Resources Top 4: Another junior drawn to the yellowcake, Richmond preps for vanadium bull market

Pic via Getty Images

- Koba buys 80% interest in uranium rights at Yarramba project in South Australia from copper-gold play Havilah (ASX:HAV)

- Project developers Castile (copper, gold), Richmond (vanadium) spike on no news

- At least one lithium play is enjoying a win today as Future Battery Minerals drills into thick, high grades at Nevada project

Here are the biggest small cap resources winners in early trade, Monday January 22.

KOBA RESOURCES (ASX:KOB)

South Australia has become a go-to uranium jurisdiction during this current boom, as speculative stocks look to replicate the success of mine developer Boss Energy (ASX:BOE) and long-time producer Heathgate.

KOB is now joining minnows like Marmota (ASX:MEU) , Norfolk Metals’ (ASX:NFL), Power Minerals (ASX:PNN) and Adavale Resources (ASX:ADD) in the hunt for a uranium company maker in Australia’s third largest state.

KOB will buy an 80% interest in uranium rights at the 4000sqkm Yarramba project from copper-gold play Havilah Resources (ASX:HAV) for 25m shares, and another 10m milestone shares on announcement of a +15Mlb resource.

KOB will need to spend $6m over four years on exploration, with HAV’s 20% interest ‘free-carried’ until completion of a feasibility study.

Drilling is pencilled in for Q2 this year.

“The Yarramba project is centred on 4.6 million pounds of U3O8 at the Oban deposit which provides a great foundation on which substantial resources can be built,” KOB boss Ben Vallerine says.

“No exploration has been undertaken at Yarramba since 2012, therefore the 4,000km2 project provides us excellent opportunities to make sizeable discoveries in close proximity to existing infrastructure.”

Vallerine says the explorer will also “aggressively pursue additional uranium assets”.

HAV, down 40% since BHP pulled out of a ~$405m deal to buy the Kalkaroo copper-gold project late last year, is up marginally in early trade.

CASTILE RESOURCES (ASX:CST)

(Up on no news)

CST is surging on outsized volumes this morning on no news.

In 2020, Top 10 Aussie gold producer Westgold Resources (ASX:WGX) spun its Northern Territory gold-base metal assets into Castile, which hit the bourse with a market cap of about $40m.

Gathering dust in the basement of Westgold’s portfolio for several years was Castile’s high-grade – but deep — Rover 1 iron oxide-copper-gold discovery.

According to a recent PFS Rover 1 could churn out 28,700oz gold, 6,900t copper, 300t cobalt and 75,300t iron per annum for $225m in annual revenues.

The development has solid copper and gold equivalent all in sustaining costs (AISC) of A$7030/t and A$1330/oz, respectively. It would cost A$280m to build.

A BFS – the most advanced of all economic studies – is due sometime this year. Formal discussions with customers and financial institutions for project funding is also underway, with CST boss Mark Hepburn recently travelling to India as part of a trade delegation.

“From the meetings we attended it is obvious that India will require vast amounts of copper to meet their decarbonisation goals,” he said in December.

“Castile’s strategy of producing end-user 99% copper means we can negotiate directly with these large companies, securing maximum value for our product and our shareholders.”

