Mining

Bulk Buys: It's a 'pivot toward positivity', but will China's Covid shift actually light a fire under iron ore?

Mining

Bulk Buys: Get your umbrellas - price forecasts suggest coal profits could pour for a while yet

Mining

Pic: Supplied

Mining

After four years at the helm of Allegiance Coal, Mark Gray says the US coal miner is on the cusp of making it into the big leagues.

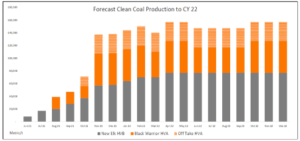

Having restarted the New Elk coal mine in the last week of May, Allegiance (ASX:AHQ) and acquiring the operating Black Warrior mine in July, the company is about to hit the inflection point on a plan that will turn it from a small coal mine developer to a mid-tier with a 2Mtpa plus production profile near term.

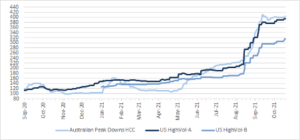

With prices for coking coal on the seaborne market around all-time highs, that means an inflection point for revenue as well.

“Our cash flow this quarter was only $1.7 million, which was really just Black Warrior, a producing asset contributing cash flow we inherited following our acquisition in August, which is nice,” Gray told Stockhead

“But, I can tell you in the fourth quarter that number will be at least 15 times that stepping up again first quarter 22”.

“We are literally that close, our first vessel sails next week with another following a month later. And that start’s our rapid climb up the revenue curve.

Allegiance is working on adding a second production unit at New Elk, where the company is aiming to increase its staffing from around 90 to 130 to ramp up its productivity.

At Black Warrior, Allegiance’s production rate will increase this quarter from 200,000tpa to 600,000tpa.

Drum samples of New Elk coal have been sent to prioritised customers in Japan, Brazil, South Korea, and Europe, with Allegiance’s first shipment to leave ports bound for Asia within days.

“Revenue growth is our aim in December 21 quarter stepping up again in March 22 quarter, and then we’ll focus on driving unit costs down following 6 to 9 months of start-up and ramp-up” Gray said.

“That’s where we’re at, it’s very demanding but it’s very exciting. I wake up in the morning and pinch myself sometimes, I mean it is that close.”

The New Elk acquisition bears similarities to legendary Australian coal tale Stanmore Coal (ASX:SMR), where Nick Jorss paid $1 for the Isaac Plains mine and turned it into a $250 million a year business.

Gray has similarly lofty expectations for Allegiance and New Elk.

New Elk was placed on care and maintenance in late 2012 as coking coal prices nosedived and its previous owners struggled to achieve consistent production and contain operating costs.

Allegiance paid just US$1 in 2020 to acquire the shares in New Elk and undertook via New Elk to repay a C$55 million debt from New Elk’s bankrupt holding company shareholder Cline Mining Corporation through a mix of shares, cash, a reclamation bond and payments out of cash flow.

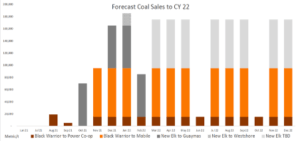

After commencing start-up late May, the first of an initial four 70,000t shipments is due to head for Asia from the Port of Guaymas in north-west Mexico this week.

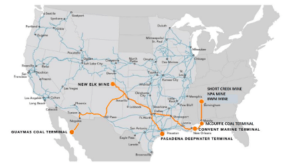

New Elk is strategically located in Colorado, close to North America’s western seaboard.

That gives Allegiance a competitive advantage over other US coal producers, most of whom operate on the east coast.

Allegiance has direct access to the Japanese and Korean steel markets, where prices paid for coking coal are scaling to new highs on the back of supply constraints and soaring steel production post pandemic.

“Our medium to long term target market for New Elk without a doubt is Japan and South Korea,” Gray said.

