The vanadium market is in deficit until 2024. Here are seven ASX stocks to watch

Pic: Getty

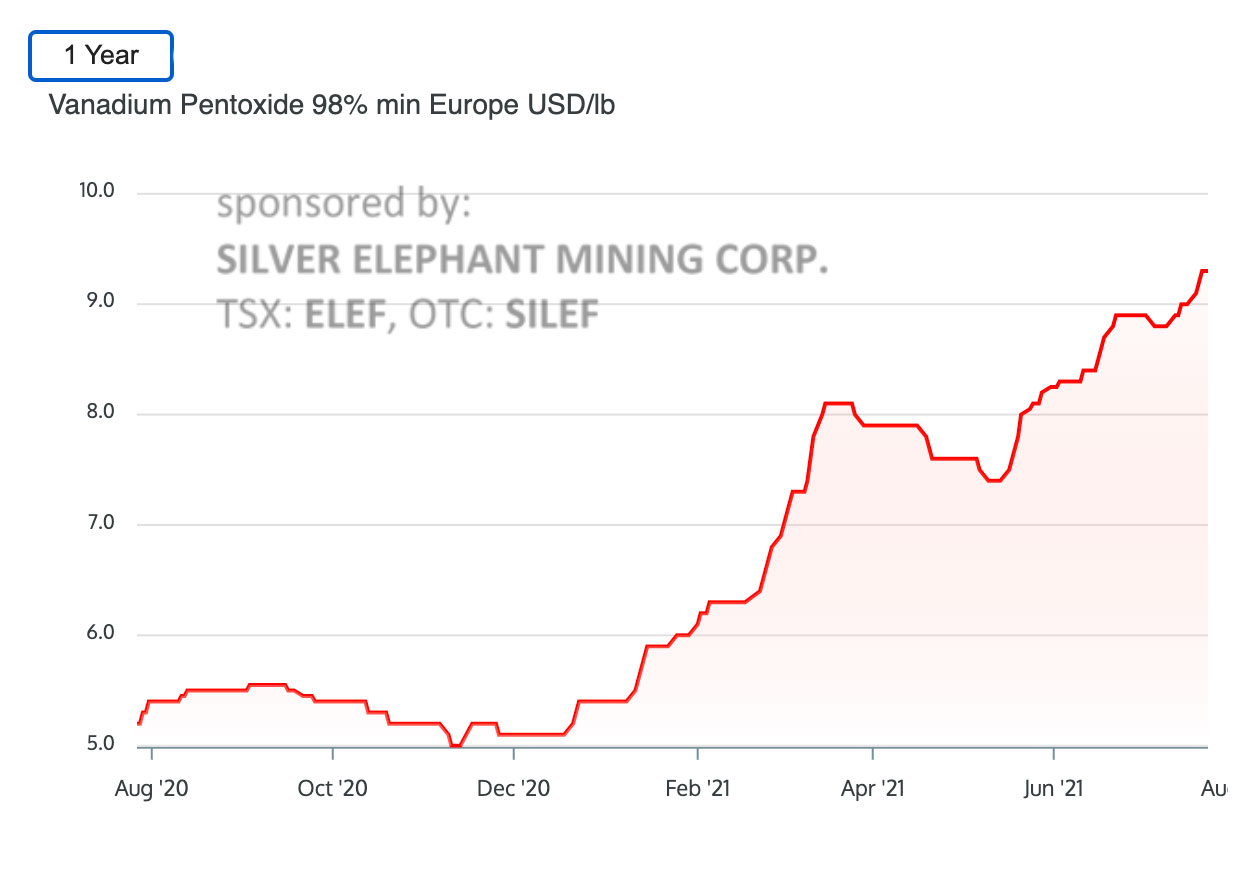

After a few years in the wilderness, vanadium demand is making a comeback as steel consumption soars, in China and overseas.

92% of vanadium consumption is used to strengthen steel. Of the remainder, most is used in aerospace alloys and chemical catalysts, and 1% goes into vanadium redox flow batteries (VRFBs).

The party is set to continue — vanadium supply is likely to remain constrained until 2024, Roskill’s steel alloys principal consultant Erik Sardain says.

“If you look at the world ex-China, we aren’t probably going to see a huge increase in terms of vanadium supply – we might even see some declines,” he told Stockhead.

“Largo Resources is not going to increase production a whole lot, while Bushveld Minerals has been cutting guidance and all the unrest in South Africa won’t help either.

“Chinese [steel mills] are always a little trickier to predict, but I believe that they are probably very close to their production capacity [of vanadium slags].”

The market is going to shift from surplus in 2020 into deficit in 2021, Sardain says.

“Moving forward in the next couple of years, supply is likely to remain tight in 2022 and 2023 until new projects come online from 2024.”

Vanadium batteries: the wildcard

In 2018, the Hornsdale lithium-ion power reserve — also known as ‘Tesla’s Big Battery’ – was built in South Australia.

Much maligned and misunderstood early on, the positive impacts of the battery’s services have well and truly been recognised. Lithium-ion stationary storage has since exploded.

Unlike lithium-ion, vanadium redox flow batteries (VRFBs) – a perfect fit for stationary storage — are yet to have their ‘big battery’ moment.

Right now, it’s mostly a case of ‘talk the talk’, not ‘walk the walk’, Sardain says.

“It is early days. In 2021 we expect to see some new installations, but it will probably remain quite small in 2021,” he says.

