Guy on Rocks is a Stockhead series looking at the significant happenings of the resources market each week. Former geologist and experienced stockbroker Guy Le Page, director and responsible executive at Perth-based financial services provider RM Corporate Finance, shares his high conviction views on the market and his “hot stocks to watch”.

Market Ructions

Iron ore hit some headwinds and was off 7.5% to US$181.57/tonne (from its record high of US$235.57 in May of this year) in response to Beijing raising export tariffs on some steel materials and removing rebates on cold-rolled products.

China has for some time made it clear it was looking to reduce emissions by cutting steel output as global manufacturing declined.

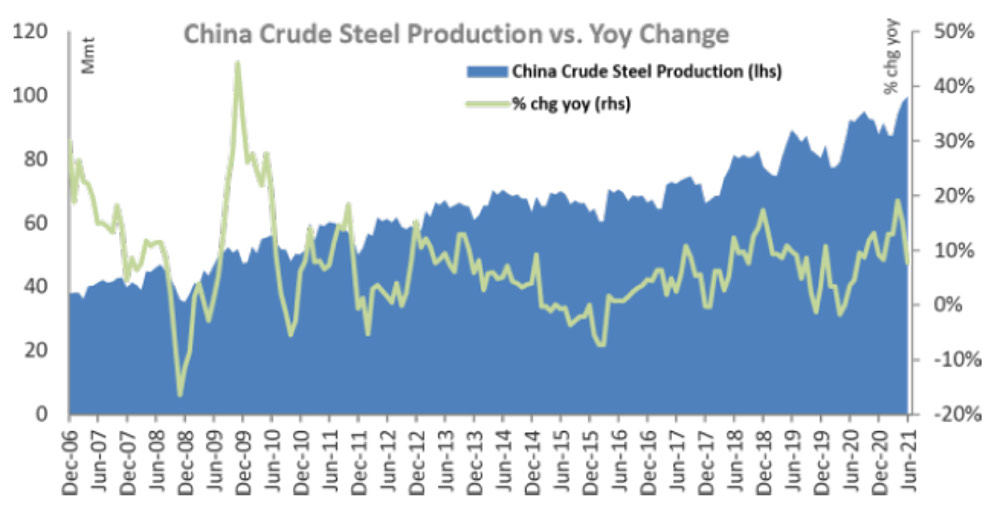

This was in the wake of China’s steel production rising 12 per cent in the year to June 2021 (figure 2).

Shagang Group, the world’s fourth largest steel mill, indicated it would curb production and offshore sales in compliance with government efforts to reduce emissions.

According to CBA, Beijing’s plan to keep China’s crude steel production flat in 2021 implied that output would need to fall 12% year-on-year in 2H 2021.

Figure 1: Iron ore price 1-yr (Source: www.market.businessinsider/commodities/iron-ore-price).Figure 2: Chinese Steel production 2006 to 2021 (Source: Morgan Stanley Research, Metal and Rock, 27 July 2021).

Gold finished up US$12 for the week to close at US$1,814/oz on the back of some poor macro data from the US including unemployment claims 3.7m (higher than expected), lower home sales, higher core inflation, lower GDP growth and a weaker US dollar.

Platinum was off US$14 to US$1,042/ounce while palladium closed at US$2,600/ounce, down US$8 for the week.

The outlook for palladium looks particularly bullish with many analysts considering a move above US$3,200/ounce is likely in the coming months on the back of strong recovery in automotive output and reduced Russian output that could see the global deficit widen to ~275koz in 3Q (vs ~85koz in 2Q).

Copper had a good week closing up 9 cents to US$4.40/pound after the passage of the US infrastructure bill in the Senate and rumours of strikes in Chile.

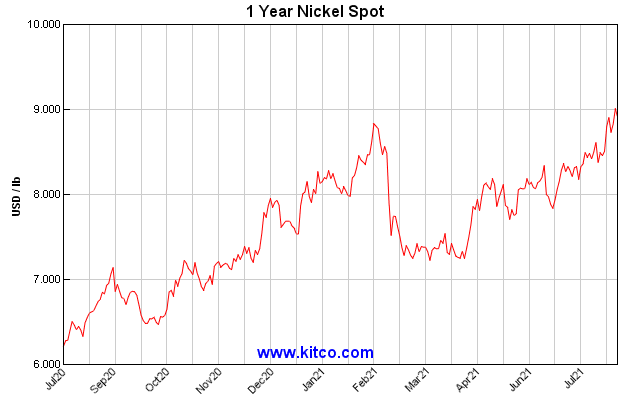

Nickel (figure 3) has remained strong with supply disruptions and a soaring stainless market supporting nickel to fresh highs of $19,300/t last week and is now firmly on track to pass US$20,000/tonne.

