Who Made the Gains? These ASX explorers made investors rich in 2023

Jamie Gold of California reacts as he wins the World Series of Poker no-limit Texas Hold 'em main event at the Rio Hotel & Casino August 11, 2006 in Las Vegas, Nevada. Gold outlasted more than 8,700 other poker players to win the top prize of USD 12 million. (Photo by Ethan Miller/Getty Images)

- The sub $500m capped battlers who made investors rich in 2023 include RDN, CXU, VMM, BEZ and TG6

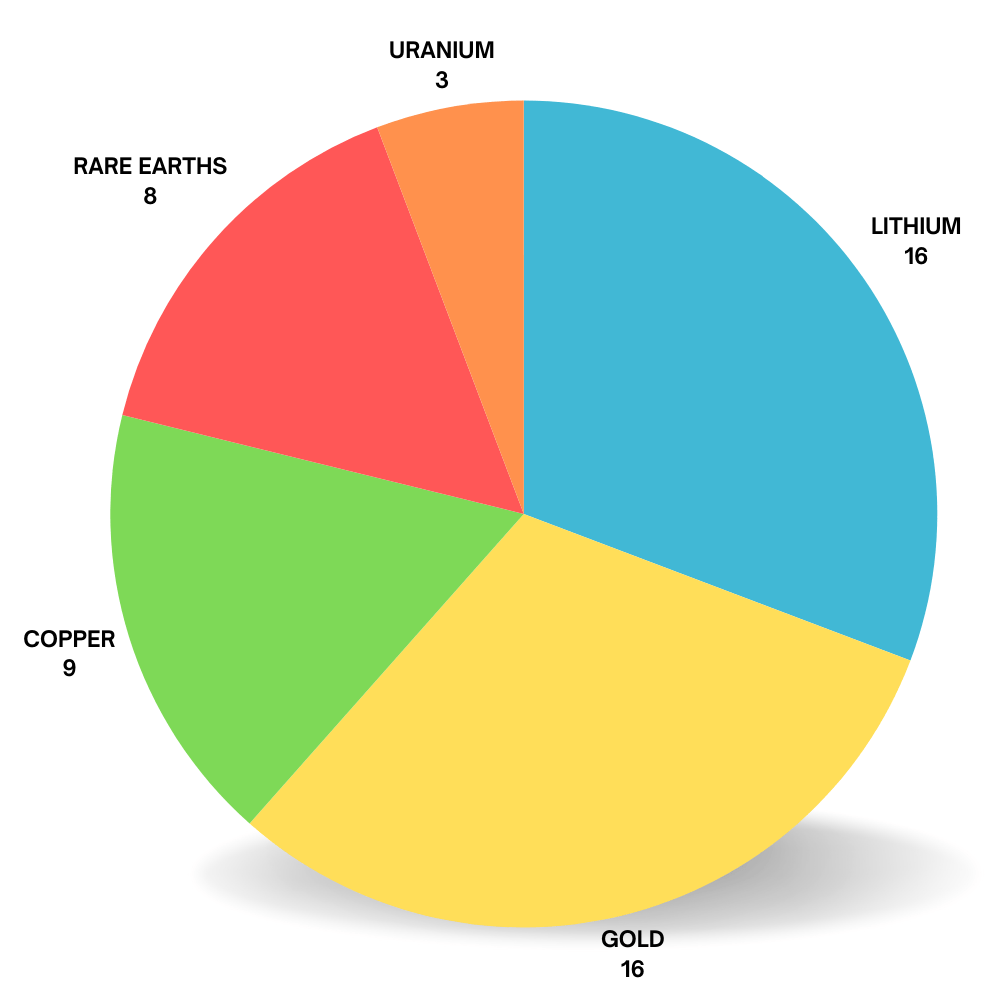

- Despite weak pricing, lithium and rare earths were favoured commodities

- Uranium the best performing commodity in 2023, but only 3 yellowcake stocks in the top 50

This instalment of Gains is a celebration of the best stories of 2023, a year in which the froth was knocked off the markets and dusters, moose pasture, capex blowouts, missed guidance and high-cost projects were punished mercilessly.

