These 7 near term miners are preparing to profit from the approaching copper crunch

Pic: iStock / Getty Images Plus

The impending copper shortage has been a slow-moving car crash, years in the making.

Despite the mountain of cash spent on exploration every year, we aren’t finding the big tier 1 deposits fast enough to replace existing – and increasingly depleted — operations.

Just look how major discoveries have petered out over past decade especially:

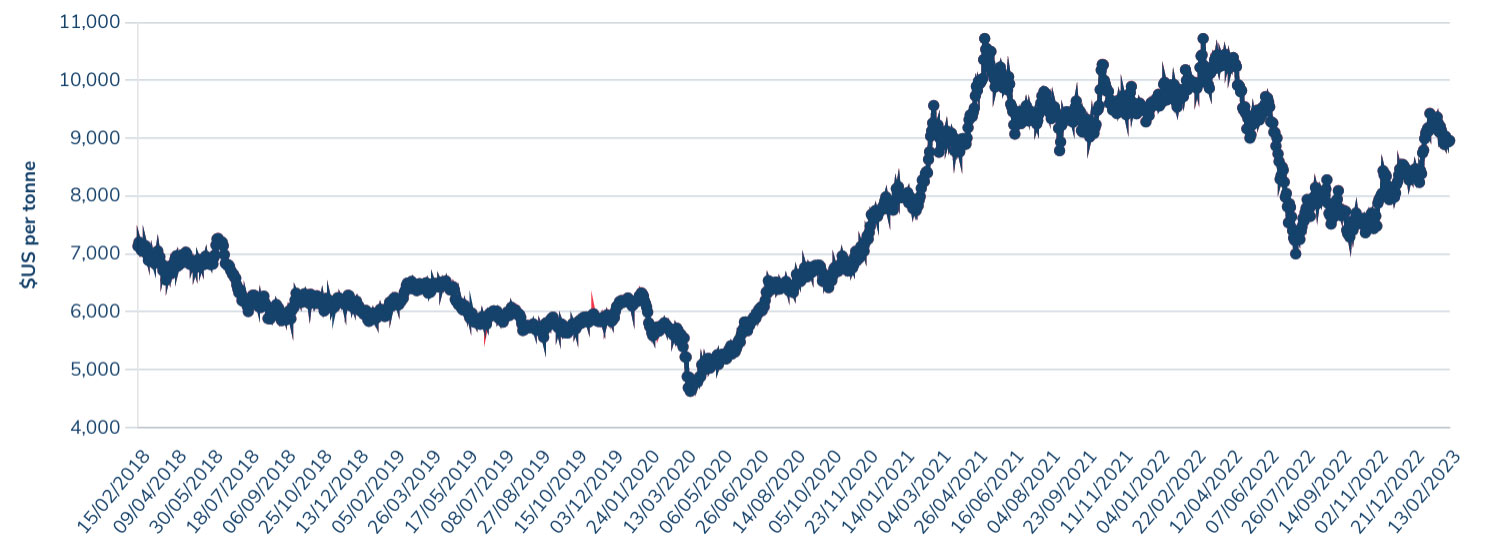

— Robert Friedland (@robert_ivanhoe) February 11, 2023

It has forced the majors like BHP (ASX:BHP) and Rio (ASX:RIO) to look to expensive M&A to grow their copper exposure – great for them, but the equivalent of shuffling deckchairs on the Titanic for global production.

Meanwhile, demand is set to go through the roof, thanks to the electrification thematic.

EVs, for example, need up to five times more copper than an internal combustion passenger car (~30kg) and, like lithium to a lithium-ion battery, there are no viable substitutes.

Expansion of electricity grids to handle renewable energy will also see copper demand for power lines alone double by 2040, according to the International Energy Agency.

Goldman Sachs thinks we’ll need 8Mt of additional copper by 2030.

It’s a number that doesn’t sound so high until you consider that would mean 8 replicas of BHP and Rio Tinto’s Escondida mine, the world’s largest.