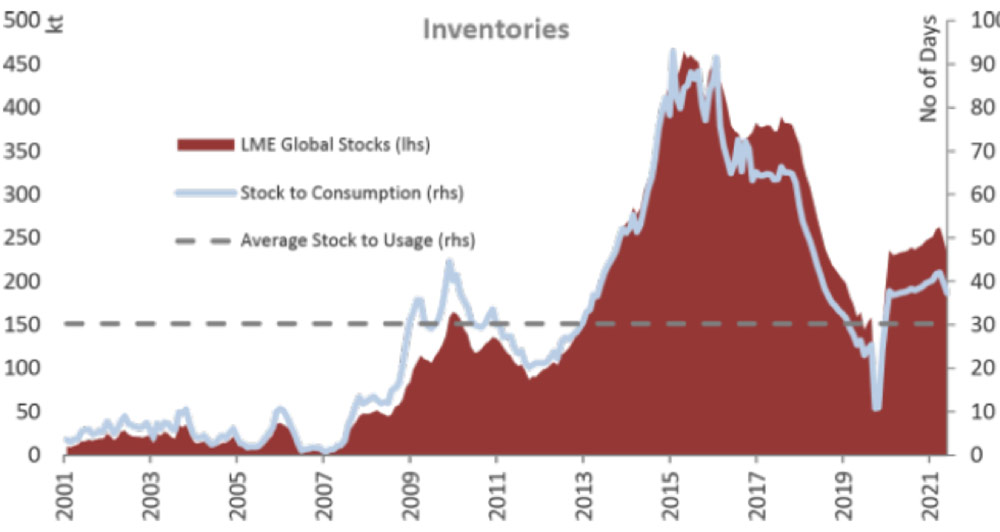

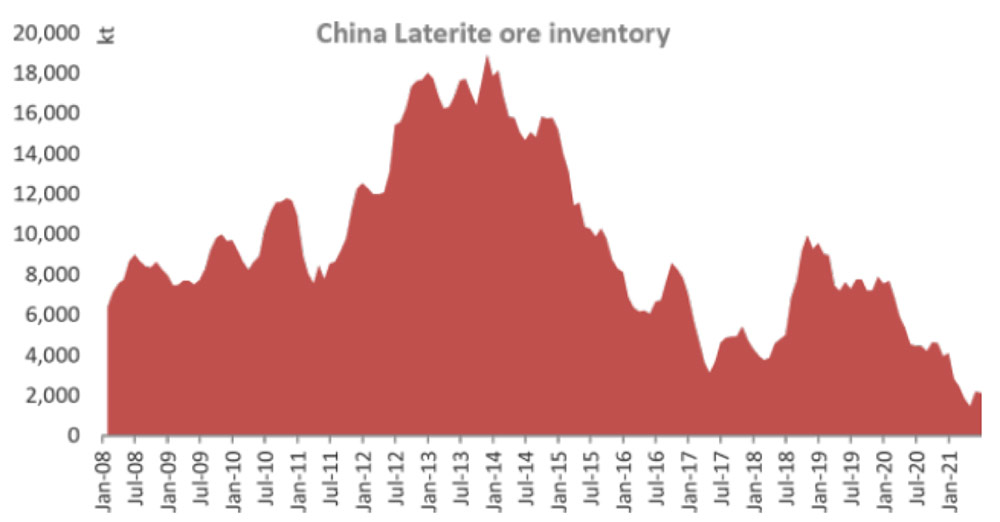

As inventories fall (figure 4, 5) there appears to be support everywhere for a contained rally in nickel with strong demand for stainless from the construction, manufacturing and oil/gas sectors.

Despite chip shortages, EV battery demand remains strong.

While talk of nickel laterite production expansion had suggested an oversupply of nickel, that looks doubtful with a period of market tightness into 2H21 looking more likely.

Add to that supply disruptions at Norilsk (operating at 85% of normal levels) while Vale’s 65ktpa Sudbury mine in Canada has been on strike since early June. Recent protests in New Caledonia have forced the suspension of Glencore’s Koniambo operation while adverse weather is disrupting shipments of ore from the Philippines into China.

Figure 3: LME nickel – 12months (Source: www.kitcometals.com, 27 July 2021).Figure 4: Nickel Inventories 2001 to 2021 (Source: Morgan Stanley Research, Metal and Rock, 27 July 2021).

Figure 5: Chinese nickel laterite inventories 2008 to 2021 (Source: Morgan Stanley Research, Metal and Rock, 27 July 2021).

Company News

You will be pleased to know that I have arrived for the 2021 Digger & Dealers conference here in Kalgoorlie.

