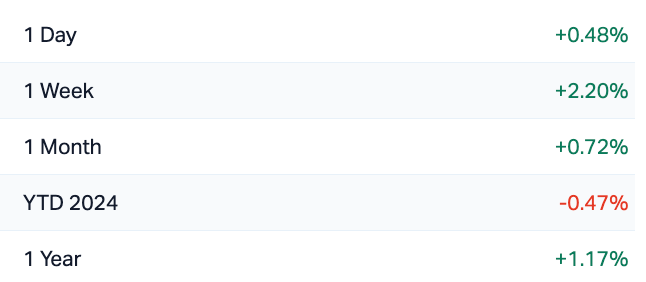

The local benchmark ended the shortened Aussie Day week up circa 2% and TBFH, looks a likely candidate to soon join some of the other global equity markets to clock all-time highs.

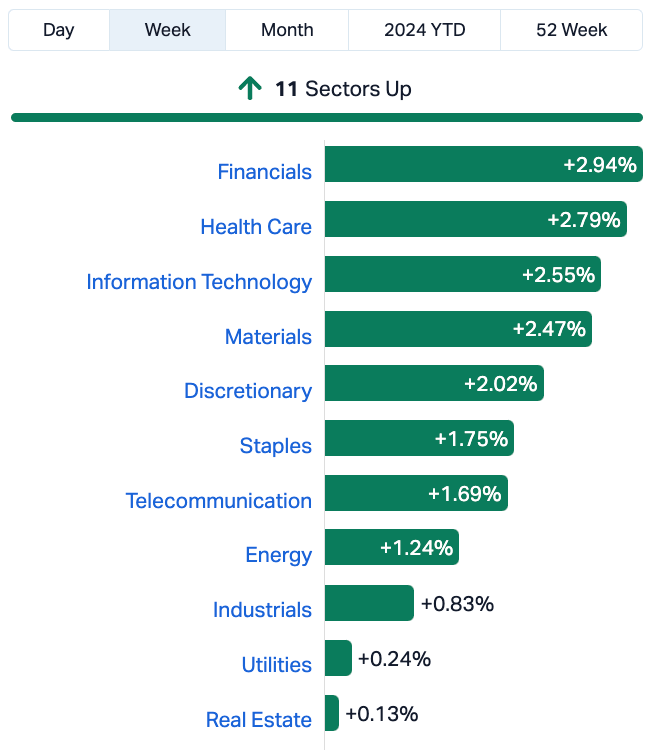

The ASX200’s big name sectors flexed their muscles to provide some welcome positive momentum, with Financials, Energy, Healthcare and Materials at the fore.

The Big Banks had a field week.

The ASX200 (XJO) index

In the US…

Wall Street, meanwhile put six straight positive sessions to the sword on Friday, as discretion proved the better part of valour and a few cash rate cut punters cashed their chips.

Calls to take the points were nigh universal in NY, although not universally appreciated.

Subsequently, there’s a bit more cash looking on from the sidelines to start Monday, but not nearly as much as a betting man would’ve thought. There’s just not enough good bad news (re: US inflation) nor enough bad good news (re: US economy) for US traders to change up their strategies. Growth, strength and the expectation of more. A familiar US outlook.

The majors US indices closed out the week higher – the S&P up 1.05%, the Dow Jones, 0.65%, and the Nasdaq Composite a 0.6% gain.

On the data front last week, America’s much-anticipated December Core PCE fell to 2.9% beating the 3% expected, a near three-year low.

The core US PCE shifted lower too, looking for all money like a disinflation trend.

“Fed rate cuts are coming. The only question is when,” IG Markets analyst Tony Sycamore told Stockhead last week.

Elsewhere, Tesla crashed a little more last week, after the company missed analyst estimates on both revenue and earnings.

The price war with Chinese competitors has taken a heavy toll on Tesla’s margins, and with the stock’s valuation being extremely stretched, the underwhelming results served as a reality check for many investors.

Chinese markets…

Chinese stock markets climbed for a third session post various supportive central government policies to get capital markets back at it.

Announcements finally did the trick in restoring investor confidence. The latest reports suggest Beijing will deploy about 2 trillion yuan to stabilise its markets by purchasing stocks directly. Beyond that, the central bank announced a sharp cut to bank reserves, a move that will inject liquidity into the banking system and hopefully kickstart growth.

Bitcoin…

Bitcoin is trading at circa US$42,100, up 1.3% for the week. Although… maybe let me find a chart to illustrate the roundabout way the cryptocurrency took to arrive there.

Gold…

And after a sluggish few sessions, the price of gold recovered a tad towards the end of the abbreviated Australia Day week.

The XAU/USD spot gold price was trading around US$2,026 – back close again to where it was this time last week, having been down more than a tenner a few days ago.

Around the traps

ResMed (ASX:RMD) +6.36% rallied after reporting better-than-expected 2Q earnings after the close in the US, driven largely by better margins. Upgrades to come on this.

Mineral Resources (ASX:MIN) +7.07% released a 2Q production update which was as much about what they have achieved as it was about alleviating market concerns around their lithium exposure and specifically, the balance sheet. They did well on both fronts.

Domino’s Pizza Enterprises (ASX:DMP) was walloped as they stepped away from prior guidance, the downgrade posted to the ASX at 7.17pm on Friday night – never positive and never a good look.