“Three mills from that region have expressed a keen interest subject to sample tests to buy New Elk coal because we can export it off the US West Coast quite affordably and compete direct into the Asian market, unlike all our US met coal peer who are all on the East Coast.

“We’re sort of in the middle of the US and our rail costs are largely the same whether we go east or west.

“We can get a High Vol coking coal product onto the Pacific market a lot cheaper than our competitors can because the Asian steel mills have to send vessels around the Cape. The shipping differential between the US West Coast and the US East Coast can be anywhere between US$20-30/t or more.”

There have been some teething issues at New Elk, largely around labour and housing in the community around the mine.

At the moment the company boasts a staff of around 90 and is running a single production unit, with plans to boost its team to 130 and add a second production this quarter.

Gray says “monthly clean coal production rates from our #1 unit in the Blue Seam Mine will increase from 25,000t currently to 30-35,000t by the end of the year, that’s our target for a single unit”.

“I want to have New Elk doing 800,000 sold tonnes annualised with two production units by the start of 22. My original target was December 21 quarter but the challenges we’ve been experiencing in sustaining the work force because of the lack of housing has slowed us down” Gray said.

“And so at the moment, we’ll reach 400,000t annualised by the end of this quarter with a single unit”.

“Our second unit is not fully manned yet on a single shift, but we’re working on securing more housing to get new guys settled.”

“My aim is to get two shifts fully crewed by the end of the year, then we’ll be in a position to deliver that 800,000 tonnes annualised next year.”

New Elk is a 750Mt resource with multiple deposits, meaning there are growth options aplenty.

“So my strategy for New Elk, it’s a big deposit of 750 million tonnes across nine coal seams, of which four we’re targeting, it offers wonderful organic growth” Gray said.

“The other five, just the mining conditions are not that flash and the coal quality is not as good.

“Each year I want to develop another mine within the target coal seams. And so the objective next year is to open up what we call the Green Seam by the end of the year, particulalry if I’m able to secure long term supply contracts with Japan and South Korea.

“And then add incrementally another 400t, another 400t. And by the end of 2023 or sometime during 2023 be at a point where we’re doing 2.5 million tonnes annualised.”

Those sorts of numbers would put Allegiance in the same mid-tier category as companies like Stanmore.

But it has more production and development opportunities up its sleeve in the Black Warrior and Short Creek mines.

Another canny acquisition was the producing Black Warrior operations, which was running at the margins as a thermal coal producer.

But in its Blue Creek and Mary Lee coking coal products, Gray sees the opportunity to service a more lucrative and sustainable opporunity in the seaborne met coal market.

The Alabama mine, which was effectively a family business run on just five 10-hour shifts a week, is being ramped up from a run rate of 200,000tpa to 600,000tpa for the Pacific and Atlantic trade routes.

“So Black Warrior, which we acquired at the end of July, beginning of August, was a producing mine,” Gray said.

“It was doing a little less than 20,000 tonnes a month and it was an opportunistic acquisition, because the vendor was 82 years old, he’d operated in mining for 30-35 years, he made fantastic money, but the mine was now at the margin, and it needed capital investment and energy to transform’.

“So I saw the opportunity and we bought it. And we’re going through the process now where we’re transitioning that mine from 200,000 to 600,000 tonnes, annualised simply by spreading the existing work force across a day and night shift five days a week on bigger equipment’ .

“So we’ll get to 50,000t a month by the end of the year for that asset.”

While we are still complete carbonisation tests on that coal, it is already commanding more than US$200/t for a low documentation December shipment.

“So one of the opportunities I saw when this asset was put in front of me is that it was a good quality High Vol coking coal, which the previous owner was selling to Alabama Power as a thermal coal,” Gray said.

“So I’m putting that onto the seaborne market straight away. I’ve got a cargo of that, 80,000 tonnes, not the premium product I want to sell long term, just a mixed bag of coals from the mine, going out in the first week of December.

“I’m not yet in a position to get index pricing without CSR documentation and remembering it’s still untested coal, but I still got a price way over 200 bucks.