A number of the Stockhead faithful had expressed concern that I might be exposed to some barmaids at the Exchange and Palace Hotels wearing what my brother-in-law refers to as “Kalgoorlie formal wear” however I have undertaken to wear dark glasses to shield me from this wicked sight.

I believe a few years ago one of the Big 5 accounting firms (who can’t be named – however you have a one in five chance of guessing) had banned their staff from entering such establishments for fear of breaching their “peace and harmony” rules, otherwise known as an HR policy.

Fortunately, however I believe that a number of them could have ended up at Langtree’s instead, which for those of you who don’t know, provide consulting services to professional men at very reasonable rates.

Support for gold will also be found through monetary policy, excessive quantitative easing, political tensions and the pandemic, according to Goldin.

Alex Passmore presented from Rox Resources Ltd (ASX:RXL) (figure 6) who are about to embark on a feasibility study regarding the development of the Youanmi Gold Project comprising 18Mt @ 2.85g/t gold for 1.66Moz.

Figure 7: IGO 12-month share price chart (Source: CMC Markets, 30 July 2021).

Peter Bradford, the MD of nickel and gold miner IGO Limited (ASX:IGO), (figure 7) also did an excellent presentation with IGO being one of the great success stories of the last 20 years, reporting $392 million in free cash flow with a margin of 65% for the year ending 30 June 2021. Now that is good going.

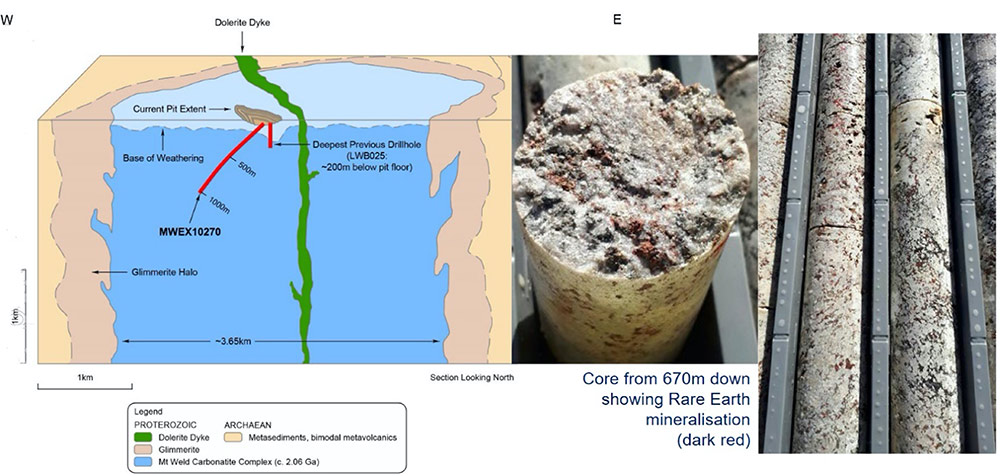

Lynas Rare Earths Ltd (ASX:LYC) (figure 8), another incredible success story now capped at over A$6 billion and the second largest producer of rare earths in the world, gave an overview of the high-grade Weld Range project in addition to their ambitious plans for their Kalgoorlie based rare earths processing facility.

Recent diamond drilling shows the mineralisation at Weld Range extends to around 1km beneath the existing pit (figure 9). So, it looks like they will be around for a while!

Figure 8: LYC 12-month share price chart (Source: CMC Markets, 30 July 2021).Figure 9: Weld Range project showing deep diamond drilling (Source: LYC Presentation, 2 August 2021).Figure 10: VRX 12-month share price chart (Source: CMC Markets, 30 July 2021).

Fresh out of a stellar run atNorthern Star Resources Ltd (ASX:NST), Bill Beament looked more like Steve Jobs (shirt hanging out, preaching to the faithful followers) as he talked about the transformation of Venturex Limited (ASX:VXR) (figure 10), which looks like morphing into a state-of-the art mining contractor while developing their Sulphur Springs project in the Pilbara of WA (JORC Resources of 17.4Mt @ 1.3% Cu, 4.2% Zn and 17g/t Ag).

I am a believer.

The overriding theme of day one of the 2021 Diggers and Dealers presentations was the drive towards the supply of battery metals to satisfy what appears to be an insatiable appetite for EVs and all things electric.

ESG is also a term that is regularly talked about that I believe stands for Energy Sapping Governance which consists of a series of slides showing us all the good things the company is doing for the environment, social and corporate governance.

I’ll be talking more about ESG at the front bar of the Palace with my friends wearing Kalgoorlie formal wear a little later.

