Resources Top 5: A porphyry hunter joins the 10-bagger club for 2021, Marvel shareholders enjoy a spinoff windfall

Pic: Tyler Stableford / Stone via Getty Images

- Marvel’s holding in graphite spinoff Evolution is now valued at $25.5m

- Caspin may have hit ‘significant body of mineralisation’ near Julimar

- More thick, high-grade copper-gold hits from Sunstone, which is now up 1,000% in 2021

Here are the biggest small cap resources winners in early trade, Friday November 26.

MARVEL GOLD (ASX:MVL)

MVL graphite spinoff Evolution Energy Minerals (ASX:EV1) is one of 2021’s hottest IPOs.

As at the close of trading on November 25, the EV1 share price was $0.51 per share, a 155% premium to the IPO price of 20c per share.

This has been a windfall for MVL. Based on this closing price, its holding in Evolution (31%) is now valued at $25.5 million.

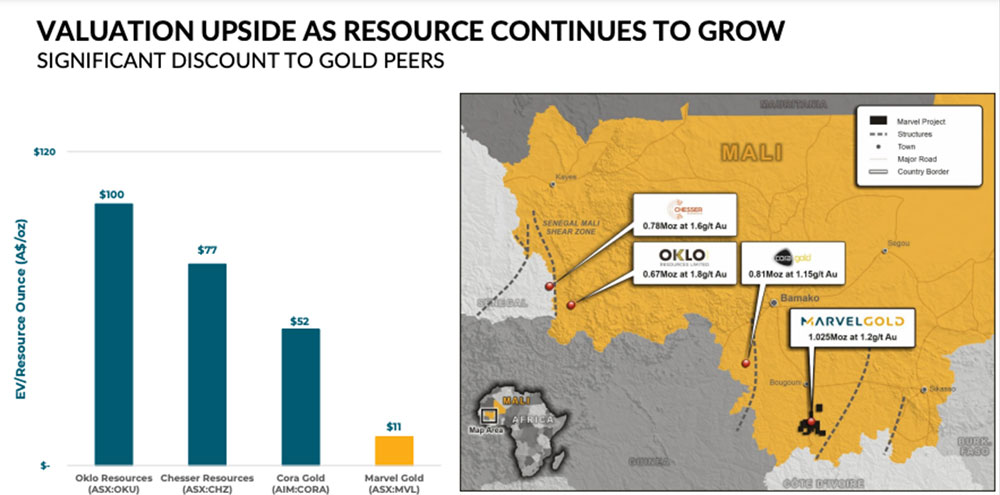

This equates to a valuation of $0.043 per Marvel share, which results in an enterprise value for Marvel after subtracting cash and this listed investment of $11 million — or $11 per resource ounce.

That’s super cheap, it says. Just look at this peer comparison:

MVL is sitting on ~1Moz of gold at its ‘Tabakorole’ project in southern Mali, a region which includes Firefinch’s 7.5Moz Morila gold mine and Resolute Mining’s 7Moz Syama gold mine.

It also has a strong pipeline of regional targets, with a mammoth 15,000m auger and 15,000m aircore drill program now underway.

The company is assessing its options with respect to the EV1 investment “to ensure value is maximised for shareholders”, MVl managing director Phil Hoskins says.

The $45m market cap stock is up 10% over the past month, and 54% year-to-date.

MVL had about $5.2m in the bank at the end of the September quarter which, alongside this $25.5m windfall, gives the company plenty of cash to either return to shareholders or sink into exploration/acquisitions.

MVL, EV1 share price charts

CASPIN RESOURCES (ASX:CPN)

CPN was demerged from Cassini Resources, which was acquired by copper major OZ Minerals (ASX:OZL) in October last year for its ‘West Musgrave’ copper-nickel project.

What’s interesting about CPN is that it was the only explorer looking for nickel-copper-PGEs near Perth, WA, before Chalice Mining (ASX:CHN) moved next door and hit the motherlode in its very first hole.

That’s right — CPN is arguably the Julimar region OG.

Its main game is ‘Yarawinda Brook’, where drilling at the ‘XC-22’ anomaly has just intersected significant nickel and copper sulphides.

Based on visual observations, the mineralised zone is at least 40m thick with up to 20% sulphides over the first 2m and becoming more disseminated (scattered) at depth.

“The large size of the XC-22 anomaly suggests that if it is coincident with mineralisation throughout its entire extent then this could represent a significant body of mineralisation,” CEO Greg Miles says.

“Many more drill holes are required before this can be confirmed as a significant discovery and laboratory assays are required to confirm the tenor of any PGE mineralisation that may be present.