With no margin given for blunders and missteps, the truly high-quality stories stood tall.

Much has been said about Wildcat (ASX:WC8) gaining 2775% in a year where lithium plunged ~80%, WA1 Resources (ASX:WA1) making this list 2 years in a row, and the Lazarus-like rise of gold stocks Spartan Resources (ASX:SPR), Ora Banda (ASX:OBM), and Resolute Mining (ASX:RSG).

So, we won’t repeat ourselves. You can read more about the new Monsters of the ASX here.

Instead, we’ll focus on the rest; the sub $500m capped battlers who made investors rich in 2023.

TOP 5 FAVOURITE COMMODITIES FOR 2023

Lithium, rare earths, and the rest of the future facing metals cohort were mostly pummelled, but you wouldn’t know it looking at this group of stocks.

Copper, a favourite to boom during the year, trod water. Gold did well, and stocks responded.

But uranium was the biggest gainer by a huge margin, and yet only 3 yellowcake stocks sit in our top 50.

TOP 50 SMALL CAP EXPLORERS & MINERS FOR 2023

Scroll or swipe to reveal table. Click headings to sort.

| CODE | COMPANY | 2023 RETURN | PRICE | MARKET CAP | COMMODITY |

|---|---|---|---|---|---|

| WC8 | Wildcat Resources | 2775% | 0.69 | $866,931,888 | LITHIUM |

| WA1 | Wa1Resourcesltd | 785% | 12.34 | $536,236,467 | RARE EARTHS, NIOBIUM |

| RDN | Raiden Resources Ltd | 742% | 0.04 | $114,138,662 | RARE EARTHS, NICKEL |

| VMM | Viridismining | 562% | 1.39 | $66,020,195 | RARE EARTHS |

| MEI | Meteoric Resources | 391% | 0.26 | $517,431,160 | RARE EARTHS |

| CXU | Cauldron Energy Ltd | 248% | 0.024 | $27,176,088 | URANIUM |

| GRE | Greentechmetals | 239% | 0.475 | $29,171,267 | LITHIUM, COPPER, ZINC |

| TG6 | Tgmetalslimited | 235% | 0.385 | $20,823,174 | LITHIUM |

| SPR | Spartan Resources | 214% | 0.525 | $505,653,467 | GOLD |

| LRS | Latin Resources Ltd | 191% | 0.285 | $740,358,643 | LITHIUM |

| BEZ | Besragoldinc | 188% | 0.15 | $62,715,136 | GOLD |

| FL1 | First Lithium Ltd | 186% | 0.515 | $36,076,609 | LITHIUM |

| OBM | Ora Banda Mining Ltd | 180% | 0.235 | $392,557,070 | GOLD |

| SUH | Southern Hem Min | 169% | 0.048 | $28,344,302 | COPPER, GOLD, LITHIUM, MANGANESE |