However, I did re-examine my own ESG performance (which has been non-existent) and decided to immediately dispatch 12 bottles of rum to our field crew in Greenland. On this basis I believe I have satisfied the “G” in ESG.

Assuming I remember anything that happened this week, I’ll have more to say on Diggers in a week or so. Armed with a fistfull of cash and a box of cigars, what could possibly go wrong…

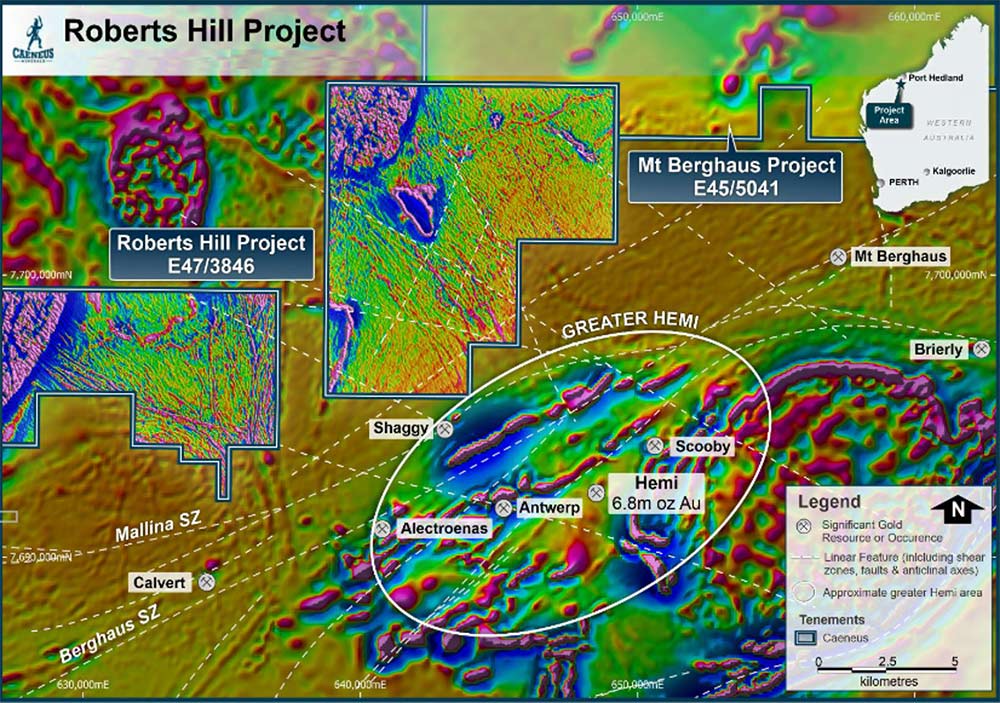

I picked up Caeneus Minerals Ltd (ASX:CAD) (figure 11) earlier last year but thought it was a good opportunity to roll this one out a second time given I had assumed most of you would have forgotten about it.

The company recently completed a $1.7 million placement at $0.007/share to fund a 20,000 aircore program commencing on its 100% owned Roberts Hill project in the Pilbara looking for Hemi (De Grey Mining Ltd, ASX:DEG) style mineralisation (figure 12).

Figure 12: Roberts Hill project in the Pilbara showing geological and geophysical interpretation (Source: CAD ASX Announcement, 27 July 2021).

The company is drilling 150 aircore holes and preliminary reports (ASX Announcement 2 August 2021) indicate that at least three holes have terminated in visible sulphides.

With its proximity to Hemi and highly prospective geology, anything could happen from here!

At RM Corporate Finance, Guy Le Page is involved in a range of corporate initiatives from mergers and acquisitions, initial public offerings to valuations, consulting, and corporate advisory roles.

He was head of research at Morgan Stockbroking Limited (Perth) prior to joining Tolhurst Noall as a Corporate Advisor in July 1998. Prior to entering the stockbroking industry, he spent 10 years as an exploration and mining geologist in Australia, Canada, and the United States.

The views, information, or opinions expressed in the interview in this article are solely those of the interviewee and do not represent the views of Stockhead.

Stockhead has not provided, endorsed, or otherwise assumed responsibility for any financial product advice contained in this article.

Get the latest Stockhead news delivered free to your inbox

For investors, getting access to the right information is critical.

Stockhead’s daily newsletters make things simple: Markets coverage, company profiles and industry insights from Australia’s best business journalists – all collated and delivered straight to your inbox every day.

Markets coverage, company profiles and industry insights from Australia’s best business journalists – all collated and delivered straight to your inbox every day.

It’s free. Unsubscribe anytime.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.

I want the news:

Hear it first

Get the latest Stockhead news delivered free to your inbox.

Thanks! You’re subscribed, Stockhead news is coming your way soon.