Monsters of Rock: Gold ETFs turn a corner and turnarounds excite ASX punters

Pic: Getty Images

- There are positive and negative signs in the latest gold ETF data

- Aurelia beats guidance in NSW

- Alkane study on Big Boda delivers big returns but at a big capex

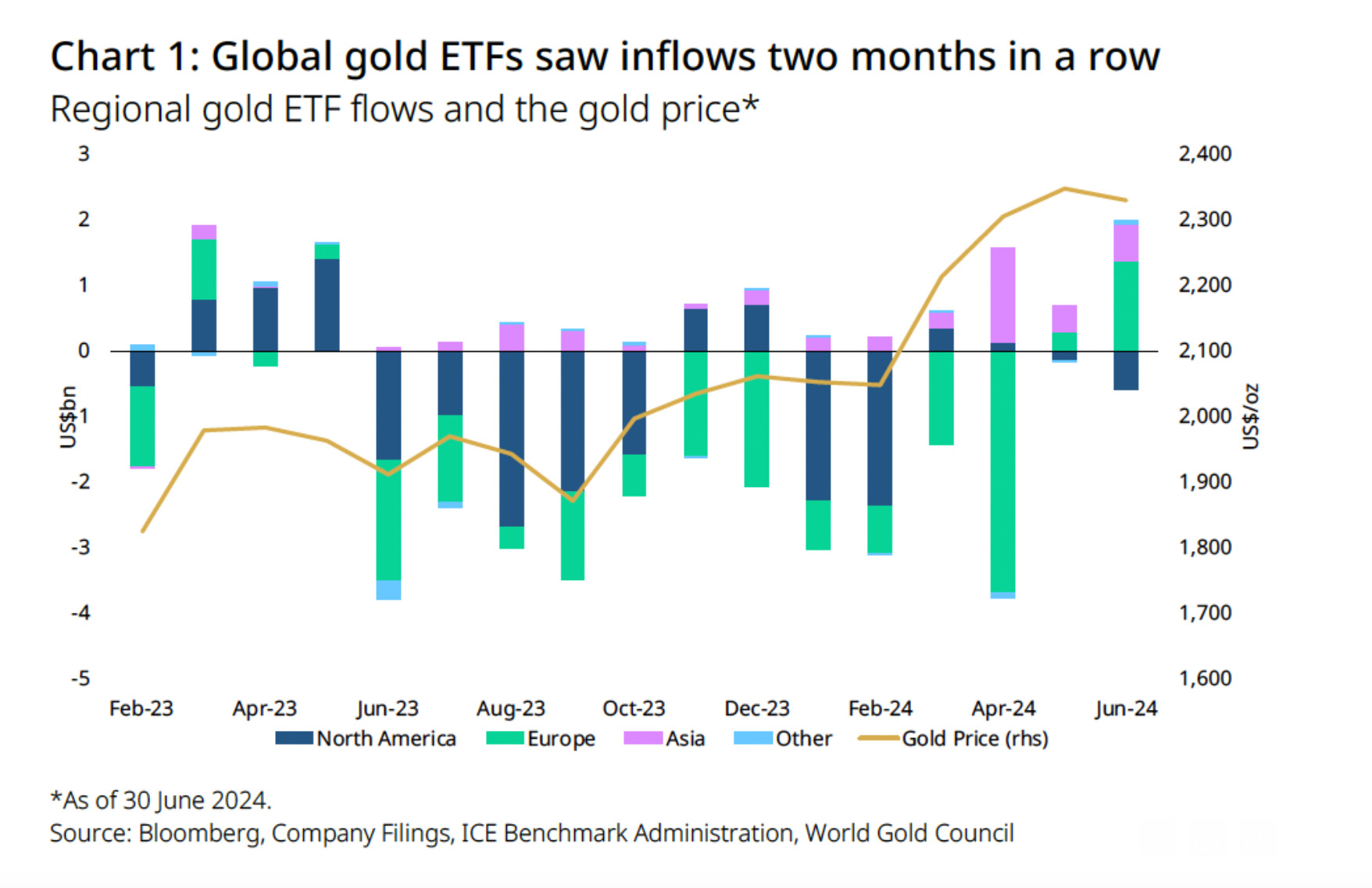

While China’s central bank demand for gold has cooled, recording no increases for a second straight month, one of the few handbrakes on gold prices seems to be lifting, with ETF inflows rising for a second straght month.

The World Gold Council today delivered new stats which showed gold ETFs attracted US$1.4bn in inflows in June, the most since May 2023.