To incentivise that extra 8Mt of production, prices above US$13,000/t would be needed, Goldman says – a big jump from current prices around ~US$9000/t.

All this is great news for a small collection of junior ASX copper stocks looking to enter production over the next few years.

Which ASX stocks are set to take advantage of the looming copper crunch?

HILLGROVE RESOURCES (ASX:HGO)

Market Cap: $70m

Copper-gold ore was mined from an open pit at HGO’s Kanmantoo mine in South Australia between 2011-2019 before it was put into care and maintenance so HGO could prove up more resources.

An underground mine is now being developed with the aim of resuming production in 2023. Just look at this wall of money:

Stage 1 development would see HGO produce 36,000t copper and 10,000oz gold over three years at all in sustaining cost of $6,991/t – giving it a nice margin at current prices above $12,800/t.

Because of all the existing infrastructure – including a 3.6Mtpa processing plant — Kanmantoo will cost just ~$30m to bring back online, according to the December 2021 study.

Since this study, the resource has increased by 1.2Mt (21%) which is expected to increase the mine plan.

The funding process is well advanced, with first production pencilled in for this year.

The company says it is highly leveraged to higher copper prices, because the underground stopes are designed to cut-off grades based on the current copper price.

“At higher prices, there is potential to grow the existing plan by simply widening stopes for relatively low incremental cost,” the company says.

“With the mill only being utilised at 40% capacity, and excess tailings storage capacity, additional mineralised material can be processed without displacing any high grade — essentially feeding more copper into a higher price environment for low incremental cost.

“This is a very unique competitive advantage at Kanmantoo as most other producers would need to work through time consuming and expensive permitting and construction to expand their production footprint in this manner.”

DEVELOP (ASX:DVP)

Market Cap: $570m

Legendary former Northern Star boss Bill Beament has already grown this underground mining contractor/mine developer 530% since leading a recapitalisation and rejuvenation effort in early 2021.

DVP has two advanced development assets, Woodlawn (NSW) and Sulphur Springs (WA), where it aims to ramp up to +50,000tpa of copper equivalent metal, starting from 2024.

The mothballed Woodlawn zinc-copper mine requires minimal capital outlay to resume production due to existing extensive infrastructure.

Drilling and mine studies are underway, with DVP aiming to advance financing in the second half of 2023 so Woodlawn is “operationally ready” in 2024.

At the advanced Sulphur Springs zinc-copper project in the Pilbara, DVP is updating current mining studies, so it is “shovel ready” by the middle of 2023. Financing will follow, it says.

REX MINERALS (ASX:RXM)

Market Cap: $170m

RXM’s focus is the advanced, fully permitted Hillside project in South Australia.

It is one of the largest undeveloped copper projects in Australia, with a resource of 1.9Mt copper and 1.5Moz gold.

A detailed December 2022 project study envisaged stage 1 production of 42,000t copper and 30,000oz gold per year over an initial 11 years.

It has a net present value (NPV) and internal rate of return (IRR) of $847m (post tax) and 19%, respectively, at a consensus copper price of US$3.92/lb.

At Goldman Sachs ‘Demand Case’ price of US$5.90/lb, NPV and IRR jump to $2.17bn and 37%, respectively.

It would cost $854m to build, inclusive of contingency.

Financing talks are underway, with RXM targeting a final investment decision mid-year.

If all goes to plan, first concentrate delivery will occur Q4 2025, “to align with the beginning of the forecast global copper market deficit”.

CYPRIUM METALS (ASX:CYM)

Market Cap: $70m

CYM is hoping to revive the long troubled 940,000t Nifty copper mine in WA.

Discovered originally by WMC in WA’s Pilbara, India’s Aditya Birla and ASX-listed Metals X (ASX:MLX) have both failed to make Nifty a money spinner. But in a higher copper price environment CYM is hoping to realise the mine’s potential.

A recent $35m cap raise will be mostly put towards financing the restart of Nifty, which is expected to produce ~25,000t of copper metal a year for 6.3 years in Phase 1.

