Where is Australia’s next biggest copper discovery going to come from?

Pic via Getty Images

- Experts forecast a higher pricing scenario for the red metal this year which is good news for copper explorers

- But given Australia hasn’t seen a major copper discovery since Sandfire’s Degrussa, where will the next one be?

- ASX explorers share their thoughts

Copper had a disappointing run in 2023, but brighter days could be around the corner for the mining sector’s ‘everything, everywhere, all at once’ metal used in power generation, power transmission, power distribution, electronic circuity and almost everything that requires electricity.

In a report published earlier this year by market research organisation BMI, factors such as rising demand (driven by the decarbonisation economy) and a likely decline in the US dollar towards the second half of ’24 are set to translate into a higher copper pricing scenario.

BMI, a Fitch Solutions company, has estimated copper’s yearly average price will remain at $8,800/t this year, ~3.14% higher than the $8,523/t average copper price set in 2023.

For junior mining companies looking to make a discovery, this is good news.

Higher commodity prices generally provide companies with greater potential to raise funds for drilling and exploration activities.

It also creates the perfect setting for a healthy wave of market action including M&A deals, new government incentive schemes, and strategic partnerships/joint ventures, all tell-tale signs of a strong economic environment.

The Degrussa story

But Australia hasn’t seen a major copper discovery since Sandfire’s Degrussa mine in 2009, which ceased operations in 2023.

Sandfire, originally on the hunt for a small gold orebody at the Old Highway prospect, decided to explore a few kilometres up the road at another prospect called ‘Degrussa’ after undergoing some problems accessing the ground.

That gold drilling program ended up being a failure, but a young geologist named Margaret Hawke was given permission to drill six extra drill holes in an area where Sandfire had some interesting anomalous gold intersections the year before.

On 18 May 2009, a 22m RC hit grading 3.6% copper, 3.8g/t gold, and 13.4g/t silver unearthed a new high-grade gold-copper discovery.

Within 18 months, the struggling explorer transformed its fortunes from a 4c penny stock into a ~$1bn mining company as countless juniors moved into the region hoping to emulate Sandfire’s success.

The company became Australia’s newest copper producer in 2012 in just over three years from the inital discovery drill hole.

But despite the country hosting nearly 70% of copper resources, Australia hasn’t stumbled across another discovery quite like it.

NOW READ: This is how copper play Sandfire went from 4c to over $8 in 18 crazy months

Where will the next big copper discovery be?

That might sound a little unusual given the upward trend of copper exploration in the country over the past ~7 years (which rose to $183m in September ’23) but according to S&P, the size and rate of global copper discoveries has dwindled over the past decade.

This boils down to two primary issues – the time between a discovery hole and the point at which growth in its reserves and resources defines it as a major discovery and an industry trend away from grassroots exploration spending.

That said, remote regions like the West Musgrave in WA are quickly turning into a hotbed of exploration activity, partly due to the prospectivity of the area as well as the infrastructure development taking place.

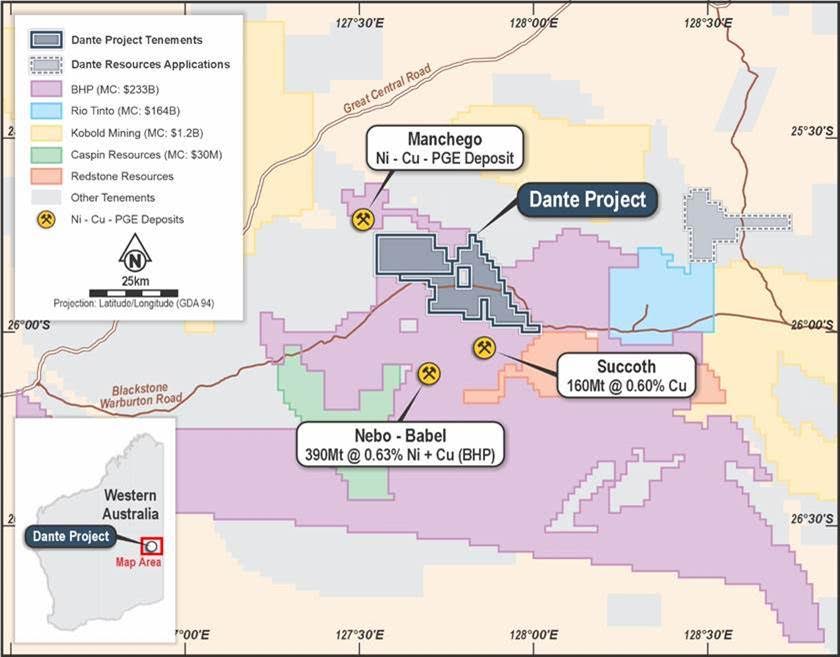

One explorer in the area is GCX Metals (ASX:GCX), owner of the Dante project which is surrounded by mining majors including BHP (ASX:BHP) and its 390Mt Nebo-Babel nickel-copper-PGE project currently under construction and the likes of Rio Tinto (ASX:RIO), Caspin Resources (ASX:CPN) and Redstone Resources (ASX:RDS) exploring tenure in the province.