| RIM | Rimfire Pacific | 150% | 0.02 | $44,404,895 | SCANDIUM, COBALT, COPPER |

| WGX | Westgold Resources. | 147% | 2.165 | $1,041,970,006 | GOLD |

| STK | Strickland Metals | 135% | 0.094 | $146,859,581 | GOLD |

| TCG | Turaco Gold Limited | 133% | 0.135 | $73,400,000 | GOLD |

| EQN | Equinoxresources | 131% | 0.3 | $28,834,876 | RARE EARTHS |

| RSG | Resolute Mining | 124% | 0.4475 | $990,008,256 | GOLD |

| OZM | Ozaurum Resources | 120% | 0.145 | $23,018,750 | LITHIUM |

| RAG | Ragnar Metals Ltd | 110% | 0.024 | $11,375,543 | LITHIUM, RARE EARTHS |

| XAM | Xanadu Mines Ltd | 103% | 0.059 | $91,844,317 | COPPER, GOLD |

| IPX | Iperionx Limited | 100% | 1.38 | $304,704,668 | TITANIUM |

| CMD | Cassius Mining Ltd | 100% | 0.04 | $20,104,422 | LIMESTONE, LITHIUM |

| TNC | True North Copper | 98% | 0.105 | $36,374,226 | COPPER |

| IND | Industrialminerals | 94% | 0.755 | $52,257,600 | LITHIUM, SILICA SANDS, QUARTZ |

| SLM | Solismineralsltd | 93% | 0.145 | $12,166,989 | LITHIUM, COPPER |

| KNG | Kingsland Minerals | 90% | 0.285 | $13,372,885 | GRAPHITE |

| AWJ | Auric Mining | 88% | 0.12 | $15,048,853 | GOLD |

| AX8 | Accelerate Resources | 83% | 0.042 | $24,070,274 | LITHIUM, MANGANESE |

| SLB | Stelarmetalslimited | 77% | 0.275 | $14,412,179 | LITHIUM |

| HGO | Hillgrove Res Ltd | 72% | 0.093 | $168,253,449 | COPPER |

| TGM | Theta Gold Mines Ltd | 69% | 0.115 | $84,849,001 | GOLD |

| TLM | Talisman Mining | 68% | 0.235 | $44,255,282 | IRON ORE, COPPER, GOLD, RARE EARTHS |

| A4N | Alpha Hpa Ltd | 65% | 1.055 | $989,827,035 | HPA |

| ACP | Audalia Res Ltd | 64% | 0.018 | $12,458,451 | VANADIUM, TITANIUM |

| WMG | Western Mines | 63% | 0.26 | $18,580,800 | NICKEL, COBALT, COPPER |

| ENR | Encounter Resources | 61% | 0.29 | $124,697,742 | RARE EARTHS, NIOBIUM, COPPER, GOLD |

| GWR | GWR Group Ltd | 59% | 0.094 | $30,033,757 | IRON ORE, MAGNESIUM |

| SXG | Southern Cross Gold | 58% | 1.26 | $117,972,866 | GOLD |

| IPT | Impact Minerals | 57% | 0.011 | $31,511,743 | HPA |

| DYL | Deep Yellow Limited | 56% | 1.09 | $833,010,988 | URANIUM |

| SMI | Santana Minerals Ltd | 54% | 1.01 | $176,942,350 | GOLD |

| RED | Red 5 Limited | 54% | 0.315 | $1,090,589,614 | GOLD |

| WML | Woomera Mining Ltd | 53% | 0.029 | $34,617,142 | LITHIUM |

| BNR | Bulletin Res Ltd | 51% | 0.14 | $41,105,865 | LITHIUM |

| NXG | Nexgenenergycanada | 50% | 10 | $353,779,073 | URANIUM |

| PMT | Patriotbatterymetals | 50% | 1.125 | $505,484,515 | LITHIUM |

| AKM | Aspire Mining Ltd | 50% | 0.105 | $53,301,883 | COAL |

TOP 5 BELTERS (SUB $500M MC)

RAIDEN RESOURCES (ASX:RDN) +742%

Azure Minerals’ (ASX:AZS) huge Pilbara lithium discovery at Andover ignited a rocket under neighbouring explorers. These included RDN, which fast became a market darling after acquiring lithium-rich ground directly to the north and south.

RDN MD Dusko Ljubojevic says the explorer has uncovered “incredible lithium potential” adjacent to Andover, which will likely become a future lithium mine.

“The best deposits get developed. Andover will probably be one of them, and we’ll be right there,” he said.

But until lithium stole the limelight, RDN’s main game was the nearby Mt Sholl, where a maiden resource of 23.4Mt at 0.60% nickel equivalent or 1.54% copper equivalent was released in April.