It put a shiny gloss over sad figures which showed H1 gold ETF deposits were the worst first half since 2013, with US$6.7bn in net outflows across the first six months of 2024.

That amounted to 120t of losses from gold ETFs with Asian inflows ameliorating heavy outflows in the US and Europe. Holdings fell 3.9% YTD to 3105t, far short of the record monthly high of 3915t seen in October 2020.

Helped by stronger gold prices, collective holdings are sitting around US$233bn – up 8.8% YTD – but they are still around the lowest levels since 2020. And Asian investors were largely responsible for the good news, with funds in the continent attracting a record US$3bn in the first half.

At the same time, net longs from investors and money managers were up 13% and 36% respectively over the first half, with money manager net longs on gold prices at a more than 50-month month-end high.

Weak ETF performance, tempered by 16 straight months of flows into Asian ETFs, have been viewed as a rare weak spot in gold markets as prices have risen to levels near record highs.

But it has also been mooted as a potential opportunity for bullion, with prices performing strongly in spite of muted ETF demand.

Aurelia up as investors buy turnaround yarn

Aurelia Metals (ASX:AMI) was in a world of hurt a couple years ago when a leaked capital raising forced it to double back on its original funding plans for the Federation copper project.

But it’s up 100% YTD (double for those playing at home), with the 380% stock today announcing it beat production guidance from the Peak and Dargues gold and base metals mines for FY24.

Aurelia churned out 65,300oz of gold at the NSW mines in the 12 months to June 30, above guidance of 60-65,000oz, along with 2200t copper (2000-2300t guidance), 18,700t lead (19,000-22,000t guidance) and 16,800t zinc (16,000-18,000t guidance).

FY24 all in sustaining costs are expected to clock in at the lower end of its guidance of $2000-2150/oz.

Federation was anticipated to hit first stope by the first quarter of FY25, but that could now occur in the December quarter due to a major rainfall event earlier this year. The copper rich Great Cobar development is expected to be approved after.

Once both are in full swing, Aurelia’s revenue is expected to shift from being more than half gold and silver sales to being majority copper-zinc-lead.

Big Bad Boda

While Aurelia was crowing another NSW copper-gold play drew barely a whimper from the market, Alkane Resources (ASX:ALK) unchanged after dropping its Boda-Kaiser scoping study to the ASX this morning.

If it was four years ago the market may have been brimming with enthusiasm. But the heat has come off the porphyry find in the meantime, fading into the background years after the original drill hits sent explorers clamouring to peg ground in the East Lachlan fold belt.

Alkane, which will hold an investor briefing tomorrow, has assessed three scenarios for the 8Moz gold, 1.5Mt copper deposits at the Northen Molong Porphyries.

A 5Mtpa development is unlikely to make the grade at current gold and copper prices, but a larger 20Mtpa scenario has economies of scale that could make it sing or a 10Mtpa development that could be staged or run standalone if gold and copper prices continue to rise.

The largest, 20Mtpa option, would product 35,600t Cu and 159,300oz Au over the first fives years of its 17 year mine life.

Costs are forecast at $630/oz on a gold and copper credit basis, with undiscounted free cash flow of $5.7bn over 17 years.

Albeit, that comes at an average price of $15,000/t Cu and $3500/oz Au, either above or even with current copper and gold prices, which are already near record highs.

Investors tend to get skittish about studies which use costs at or above current price levels, with the mark of a higher tier project its ability to weather down points in the mining cycle.

At $1.8 billion, the capex doesn’t come cheap either. Alkane MD Nic Earner flagged the company could look to bring a strategic partner in on the development, highlighting gold and copper’s ‘strong’ long term market fundamentals.

“There remains significant potential to add both to the overall resource with further exploration, and to the potential project economics with further examination of mining cost and method, particularly large scale underground mining,” Earner said.

“Our focus over the next year at Boda-Kaiser is regional exploration, environmental studies, increasing our understanding of mining options and discussions with potential strategic partners.

“Alkane’s Board would like to thank the team of dedicated employees and consultants involved in the completion of this study.”

Today’s Best Miners

Aurelia Metals (ASX:AMI) (gold/copper) +4.8%

Spartan Resources (ASX:SPR) (gold) +3.7%

Red 5 (ASX:RED) (gold) +2.5%

Perseus Mining (ASX:PRU) (gold) +2.5%

Today’s Worst Miners

Yancoal Australia (ASX:YAL) (coal) -3.9%

Silex Systems (ASX:SLX) (uranium) -3.5%

Alpha HPA (ASX:A4N) (HPA) -3.3%

Champion Iron (ASX:CIA) (iron ore) -3.3%

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.