In an interview with Stockhead, GCX managing director Thomas Lines said the West Musgrave has one of the best shots in Australia – if not globally – at delivering the next copper discovery of scale simply due to it being a “very well endowed” copper province.

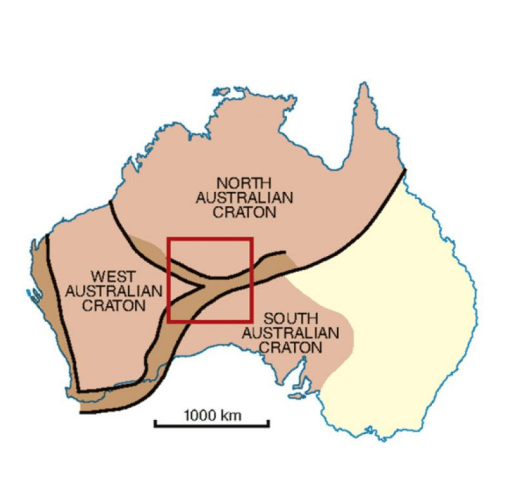

It is host to the Giles Complex, a geological formation comprising of PGE reefs commonly compared to the 2.2 billion-ounce South African Bushveld Complex.

According to Lines, the uniqueness of the West Musgrave comes down to it being one of only a handful of places in the world to have produced this metallogenic geological setting.

“This type of setting typically produces large, magnetic sulphide deposits and it’s at the triple point junction of three large cratons – the North Australian craton, the West Australian craton and the South Australian craton,” he says.

“This junction has created a magmatic hot spot which has brought up these rare, large intrusions and complexes.

“BHP’s almost 400Mt Nebo Babel deposit is one of them and a couple of kilometres from that is OZ Minerals’ 160Mt Succoth deposit,” Line says.

“Collectively, there’s over two and a half million tonnes of copper metal there and it’s still very underexplored despite these large resources being there.”

Opening up WA’s West Musgrave region for more exploration

Another added bonus is the major de-risking BHP’s $1.7bn mine development is bringing to the province.

“Along with the mine itself, BHP plans to develop processing facilities, a borefield, temporary and permanent waste landforms, a tailings storage facility, accommodation, airstrip and power infrastructure,” he says.

“They are flying 10 flights up there every single week, they’ve got about 300 people on site, and they’re bringing in a huge amount of infrastructure.

“All of that is encouraging further investment which will start to open up the province for more exploration expenditure,” Line adds.

Alma’s search for the next big copper find in QLD

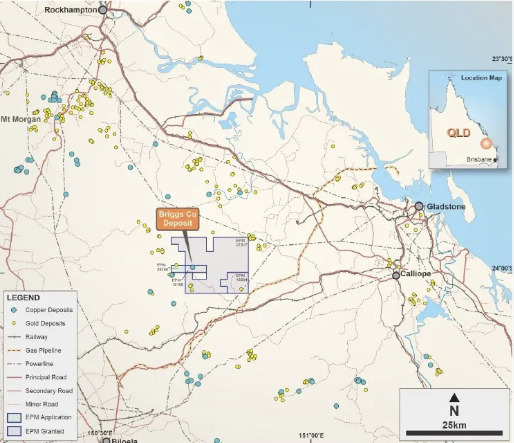

Over in central Queensland, Alma Metals (ASX:ALM) is earning a 70% stake in the Briggs copper-molybdenum project from Canterbury Resources (ASX:CBY) via the spending up to $15.25m on exploration over a period of nine years.

Its interest in Briggs is fuelled by the easy-mining, shallow-porphyry nature of the deposit.

Porphyry mines are huge, responsible for ~60% of the world’s copper, most of the world’s molybdenum, and significant amounts of gold and silver.

While they typically have lower grades between 0.2% to 0.7% copper equivalent, this is more than made up for by their large volumes.

