Health & Biotech

Healthy balance sheet with no debt, this overlooked ASX health stock has been paying dividends for years

Health & Biotech

Wellnex to get Pain Away for lower upfront cost en route to London Listing

Health & Biotech

Vested Equities believes Wellnex Life is well set up for future growth. Pic Getty Images.

Health & Biotech

Special Report: Vested Equities has initiated coverage on Wellnex Life with an overweight rating and 11.5 cents/share 12-month price target, saying the owner and developer of some of Australia’s leading health brands is well positioned to deliver strong revenue growth.

In its initiation report Vested says the Wellnex Life (ASX:WNX) agreement with world-leading consumer healthcare company Haleon, continued margin expansion resulting from an increase in owned brand sales, and the Pain Away acquisition will drive revenue growth.

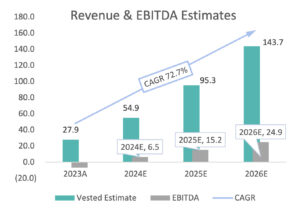

“We anticipate substantial revenue growth from FY23’s $27.9 million to an estimated $143.7 million in FY26E,” Vested says in its report.

“We anticipate FY24 as the year when EBITDA turns positive at $6.5 million, albeit slightly lower than management’s estimates due to our projection of slightly higher integration costs.

Vested says for FY26E, it forecasts a conservative EBITDA margin of 17% because it firstly wants to see how the integration of Pain Away goes and secondly its owned brand revenue contribution.

Source: Vested Equities

Vested says WNX managing director Zack Bozinovski and CEO George Karafotias have

“demonstrated their ability building strategic partnerships with the likes of Haleon and Arrotex, as well as negotiating accretive acquisitions such as Pain Away”.

“This is testament to their remarkable blend of vision, experience, and strategic acumen that makes us unequivocally bullish on their ability to guide the company to new heights,” it says.

Vested says it is further excited to see the appointment of sales manager Nicholas Krogh and marketing manager Dominique Ries.

“The addition reaffirms their confidence in the future growth of the company – and our confidence in management ability to deliver results,” Vested says in its report.

WNX introduced the initial soft gel liquid paracetamol to the Aussie market after significant investment in time and resources, particularly in creating a comprehensive dossier.

Vested says the dossier not only encompasses crucial intellectual property but also necessitates clinical and patient data demonstrating the product’s effectiveness and safety.

Approval of the dossier from the Therapeutic Goods Administration (TGA) is mandatory before any sales, which Vested says provides a high barrier to entry for competitors.

WNX inked a deal in March 2022 to retail its innovative soft gel liquid paracetamol in Australia and New Zealand under the behemoth Haleon brand (formerly GSK Consumer Healthcare).

WNX recently achieved a key milestone by extending its supply agreement with Haleon.

Haleon is a world-leading consumer healthcare company that owns brands including Panadol, Sensodyne, Voltaren, Polident, Centrum, Otrivin and Advil.

Starting FY24, WNX will supply Haleon into the European and Middle East markets with:

WNX earlier this month announced a $13.6m entitlement offer to fund the acquisition of Pain Away, the largest Australian-owned topical pain relief brand and number two provider of topical pain relief products in Australia.

WNX will pay $20.85 million, plus inventory to a targeted value of $1.15 million, for Pain Away, which develops and manufactures pain relief products focused on joint and muscle pain using all natural ingredients.

Pain Away’s current product range consists of 25 individual products across five main categories including creams, sprays, patches, lotions and other (primarily tablets, capsules, and bath salts).

The products are distributed nationally through more than 6,000 pharmacy outlets across Australia, including Chemist Warehouse, Terry White Chemmart, Priceline Pharmacy, Amcal as well as grocery retailers including Woolworths, Coles, and Aldi.

“We believe the Pain Away acquisition will have an immediate impact on the company’s financial position and their bottom line and provide future growth opportunities for the business as a whole,” Vested says in its report.

“We agree with management’s rationale behind the Pain Away acquisition, especially their emphasis on the operational synergies that should be realised immediately after integration.”

WNX is projecting revenue to increase by ~118% compared to FY23 with gross margins expected to rise from just below 25% to just under 30%.

In FY23, WNX entered a partnership with One Life Botanicals, a leading producer of medicinal cannabis.

The collaboration gives WNX access to high-quality locally made medicinal cannabis products for the Special Access Scheme Category B (SAS-B) market, offering competitive pricing.

Acknowledging the unique aspects of this joint venture, Chemist Warehouse also joined forces to introduce a new medicinal cannabis brand.

Vested says WNX appears to be well-positioned to capitalise on the “collaborative endeavours” and the burgeoning SAS-B market, projected to reach ~$600 million in FY24.

“Pain Away is a perfect fit to extend its presence in the medicinal cannabis market and in the future the company will look at bringing to market an over-the-counter S3 medicinal cannabis product,” Vested says.

Vested says its 12-month price target of 11.5 cents/share, which is ~117% increase on its 5.3 cents last close price, is based on a peer-group-based analysis comprising of three custom FactSet Industry indices including:

“For our base multiple, we use an equally weighted metric of the three indices which are applied to both Vested’s forecast and management’s guidance for EBITDA and net Income,” the Vested report says.

“We use equal weights for each estimate then take a time weighted average of 24E & 25E which produces the 12-month price target of 14.5c – that is then adjusted for a 20% liquidity discount resulting in our price target of 11.5c.”

Source: Vested Equities

This article was developed in collaboration with Wellnex Life, a Stockhead advertiser at the time of publishing.

This article does not constitute financial product advice. You should consider obtaining independent advice before making any financial decisions.

Vested has not and will not receive a fee either directly by the company itself or by a third party for the initial coverage report.

Health & Biotech

Health & Biotech

Health & Biotech

Get the latest Stockhead news delivered free to your inbox.