News

Market Highlights: Google, Microsoft boost Wall Street post-hours; and what's the risk for gold from here?

Mining

The world is going nuclear and ASX juniors are exploding on to Canada's Athabasca Basin uranium scene

News

Which three ASX-listed small caps are flying well below where they should be, according to Collins Street's Michael Goldberg? Pic via Getty Images.

Experts

MoneyTalks is Stockhead’s regular recap of the ASX stocks, sectors and trends that fund managers and analysts are looking at right now.

Today we hear from Michael Goldberg, executive director of Melbourne-based Collins St Asset Management.

“100% uplift, maybe more,” is undoubtedly music to the ears of just about any small-cap investment enthusiast.

It’s also the medium to long term share price potential that Michael Goldberg and the team at Collins Street Asset Management believe that they’re seeing in a selection of unloved and misunderstood, yet profitable and well managed small to mid cap industrial stocks.

“This is serious money for the contrarian, deep value investor that can be patient and look through short term volatility,” Goldberg says, adding that in order for these to make sense, you’re going to need some background.

“Markets are often emotional, frequently irrational and always trying to predict things,” Goldberg says, “and for some time now, markets appear to have been predicting a weakening economic environment.”

The consequences of this predication are twofold, Goldberg reckons.

“Firstly, there has been a clear and significant shift of capital away from smaller companies and into the largest listed companies.

“It appears to us that investors concerned by rising interest rates, global unrest and local economic uncertainty are fleeing what they perceive to be higher risk smaller businesses and investing in Australia’s larger companies (even at inflated multiples).

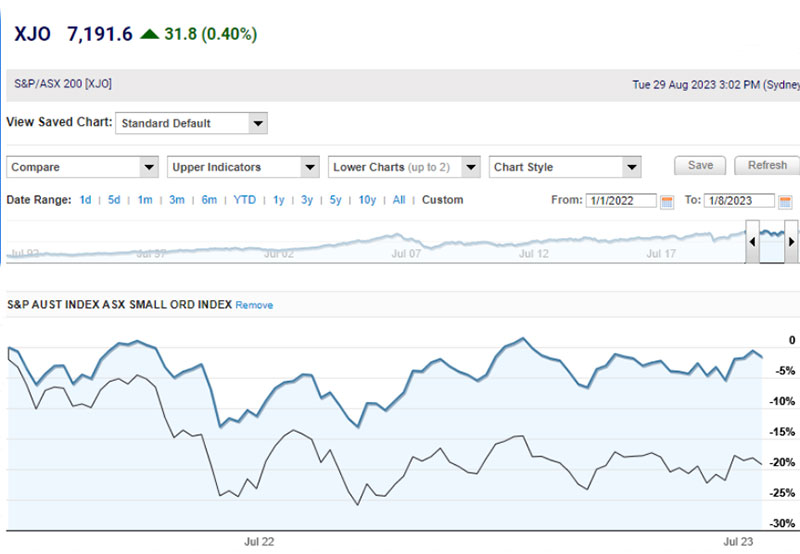

“This is illustrated by the significant divergence between the performance of the ASX200 vs the S&P smalls index – the jaws between the two is astounding and at nearly their widest point since mid 2021 as can be seen from the chart below.”

“Second, based on forward looking concerns for the local economy, investors are unprepared to believe forecast earnings (especially outside the ASX200), creating a situation where companies earnings are being downgraded by investors, while at the same time, investors are prepared to pay lower multiples for those companies’ earnings than they were in the past,” Goldberg says.

So if we accept these two points as true, how should the portfolio be positioned?

“Given the demands of reporting season I haven’t had the opportunity to polish my crystal ball all that often, so my perception of the future might be foggy,” Goldberg says.

“However, regardless of how circumstances unfold, I’d much rather own good quality companies trading at single digit P/E multiples with substantial ‘margin of error’ built into the purchase price than take the risk of paying up for perceived safety in the larger ‘expensive defensive’ type names, particularly if a deep recession does start to bite.

“On the flip side, if we manage to avoid a recession, or the recession is shallow and short, I think there are a lot of smaller companies that will have a lot of (share price) catching up to do as multiples re-rate back to their historical averages and more liquidity comes back into the sector.”

“A solid business trading on painfully small multiples with good growth prospects and an ability to quickly pass on inflation pressure (less than $10 average basket size). The business has spent the last couple of years shrinking their footprint, focusing on the quality of their franchisees rather than simply growing their business without concern for the wellbeing of the network.

“Growth has begun to resurface, clever initiatives (like virtual restaurants) have added significant upside value to our mind, and expression of interest from new franchisees suggest that the outlook for RFG is strong.”

“This company has certainly, experienced some challenges over the last couple of years, but seem to be now getting their house in order. Having reported just this past week, the company has outlined how they expect to return to (cash flow) profitability and are trading at a significant discount to the value of their assets (NTA).

“Currently trading at just 11c, the company confirmed a NTA of 25c per share. We tend to think that the number undersells the value of its equipment given what we’ve seen in the industry of late.

“In an inflationary environment, owning hard (in demand) assets is a good place to be.”

“MMA Offshore has historically provided shipping services to the offshore oil and gas sector. The sector has been unloved for some time now (the last peak was 2013), with a significant and chronic underinvestment in the space for a decade.

“Yet despite how investors might feel about traditional energy, it is a necessary part of global growth for the foreseeable future.

“Due to the underinvestment in the sector (and corresponding growing demand), companies like MMA have seen a significant increase in demand for their ships. Whereas just a couple of years ago utilisation on a fleet like MMA’s would have been under 60%, the industry is currently running at over 90%. This has meant that MMA has been able to lease out their equipment more regularly, and also demand higher prices for that equipment.

“Historically companies like MMA have traded at as low as 30% of NTA during the worst of the industry cycle – at those prices, investors are simply considering what they might be able to achieve if the company was wound up. Yet, when markets return to boom times, it’s been quite usual for these sorts of businesses to trade at over 2x NTA (at that point investors are concerned with a multiple of earnings).

“Boom times and higher prices have, in the past, brought more competition (which ultimately aids in lowering prices), however we have not begun to see that happen. Indeed, given the current global cultural climate, it would be quite difficult for a new player to enter the energy space and raise (or borrow) the capital to do so.

“MMA is currently trading at a little over 1x NTA, but we like the sectoral exposure, and believe that difficult times are likely to refocus consumers on what are the cheapest sources of energy.

“Additionally, the prospects for offshore wind farms have been significantly touted by industry. MMA would be expected to play a significant part in that growth. Already almost 25% of revenues are driven by renewables, and given the growth trajectory of the space, we’d expect those revenues to grow significantly over the next few years.”

The views, information, or opinions expressed in the interviews in this article are solely those of the interviewees and do not represent the views of Stockhead. Stockhead does not provide, endorse or otherwise assume responsibility for any financial product advice contained in this article.

News

Mining

News

Get the latest Stockhead news delivered free to your inbox.