One leg up for the company is the fact that Briggs is already among Australia’s top 10 undeveloped copper projects with an inferred resource of 415Mt grading 0.25% copper and 31ppm molybdenum and ~1Mt of copper metals along with +28.6Mlb of molybdenum.

ALM’s tenements, inland from Gladstone, are situated at the southern end of the Mt Morgan structural belt, home to the high-grade Mt Morgan mine which produced ~8,000oz of gold and 350,000t of copper before its closure in 1989.

ALM CEO and executive director Frazer Tabeart told Stockhead the location of Briggs in the predictable and mining friendly state of Queensland, in an area which is being prioritised for green industrial development, bodes well.

“From our point of view, it ticks all the boxes – we know the mineralisation is at surface so the strip ratios are likely to be low, we know there’s low cost power there, we are close to deep water ports and railway lines so transport isn’t going to be an issue,” he says.

“If you’ve got a low-grade large deposit in a stable jurisdiction with good infrastructure, good metallurgy, and low stripping ratios… it almost certainly will work, subject to doing your feasibility studies.”

Room to grow

From an exploration standpoint, things are looking promising for ALM with final assays from 2023 core drilling having extended the known strike length of higher-grade mineralisation along the eastern contact zone of the Briggs Central deposit to 500m.

There’s also potential for further growth of this higher-grade zone with a detailed soil sampling program returning strong copper anomalism along the entire south-western margin of the intrusion.

Drilling to evaluate the intrusive contact zone is planned to start in early Q2 2024 with ALM targeting an upgrade in resource confidence, sufficient to support a scoping study later this year.

Saddling up with FMG to hunt for copper

Strategic Energy Resources (ASX:SER) is another explorer looking for the next big copper deposit in Queensland but unlike ALM, SER’s joint exploration efforts with Fortescue subsidiary FMG Resources are focused on Ernest-Henry style IOCG targets in the northern part of the state.

Evolution’s Ernest Henry mine comprises one of the largest copper reserves in Australia with its latest pre-feasibility study in June 2023 highlighting an increase of 126% in ore reserves to 77.4Mt and extending the life of mine by 17 years to 2040.

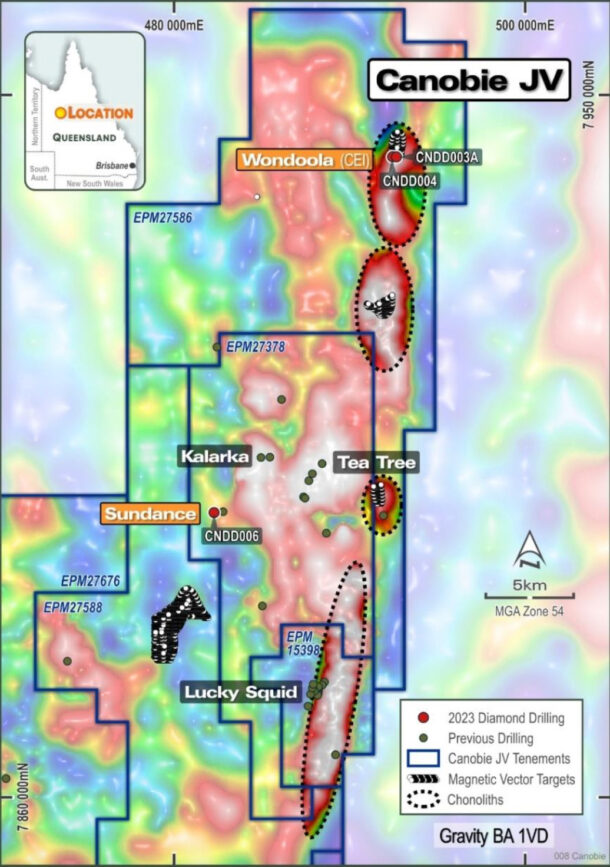

Luckily for SER, the Ernest Henry magnetite IOCG deposit lies on the same crustal-scale fault system and within the same geological domain as its Canobie project.

Canobie, a +2,300km2 project, boasts three Tier 1 targets (Sundance, Apollo Bore, and Alcala) that are deep and significant in size.

“In big broad terms, we hope that one of these targets is the next Ernest Henry,” SER managing director David DeTata told Stockhead.

FMG Resources recently completed its first field season at the project, encountering alteration that is consistent with precursor alteration in IOCG deposits throughout the district.

Datasets from the exploration program will be assessed to refine the exploration model and select next targets.

Copper stocks share prices today:

Related Topics

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.