“Our base case is that by 2030, 10% of vanadium demand is going to come from batteries [up from ~1% currently].

“But if the tech develops, this estimate will be far too low; if it doesn’t take off, that estimate is far too high.”

In other words, vanadium batteries are a binary proposition. It is either going to work, or not.

One thing is clear — China will be the driver if the technology is to succeed.

“I strongly believe that the VRFB technology is going to come from China, or it is not going to happen,” Sardain says.

“If the Chinese demand take off the rest of the world will follow.

“Is the tech going to be developed, or will another tech turn out to be more economical? It is difficult to say.

“We have to see how things develop in the next 2-3 years.”

Australian vanadium stocks to watch

MARKET CAP: $64.5 million

AVL is developing the $US399m ($541m) Australian Vanadium project at Gabanintha in WA.

A Bankable feasibility Study (BFS) – the most advanced of all project studies – is progressing towards completion in 2021.

The project expects to produce 24.3 million pounds (11,022 tonnes) of V2O5 per annum at a low all-in cost of $US5.04/lb, over an initial mine life of 25 years.

MOUs for offtake are “in place and under negotiation” for 100% of production, the company says.

“AVL is developing one of the highest-grade vanadium projects currently underway in the world,” managing director Vinca Algar says.

“Our aim is to become a low-cost producer, able to withstand long-term commodity price cycles.”

The company’s subsidiary VSUN is also marketing and selling batteries.

MARKET CAP: $47 million

TMT’s ‘Gabanintha’ vanadium project – right next door to AVL — would also boast industry-leading operating costs.

A 2019 DFS envisaged average annual production of 12,800 tonnes a year V2O5 over an initial 16-year mine life.

The ~$454m construction costs could be paid back with 3.2 years, the company says.

6,000 to 10,000 tonnes of TMT’s proposed production is now covered under Binding Offtake and MoU.

Market engagement is ongoing for additional product offtake and funding options.

MARKET CAP: $300 million

The battery metals specialist is aiming to turn slag – a vanadium bearing steel by-product – into high value vanadium products using a propriety process.

The ‘Vanadium Recovery Project’ (VRP) JV would be constructed in Finland to recover and produce sustainable high-grade vanadium products from slag stockpiles in Scandinavia.

Neometals is funding and managing feasibility studies up to a final investment decision, which — if positive — will earn Neometals a 50% interest in the joint venture.

In June, a pilot plant campaign (smaller version of the real thing) kicked off to process ~13 tonnes of vanadium-bearing slag over 22 days.

If successful, it will confirm the technical feasibility of Neometals’ proprietary process at scale and provide V2O5 samples for evaluation by potential offtakers.

“We are confident that this pilot which will further reinforce a business case underpinned by industry-leading sustainability credentials, exceptional grade stockpiled feedstocks and robust potential financial metrics,” Neometals managing director Chris Reed says.

MARKET CAP: $9.3 million

The ‘Abenab’ vanadium project in Namibia was the highest-grade deposit of vanadate ore in the world from 1921 to 1947.

This ore type is different – and better, Golden Deeps says — to all other primary vanadium projects.

It is simpler to beneficiate, and concentrates to a very high level for further processing either on-site or by other offtakers.

A recently released Mining Study established potential for new high-margin vanadium (lead-zinc) underground mining operation at Abenab.

Studies are now underway to produce V2O5, Zn & Pb on site.

MARKET CAP: $88.5 million

TNG’s mammoth $852m ‘Mount Peake’ operation expects to produce 6000tpa of vanadium pentoxide – about 3.2% of current world demand – as well as 100,000tpa of titanium dioxide pigment and 500,000tpa of iron fines.

While a $852m capex project is an ambitious undertaking for $88m market cap TNG, the company has a life of mine binding offtake agreements for up to 100% of projected vanadium production.

Vanadium sales would make up about 30% of TNG’s estimated revenue.

Like AVL and TMT, TNG is now looking to finalise the rest of its approvals and bed down financing.

It is also planning to use its vanadium resources to build batteries. The company recently partnered with Singapore’s V-Flow Tech to deliver power systems underpinned by the energy storage technology.

VANADIUM RESOURCES (ASX:VR8)

MARKET CAP: $23.5 million

VR8’s downside: it operates in South Africa, a rough jurisdiction right now.

VR8’s upside: ‘Steelpoortdrift’ one of the world’s largest deposits, located within the famous, vanadium-rich Bushveld Complex.

A recent pre-feasibility study – the first proper look at whether a project is economic or not – indicates the Steelpoortdrift project “is well positioned to become a significant high volume and low-cost producer”.

The 39 million pounds (17,700 tonne) per annum project would cost a relatively low $US200m ($271m) to build.

It has an impressive net present value (post tax) of $US1.2 billion and internal rate of return (post tax) of 45%.

Operational costs are an impressive $US3.08/lb V2O5, the company says.

It is also one of the few vanadium resources globally with a mining right granted, which includes environmental approval.

MARKET CAP: $18 million

QEM is +150 per cent since announcing plans to study “green hydrogen opportunities” at its Julia Creek vanadium and oil shale project in Queensland.

Green hydrogen burns cleanly and emits only water, making it the ‘holy grail’ of renewable energy.

The JORC (2012) Mineral Resource of 2,760 million tonnes at 0.30% V2O5 is low grade, but represents one of the single largest ASX-listed vanadium resources “and a significant opportunity for development”.

Related Topics

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.