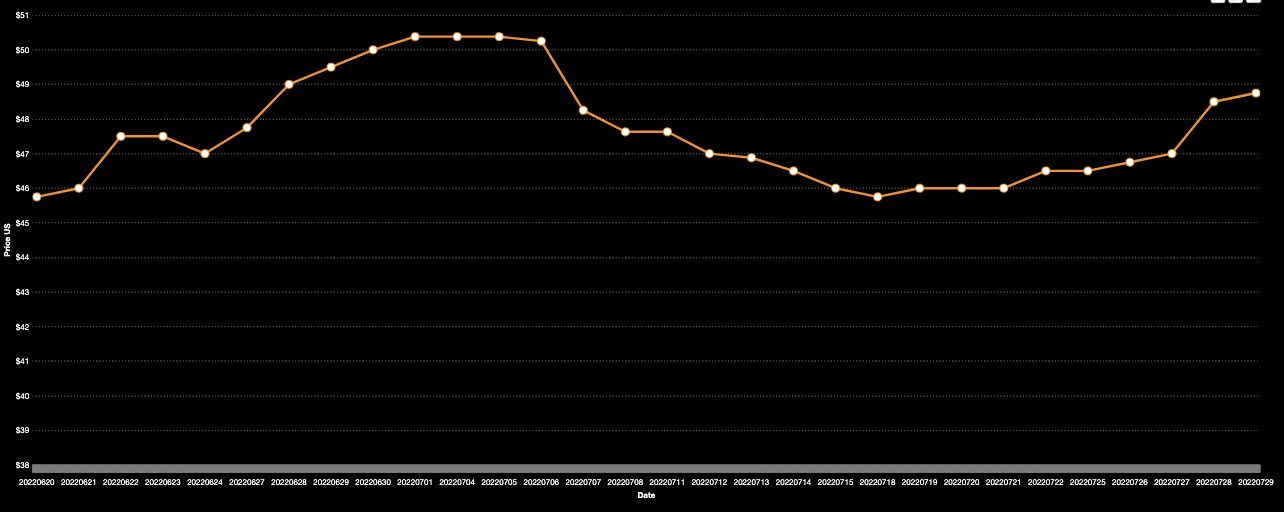

Uranium

Price: US$48.75/lb

%: -2.5%

Uranium prices have failed to breakout this year despite a major run last year powered by Sprott’s launch of its physical uranium buyer.

Utilities that have been able to skimp on prices in recent years have started to turn toward security of supply as product leaves the market.

New producers need to be incentivised to turn on, with some governments returning to the previously unloved nuclear as a weapon (sorry for the pun) in their arsenal to wean off fossil fuel supplies from Russia.

Russia is also a major player in the uranium production and conversion market, with Canadian giant Cameco making a call during the month that higher prices would emerge for Western product as the Russian and non-Russian market bifurcates.

In short, Cameco CEO Tim Gitzel says there’s “no solution without nuclear”.

“Suffice to say we are seeing governments and companies turn to nuclear with an appetite that I’m not sure I have ever seen in my four decades in this business,” he said.

“Therefore, it is easy to conclude that the demand outlook is durable and very bright. But supply is quite a different picture.”

Cameco has already seen utilities shift their procurement strategy for converted nuclear fuel.

“We have temporarily seen their focus shift from securing uranium to the more immediate need in their supply chain for enrichment and conversion services, where Russian capacity plays a much bigger role,” Gitzel said.

“So make no mistake.

“We expect uranium will follow. After all, it is the product to which all services are applied.

“With more than 45 million pounds in new uranium contracts added to our portfolio since the beginning of the year 2022 has already been a contracting success, and we continue to have a significant and growing pipeline of contract discussions underway.”

Over in Oz, Paladin Energy (ASX:PDN) joined Boss Energy (ASX:BOE) in announcing the restart of a shuttered uranium mine, with the Langer Heinrich mine set to reenter the market in 2024.

Uranium share prices today:

Other Metals

Silver

Price: US$20.36/oz

%: +0.54%

Tin

Price: US$25,047/t

%: -5.31%

Zinc

Price: US$3308.50/t

%: +4.8%

Cobalt

Price: $US50,460/t

%: -28.38%

Aluminium

Price: $2488.50/t

%: +1.75%

Lead

Price: $2034.50/t

%: +6.66%

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.