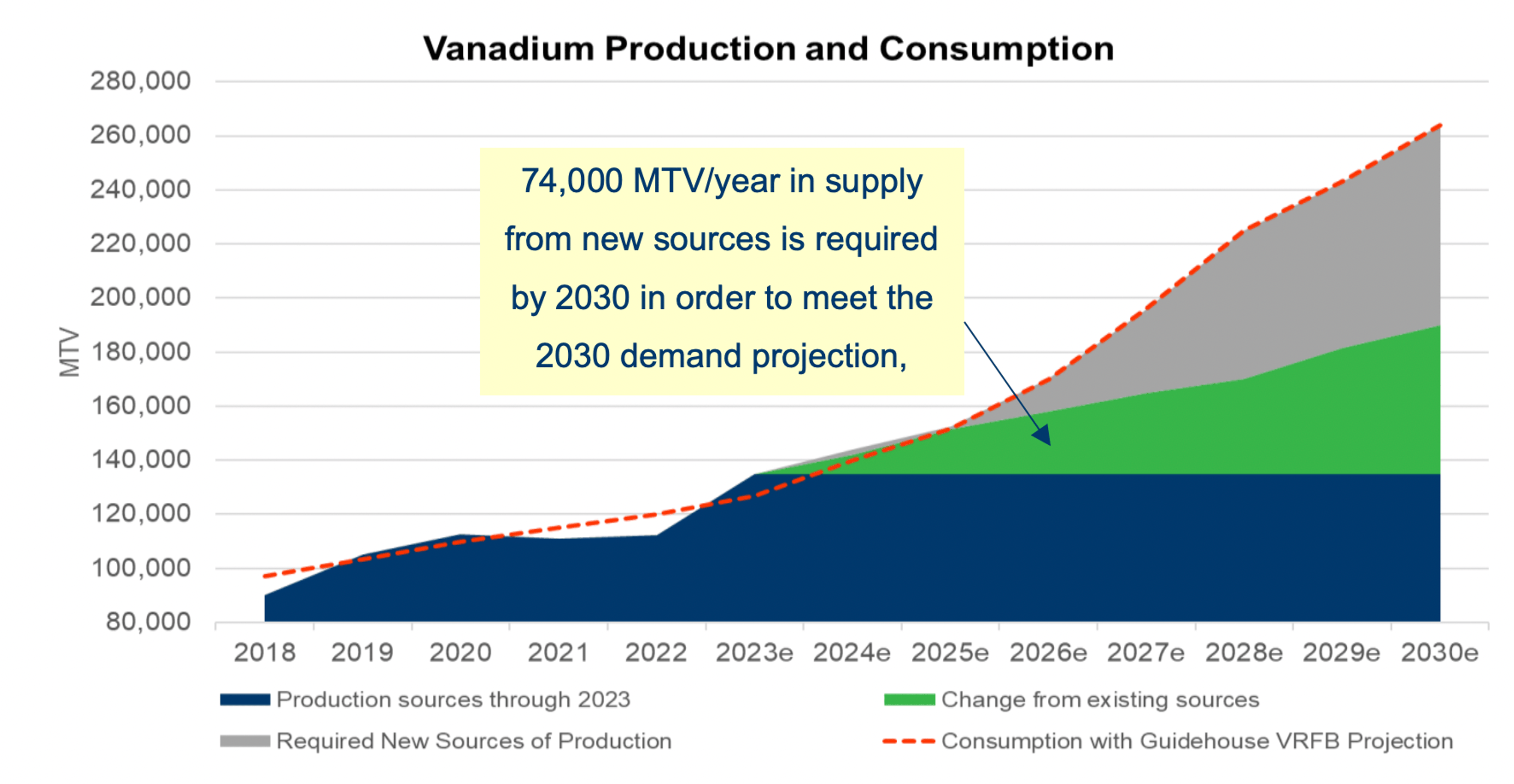

RICHMOND VANADIUM TECHNOLOGY (ASX:RVT)

(Up on no news)

A BFS is underway at RVT’s flagship 1.8Bt Richmond-Julia creek project, which hosts the world’s largest undeveloped vanadium resource of its type.

Last week it extended the timeframe for completion of the BFS by 6 months “following a detailed review of initial results from all work programs and the current vanadium market”.

It should be done by the June quarter 2025, it says, just in time for a battery driven surge in vanadium demand.

“Richmond Vanadium Technology is focused on contributing to the creation of a new industry for Australia, the development and global implementation of vanadium redox flow batteries,” RVT managing director Jon Price says.

“We need to ensure we have the technical, ESG and financial assessments capabilities, as well as the expected rise in vanadium price to take advantage of the forecast growth in demand for grid-scale energy storage in 2026 and beyond”.

RVT has a strong balance sheet and is fully funded up to an investment decision next year, Price says.

FUTURE BATTERY MINERALS (ASX:FBM)

The clay lithium hopeful is drilling into thick, high grades underneath known mineralisation at the flagship Nevada project.

Highlights include 66m at 1,001 ppm Li from 216m, and 23m @ 1,081 ppm Li from 182m.

Two of the three holes ended in mineralisation, it says. A maiden resource is due out in the current quarter.

“With drilling to date at Lone Mountain yet to intercept bedrock, there is now compelling evidence that the host Siebert Formation’s lithium mineralisation is thicker, more continuous and higher grade than previously indicated,” FBM technical director Robin Cox says.

“Our Phase 3 Mineral Resource drilling program has now concluded, with six RC holes completed through December and early January; those assays are pending.

“Final results from the Phase 3 drilling are set to inform the declaration of maiden Mineral Resource Estimate for the NLP during Q1 CY2024.”

Unlike hard rock spodumene or brines, clay lithium deposits have yet to be mined successfully. Lithium America’s advanced 19Mt Thacker Pass development, in the same neighbourhood as FBM, could be the first.

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.