It is the largest, and currently the only open-pittable, nickel-copper-PGE sulphide resource in the district, 40km from port.

In December, C$6.7bn capped First Quantum (TSX:FM) inked a deal for up to 70% of the project, which comes after a 12-month due diligence period.

To earn 70% equity, First Quantum’s Aussie arm FQMA is required to sole fund minimum $25m over eight years on exploration and project studies, all the way up to a decision to mine.

RDN would also receive $10m in staged cash payments throughout the eight-year exploration cycle.

There’s a lot of value at Mt Sholl that will be realised once nickel as a commodity comes back into focus, RDN MD Dusko Ljubojevic said early September.

“Mt Sholl is a great project,” he says.

“We believe this mineralisation going to come out of the ground at some point, whether we do it or somebody else does it – it’s not going to sit there forever.”

2022 IPO VMM pivoted to rare earths in September with great effect.

It’s Colossus acquisition is within Brazil’s pro-mining state of Minas Gerais and directly adjacent to Meteoric Resources’ (ASX:MEI) Caldeira project.

Caldeira is well known for hosting an existing resource of 409Mt grading 2,626 parts per million (ppm) total rare earth oxides (TREO) – the highest grade for any Ionic Adsorption Clay (IAC) project, with metallurgical testing continuing to show excellent leach extractions for valuable magnet REEs.

IAC projects are ostensibly easier to explore, mine and process, which offsets their low grades compared to their hard rock counterparts.

But the good ones are hard to find. VMM and MEI have now sewn up the available ground in the area prospective for IAC-hosted REE that isn’t held by the big players.

A $2.2m cap raise to fund the Colossus deal was cornerstoned by advanced IAC project developer Ionic Rare Earths Limited (ASX:IXR), which will provide the company additional expertise “to fast-track the Colossus project into development”.

CAULDRON ENERGY (ASX:CXU) +248%

When the WA state government implemented a ban on most new uranium mines in 2017, CXU stopped work at its flagship ‘Yanrey’ uranium project and began searching for other dirt to play with.

But it never really got over the yellowcake fever. With uranium sentiment on the up it has been poking around Yanrey again, already one of WA’s largest deposits.

In December it released a scoping study on the 30.9Mlb Bennett Well deposit at Yanrey which envisaged a 1.5 Mlb U3O8 per annum in-situ recovery (ISR) mining operation.

Upfront capital was estimated to be A$117.7m (US$82.4m), while operating (US$23.23/lb U3O8) and capital costs (US$12.56/lb U3O8) “benchmark well against other similar uranium projects”, it says.

This culminates in a project NPV of A$449M (US$314M) pre-tax at a discount rate of 10%, with IRR of 79% and a payback period of 1.5 years using base case assumptions of US$75/lb U3O8 and 0.70 AUD:USD.

Solid numbers. Now if only the WA government would overturn this ridiculous ban.

TG METALS (ASX:TG6) +235%

TG6’s November spod discovery at its Lake Johnston project, about 450km east of Perth, triggered a pegmatite pegging rush.

The “Tethered Goat” – as Joe ‘Mr Lithium’ Lowry dubbed the company – hit thick, high grade lithium in first holes at the Burmeister anomaly, including a highlight 9m @ 1.35% Li2O from 30m.

The best result to date is 19m at 1.52% Li2O, with the mineralised zone now 1.4km long and counting. More drill assays are pending.

BESRA GOLD (ASX:BEZ) +188%

The former gold battler is now eyeing the big leagues after inking a $US300m offtake and funding deal with bullion dealer and major shareholder Quantum Metal Recovery Inc in March.

This cash – paid over 30 months against future production ounces — would cover development of its 3Moz ‘Bau’ project in Malaysia’s Sarawak region.

With money now filling the coffers, BEZ’ main game in 2024 is commissioning of the pilot plant and updating the 2012 Bau feasibility study.

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.