“This is an exciting development for the Yarawindah Brook Project and the results to date have given us reason to review similar AEM anomalies in the region that, in light of this new information, are potentially significant.

“We look forward to providing further updates on RC drilling at XC-22 and the interpretation of stratigraphic diamond hole YAD0019 as they come to hand.”

The $86m market cap stock is up 37% over the past month, and 118% year-to-date. It had $13.7m in the bank at the end of September.

SUNSTONE METALS (ASX:STM)

More extremely wide, high-grade hits from this popular South American porphyry hunter, which is now up 1,000% in 2021. 10-bagger confirmed.

The third hole from the ‘El Palmar’ gold-copper discovery in northern Ecuador just returned 105.09m at 0.75g/t gold and 0.20% copper (1.07g/t gold equivalent) from just 32m depth.

Assays now show significant grades and widths of gold and copper porphyry in five holes (EPDD001-EPDD003, and historic holes CED01 and 02) across a 300m long zone, which remains ‘open’.

Drill holes 4, 5, and 6 have been completed (assays pending), and hole 7 is underway. All holes are mineralised from shallow depths, STM says.

This is a big find that could get a lot bigger, the company says.

“Results support Sunstone’s view that only the upper portion of a porphyry system has been drilled so far, and this likely extends to considerable depth, and a second drill rig is mobilising to site to test the depth extent,” it says.

Porphyries are huge deposits responsible for ~60 per cent of the world’s copper, most of its molybdenum, and significant amounts of gold and silver. Their easy-mining large volumes make up for the low grades, typically between 0.3 per cent to 1 per cent copper equivalent.

At STM’s high-grade ‘Alba’ gold target on the Bramaderos Project in southern Ecuador, drilling of the second hole is set to start this weekend.

Last week, the company reported a maiden drill hole at Alba which pulled up an incredible 111m long intersection grading 2.3g/t – including 7.2m at 26.9g/t.

Monstrous.

The $250m market cap stock is up 83% over the past month, and 1,000% year-to-date. STM is well funded with ~$19mill in cash and equities.

KORAB RESOURCES (ASX:KOR)

(Up on no news)

This long time battler has moved quickly to profit from positive investor sentiment in the supply constrained magnesium and phosphate markets.

Earlier this month it decided to pull the pin on the planned sale of its increasingly valuable Winchester (magnesium) and Geolsec (phosphate) projects in the Northern Territory.

Over the last few months, KOR says it has been approached by two separate groups expressing an interest in developing the ‘Winchester’ magnesium project in the NT.

The latest unsolicited proposal would see the two parties “jointly develop the Winchester quarry where the other party will fully fund the development in exchange for sharing the future profits from the quarry”.

The company says it is also in discussions with magnesium metal users and magnesium buyers, including car makers (Fiat and Daimler), and aluminium/magnesium alloy producers.

Last week it inked a Heads of Agreement (HOA) – a non-binding deal to look at signing a real agreement – with Darwin Port for the export of up to 30,000 tonnes per annum of magnesium metal.

“The HoA with Darwin Port will allow for exporting of large quantities of high purity magnesium metal to Europe, USA, and Asia, where users of this critical metal have been suffering repeated shortages and supply interruptions that are likely to continue,” the company says.

The $30m market cap stock is up 1% over the past month and 710% year-to-date. The stock had ~$2m cash at the end of September, plus a small financing facility.

WHITE CLIFF MINERALS (ASX:WCN)

(Up on no news)

A good week for WCN, which yesterday raised $912,000 at 1.2c per share – equivalent to the last closing price – to hit the ground running at a couple of soon-to-be-acquired lithium and rare earth element (REE) projects in WA.

At the ‘Yinnetharra’ project, exploration historically focused on uranium, but sampling by Geological Survey of Western Australia (GSWA) showed the potential for lithium and REEs.

The ‘Preston River’ lithium project is 30km from the world-class Greenbushes lithium (+Sn/Ta) project and “situated in similar geological terrane”, WCN says.

After the acquisition completes, the company says it will hold over 4,000sqkm of lithium and REE tenure “within proven jurisdictions and nearby to operating mines and/or recent discoveries”.

Cash will also be used for ongoing exploration at the ‘Reedy South’ gold project.

Subject to shareholder approval, WCN company directors will apply for up to $60,000 worth of shares on the same terms as the placement.

The company already had $1.2m in the bank at the end of the September quarter. The $10m market cap stock is down 10% over the past month, and 40% year-to-date.

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.