“I said to my guys, ‘while we’re transitioning, let’s just get as much coal as we can on a boat, now, and cash in on it at 200 plus bucks a tonne’. And then the next vessel, which I hope to get out either the end of December or early January, we’ll target for our premium product’. So Black Warrior is going to enjoy those prices for sure.”

Allegiance Coal doubled up on its Alabama acquisition spree, buying the Short Creek underground mine in October.

That mine is located in the Black Warrior Basin surrounded by major producers including Peabody, Warrior Met and Javelin Commodities.

A JORC 2012 compliant resource statement is due this month, with a feasibility study to be completed next year.

Short Creek is a mid-vol Blue Creek coal, a brand on the seaborne market highly regarded, and in high demand for which premium prices are paid. Four mines in the vicinity produce this coal and are currently getting more than US$400/t.

“Black Warrior was an opportunistic buy. I wasn’t planning on buying it, it was presented to me by another party while I was working on the Short Creek acquisition,” Gray said. “Black Warrior is going to provide fantastic immediate term value, but the asset I really wanted and will take us to the next level of value, is Short Creek”.

“It’s a World class asset, with a hard coking coal to match the best. It’s got size and scale and offers a long mine-life. It sits perfectly with New Elk. New Elk supplies large volumes at the lower end of the coking coal value curve, while Short Creek provides moderate volumes at the top end of that curve”. That’s the plan I had developed.

The other aspect of the Short Creek and Black Warrior acquisitions that really stands out is Allegiance’s commitment to use equity to fund the transactions and associated development activities.

“People tried to persuade me away from that to avoid dilution, borrow the money. That to me is a death wish, right?” Gray said.

“You look at how many ASX juniors transition from exploration, development to production successfully with debt – not many.

“So our share register has developed enormously, and we’ve got some fantastic institutional shareholders, they’re absolutely committed, they’re patient and they believe in the story.”

One of the questions around Allegiance must be whether it is undervalued.

It has no doubt been a beneficiary of the excitement from investors around rising coal prices.

At 46c yesterday, Allegiance stock is up 21% year to date and almost 65% over the past 12 months. But it has hit a high of 76c earlier in the year.

Analysts at Petra Capital believe the company could be worth 5.7 times more, with a price target of $2.67 a share and a buy recommendation.

Petra’s Colin Mclelland says Allegiance is trading at a multiple of only 1.2x of its projected FY2022 EBITDA.

That leaves plenty of upside.

While Allegiance is unlikely to reap the benefits of full pricing for its coal until April, Mclelland still thinks Allegiance will sell 680,000t over the next six months at a healthy average price of US$178/t.

“While AHQ has increasing theoretical leverage to the spot price from the March Quarter, the reality is sales are likely to occur at a discount to spot until AHQ is accepted as a new supplier. We assume this will occur in the June quarter (likely April onwards),” Mclelland said.

“A shipment of 80kt of coking coal predominantly from the Black Warrior mine, but priced as High Vol B is expected in the December quarter, with pricing details to be announced shortly, although the High Vol B index was circa US$200/t when the sale was agreed.”

Petra estimates Allegiance will be raking in $107.6 million in EBITDA in 2021-22 and $284.5 million in 2022-23, a growth rate of 1089% and 164%, respectively.

“AHQ is working through the process of qualifying its coals, with early sales assisting buyers understand the performance of these coals in the steel making process, as well as undertaking coke oven trials to ensure key quality/performance parameters are known and attached to these coals,” Mclelland said.

“Once this is known, AHQ can ramp up its marketing strategy to ensure it realises optimum prices and is able to consolidate its position in its customers’ coking coal blends.”

This article was developed in collaboration with Allegiance Coal, a Stockhead advertiser at the time of publishing.

This article does not constitute financial product advice. You should consider obtaining independent advice before making any financial decisions.

Mining

Mining

Mining

Get the latest Stockhead news delivered free to your inbox.