Picture: Getty Images

PETER STRACHAN: Where to find graphite stocks on the ASX? Easy as ABC!

Experts

Picture: Getty Images

Experts

Peter Strachan is a capital markets veteran, resources analyst and lover of the oil and gas game. The brains behind the popular weekly StockAnalysis investment letter, which launched in 2003, Peter has worked in capital markets for over 35 years, and is a qualified metallurgist and geologist.

The Chinese Government’s recent expansion of discretionary licensing controls over graphite exports has sent shivers through the lithium battery (LIB) manufacturing industry outside of China.

China’s new permanent graphite export licensing controls cover exports of both synthetic, as well as natural graphite and its products, including uncoated and coated spherical graphite, as well as expandable graphite.

In reaction to this policy, graphite customers in Europe, North America, and elsewhere in Asia are likely to work towards diversifying their supply chains, effectively instigating an ‘ABC’ policy (Anything But China). Battery makers and other industrial graphite consumers will aim to avoid additional costs, delays and uncertainty surrounding China’s new licensing arrangement, with likely positive flow-on impacts for funding and off-take arrangements for projects located in Australia and Africa.

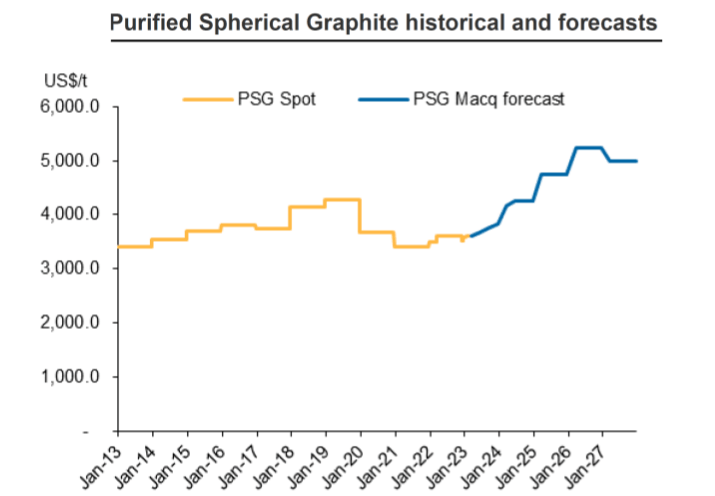

Markets for various graphite qualities are somewhat opaque, often negotiated directly between individual suppliers and users. However, Macquarie Bank forecasts that demand for battery quality graphite will grow at an annual pace of 27%, resulting in a market deficit from 2025. Meanwhile, the price of purified spherical graphite (PSG) FOB China from Benchmark Mineral Intelligence in September 2022 as reported by Fastmarkets, is expected to rise from around US$3,500/t to US$5,000/t by 2030.

Legacy industrial graphite uses require coarse flake graphite for refractory applications, brake linings and lubricants. New energy applications like LIBs require ultra-fine high purity spherical graphite, which is a manufactured product, made from natural graphite.

Environmentally, natural graphite has a lower CO2 footprint than its synthetic alternative and is projected to grow from 40% to 60% of the anode blend over time. Demand from an expanding LIB market is projected to see natural graphite demand increase 650% from 1.1Mt in 2022 to 7.2Mt in 2035.

The recently listed, former uranium focused Kingsland Minerals (ASX:KNG), is a $12 million market cap company with about $4 million in the bank.

The company has recently delivered some eye-wateringly strong graphite intercepts from its Leliyn discovery, located 35km north of the Pine Creek mining centre in the Northern Territory. The company is actively drilling to prove up an initial Resource from an established Exploration Target of 200-250Mt grading 8% to 11% total graphitic carbon (TGC) along 20km of graphitic schist. The target is well supported by intercepts such as 206m grading 10% TGC from surface, including 46m grading 12.2% TGC from 31m and 73m grading 11.2% TGC from 67m.

But wait there’s more! This project is going to be a metallurgist dream.

The graphitic schist also co-hosts significant levels of gallium alongside the graphite, with wide intercepts grading 13-21g/t Ga! Gallium, which currently trades for US$276/kg, finds application in semiconductors, used in all manner of electronic equipment, and its major supplier is, you guessed it, China!