Fortescue (ASX:FMG) +2.04% maintained FY24 production guidance after shipping near-record levels of iron ore in 1H FY24.

Paladin Energy (ASX:PDN) +0.41% released an update, confirming the restart of operations at the Langer Heinrich uranium operation in Namibia have commenced with first ore being fed to the front end of plant on Jan 20th.

Resources names drove the local markets’ fifth straight session of gains into the Australia Day long weekend, while the local Tech sector is becoming even further estranged from the power players on Wall Street.

The Property stocks fell away following a string of sector downgrades out of Barrenjoey.

That said, all 11 ASX Sectors ended the week higher. Nice.

ASX Sectors Last Week

Via MarketIndex

The Week Ahead

At home, its headline inflation data forecasts are for a significant slowdown in both quarterly and monthly terms. Other releases include December’s retail sales and building permits.

Around the ‘hood, we’re watching Chinese manufacturing PMIs for January – very likely subdued as activity remained subdued despite several stimulus announcements.

In Japan, markets will assess the BoJ’s Summary of Opinions for insights into the central bank’s policy outlook. Other Japanese releases include January’s consumer confidence and December’s industrial production, retail sales, unemployment rate, and housing starts. Elsewhere, Q4 GDP reports are expected from the Philippines, Hong Kong, Taiwan, Saudi Arabia, and Qatar. Additionally, South Korea and Indonesia will update their inflation rates.

US non-farm payrolls on Friday night could see the US make a small shift either way on the date for a first Fed rate cut, which is currently fully priced in for May.

Aside from non-farm payrolls and FOMC meeting, US Q4 earnings season continues this week with reports scheduled from companies including Pfizer, Alphabet, Starbucks, AMD, Microsoft Corp previewed here, Mastercard, Boeing, Qualcomm, Meta, Apple previewed here, Amazon, Exxon Mobil Corp, and Chevron Corp.

The Aussie Economic Calendar

Monday January 29 – Friday February 2

All sources: Trading Economics, IG Markets, S&P Global Market Intelligence, CommSec

MONDAY

Aus Dec retail sales

TUESDAY

Australia NAB Business Confidence (Dec)

WEDNESDAY

Australia CPI (Q4)

THURSDAY

Australia Building Permits (Dec, prelim)

Jan CoreLogic home value index

FRIDAY

Q4 PPI

Australia Home Loans (Dec)

The Everyone Else Economic Calendar

Monday January 29 – Friday February 2

MONDAY

New Zealand Trade (Dec)

Singapore MAS Monetary Policy Statement

TUESDAY

Japan Unemployment Rate (Dec)

France GDP (Q4, prelim)

Spain GDP (Q4, flash)

Italy GDP (Q4, advance)

United Kingdom Mortgage Lending and Approvals (Dec)

Eurozone GDP (Q4, flash)

Eurozone Economic Sentiment (Jan)

Mexico GDP (Q4, prelim)

United States S&P/Case-Shiller Home Prices (Nov)

United States JOLTs Job Opening (Dec)

United States CB Consumer Confidence (Jan)

WEDNESDAY

South Korea Industrial Production (Dec)

Japan BoJ Summary of Opinions (Jan)

China (Mainland) NBS PMI (Jan)

Philippines GDP (Q4)

Japan Consumer Confidence (Jan)

Germany Retail Sales (Dec)

United Kingdom Nationwide House Prices (Jan)

France Inflation (Jan, prelim)

Taiwan GDP (Q4, advance)

Hong Kong SAR GDP (Q4, advance)

Germany Unemployment Rate (Jan)

Germany GDP (Q4, flash)

Germany Inflation (Jan, prelim)

United States ADP Employment Change (Jan)

Canada GDP (Dec, prelim)

United States Fed FOMC Interest Rate Decision

Brazil BCB Interest Rate Decision

THURSDAY

Worldwide Manufacturing PMIs, incl. global PMI* (Jan)

South Korea Trade (Jan)

Indonesia Inflation (Jan)

Eurozone Inflation (Jan, flash)

Eurozone Unemployment Rate (Dec)

Italy Inflation (Jan, prelim)

United Kingdom BoE Interest Rate Decision

United States ISM Manufacturing PMI (Jan)

FRIDAY

South Korea Inflation (Jan)

France Industrial Production (Dec)

United States Non-farm Payrolls, Average Hourly Earnings,

Unemployment Rate (Jan)

United States UoM Sentiment (Jan, final)

United States Factory Orders (Dec)

share

Link copied to clipboard

SUBSCRIBE

Get the latest Stockhead news delivered free to your inbox.

It's free. Unsubscribe whenever you want.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.

Get the latest Stockhead news delivered free to your inbox

For investors, getting access to the right information is critical.

Stockhead’s daily newsletters make things simple: Markets coverage, company profiles and industry insights from Australia’s best business journalists – all collated and delivered straight to your inbox every day.

Markets coverage, company profiles and industry insights from Australia’s best business journalists – all collated and delivered straight to your inbox every day.

It’s free. Unsubscribe anytime.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.

I want the news:

Hear it first

Get the latest Stockhead news delivered free to your inbox.

Thanks! You’re subscribed, Stockhead news is coming your way soon.