It boasts strong numbers, including an IRR and NPV of 37% and $277m, respectively. The project will cost $134m to get back online, including contingency.

“The restart project economics remain very robust and are further enhanced based on current copper prices of $13,000 per tonne which is above those applied in the Nifty copper project restart study,” CYM MD Barry Cahill said last month.

Phase 2 will continue the open pit into the sulphide portion of the orebody for a +20-year mine life.

CYM is aiming for a H1 2024 restart.

ALARA RESOURCES (ASX:AUQ)

Market Cap: $26m

AUQ says construction of its 51%-owned Al Wash-hi Majaza copper-gold project in Oman remains on track for completion in the June 2023 quarter.

These are exciting times for the company, which has been plugging away at this project for well over a decade.

A revised DFS envisaged a smallish open pit operation producing 35,000tpa concentrate a year for ~80,000t copper and 21,800oz gold over 10 years. It will cost about US$60m to build.

At US$7,000/t copper, earnings before tax (EBITBA) were estimated at US$208m.

At a US$9,500/t copper price, project EBITDA increases to US$370m, AUQ says.

“In an exciting development just after quarter’s end, we informed the market that high-grade copper sulphide ore had been encountered when developing the Wash-hi mine pit,” AUQ managing director Atmavireshwar Sthapak said January 31.

“With the completion date of the project now in clear sight, we are much closer to that day when Alara will start generating a material revenue stream from copper production entering a market with still favourable demand/supply dynamics.”

KGL RESOURCES (ASX:KGL)

Market Cap: $90m

KGL’s main game is the Jervois copper project in NT, where the plan is to produce 30,000 tonnes of copper per year, plus silver and gold.

A feasibility study (FS) released late last year outlined “one of the highest-grade copper developments in Australia”, which KGL hopes to bring into production from 2025.

Here are some of the key FS takeaways:

- Project construction cost: $298 million

- Mine life: 75 years

- Annual production: 24.7kt of Cu metal in concentrate with gold and silver payable credits

- An NPV (8% real, after tax) of $241m, IRR of 20.7%, payback of 4.2 years

Those metrics are based on a long-term copper price of US$9,326/t.

If prices hit +US$13,000/t, as some experts predict, NPV and IRR jump to $701m and 40.1%, respectively.

The focus in 2023 will be project financing and growing the high-grade 23.8Mt at 2.02% copper, 25.3g/t silver and 0.25g/t gold resource, KGL says.

“We are looking forward to making the necessary progress to start construction in 2023, subject to achieving some normalisation in market conditions – more specifically, the availability of labour, pricing of key inputs and supportive macroeconomic conditions,” it says.

ANAX METALS (ASX:ANX)

Market Cap: $26m

In 2020, ANX purchased an 80% stake in the mothballed Whim Creek VMS project from DEVELOP, which retains a free carried 20% interest through to a decision to mine.

Open pit mining had previously lasted six years, before stopping in 2009 due to the sharp drop in the copper price following the global financial crisis.

The project now includes four deposits at Mons Cupri, Whim Creek, Salt Creek and Evelyn containing a total 112,000t copper, 69,000t zinc, 18,000t lead, 4.3Moz silver and 43,700oz gold.

A 2021 scoping study envisaged ~11,000t per annum copper production (Cueq) over an initial 5-7 years for free cash of ~$291m.

It would cost about $55m to (re)build.

A DFS is due to be released soon and, if that goes well, a final investment decision pencilled in for Q3.

“Despite ongoing inflationary pressures and supply chain constraints the project continues to demonstrate robust financial metrics,” the company said late January.

“The proposed underground mines at Salt Creek and Evelyn provide further upside to the projected metrics and both assets are open for immediate growth.”

Resources at the Evelyn satellite deposit were recently upgraded to 14,900t copper, 22,800t zinc, 18,500oz gold and 779,000oz silver.

ANX already has $US20m in debt funding locked in from global miner Anglo American, subject to the results of the DFS.

Related Topics

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.