The company is tightly held with its top five shareholders holding about 33% and top 20 controlling 56.6% of the action. Kingsland was floated on its Cleo uranium deposit near Pine Creek, which has an Inferred Resource of 6.8mt containing 2,360 tonnes of U3O8 and has gold and lithium potential on its Pine Creek Orogen province permits.

On the global risk rating, Kingsland will benefit from its location in Australia, even though the NT applies a more stringent royalty regime than other states.

Investors should watch for updated drilling and an initial Resource estimate at the Leliyn graphite project, ahead of the wet season and as the year draws to a close.

Renascor Resources (ASX:RNU) is a $419 million market cap company with a focus on graphite project development at its Siviour project on the mid-east coast of the Eyre Peninsula, where it has established a Resource estimate of 123.6Mt grading 6.9% total graphitic carbon (TGC).

The company is well advanced with mining and processing work following completion of a Definitive Feasibility Study and commencement of battery anode material (BAM) manufacturing studies.

RNU has Mitsubishi Chemical as strategic partner in its development, providing for potential purchase of graphite concentrates, purified spherical graphite and other graphite products from Renascor’s Siviour Graphite and Battery BAM Project in South Australia.

The company should have ongoing news flow on project optimisation and funding arrangements as 2024 progresses.

Lithium Energy (ASX:LEL) is a $68m market cap company that had working capital of ~$8.9 million as of June 30, 2023. LEL holds interests in both lithium and graphite projects in Argentina and Queensland respectively.

LEL’s Burke graphite deposit, located ~150km north of Cloncurry, has an estimated mineral Resource of 9.1Mt grading 14.4% TGC, containing a higher-grade core of 7.1Mt grading an impressive 16.2% TGC. Further south, between Mt Isa and Cloncurry, the outcropping Corella graphite deposit has an estimated Resource of 13.5Mt grading 9.5% TGC.

LEL has completed metallurgical test work, confirming recoveries of over 85% into a concentrate grading over 96% TGC. Pre-feasibility work is now leading to completion of test work designed to produce Battery Anode precursor material, purified spherical graphite, with results expected in the March quarter of 2024.

LEL’s Solaroz Li brine project on the Olaroz Salar is estimated to contain a Resource of 3.3Mt of lithium carbonate equivalent (LCE). The company shares its position on the Salar with Allkem (ASX:AKE) and Toronto listed Lithium Americas. LEL is testing direct extraction metallurgical pathways as an alternative to solar concentration.

Itech Minerals (ASX:ITM) is a $17 million market cap exploration company that had just over $5 million in the bank as of September 30, ‘23. The company’s three graphite projects are in the well-known northern Eyre Peninsula graphite mineral province. Active drilling this year at its Lacroma graphite project has intercepted stacked lenses of graphitic shale over widths of 15-90m grading 6% to 8% TGC with higher grade inclusions of up to 12% TGC at depths from surface to around 152m down hole. The company estimates that the mineralisation has a true thickness of approximately 60m grading 6-7% TGC, containing a ~25m higher grade core grading 8-9% TGC.

At its Sugarloaf graphite project, an Exploration Target of 158-264Mt grading 7-12% TGC has been estimated along a graphite host rock strike of 4.3km. Recent drill results of 28m grading 15% TGC from 75m and 18m at 11.2% TGC from 114m within one hole supports its target.

At its adjacent Caralue Bluff clay hosted rare earth element (REE) prospect, ITM has established an Exploration Target of 110 to 220Mt grading 635-832ppm total rare earth oxides (TREO) plus 19-22% Al2O3. Metallurgical test work has established that 74.5% of the REEs and greater than 75% of the magnet REEs (Nd/Pr) can be concentrated in a fine (<20 micron) fraction, which accounts for 51% of sample mineralisation, leading to potential for a much-reduced operating cost of extraction.

Investors should be watching for ongoing assay results at both ITM’s graphite projects, leading to initial Resource estimates as well as ongoing metallurgical work to optimise a low-cost recovery process from its low grade, REE mineralisation.

Get the latest Stockhead news delivered free to your inbox.