Like nimble gazelles, ASX juniors are waltzing into Africa’s virgin territory for critical minerals

ASX juniors are herding themselves into Africa's largely untapped critical minerals jurisdictions. Via Getty Images.

Is everyone forgetting how cheap it is to mine critical minerals in Africa? Maybe? Or maybe not.

A quick scrape of the ASX will tell you there are quite a few early movers into the world’s Garden of Eden, proving up mineral wealth in vastly underexplored jurisdictions with little to no previous mining nous for rare, in-demand commodities.

Like nimble gazelles, intrepid ASX-listed mining juniors are leaping into near-virgin mining territory and attracting a helluva lot of attention from a bunch of OEMs, Sovereign Wealth Funds and governments both foreign and domestic.

The big cats are also jumping on board to help explorers cut red tape, provide funding and accelerate the development of minerals projects necessary for our jump into cleaner energy sources. Let’s take a look-see:

US-Saudi partnership to spend big in Africa

None are more publicly stating their plans to foray into Africa than the Saudis and US – announcing a partnership late last year to invest US$15 billion into the continent to secure critical minerals supply.

Saudi investment minister Khalid Al-Falih has publicly announced the nation would use its sovereign wealth fund to make “game-changing investments” into Africa.

Commenting on behalf of the Center for Strategic and International Studies (CSIS), Gracelin Baskaran says the partnership – for African countries in particular – is lucrative, as the land of the two holy mosques plan to be producing 500,000 EVs annually by 2030.

“Saudi Arabia has shown they are willing to deploy the capital at a time when many private sector players are scaling back on investment,” Baskaran said.

“It has also shown that is willing to provide African countries with the support to ensure they get more from their resources.

“By partnering, Saudi offers the US and its allies the most powerful counter to China’s dominance in critical minerals.

“The US has had very limited commercial engagement with the African continent, which has over 75% of the world’s manganese, platinum and chromium, nearly half the world’s cobalt, and a fifth of the world’s graphite.

“On the other hand, Saudi Arabia has become increasingly close to Africa.”

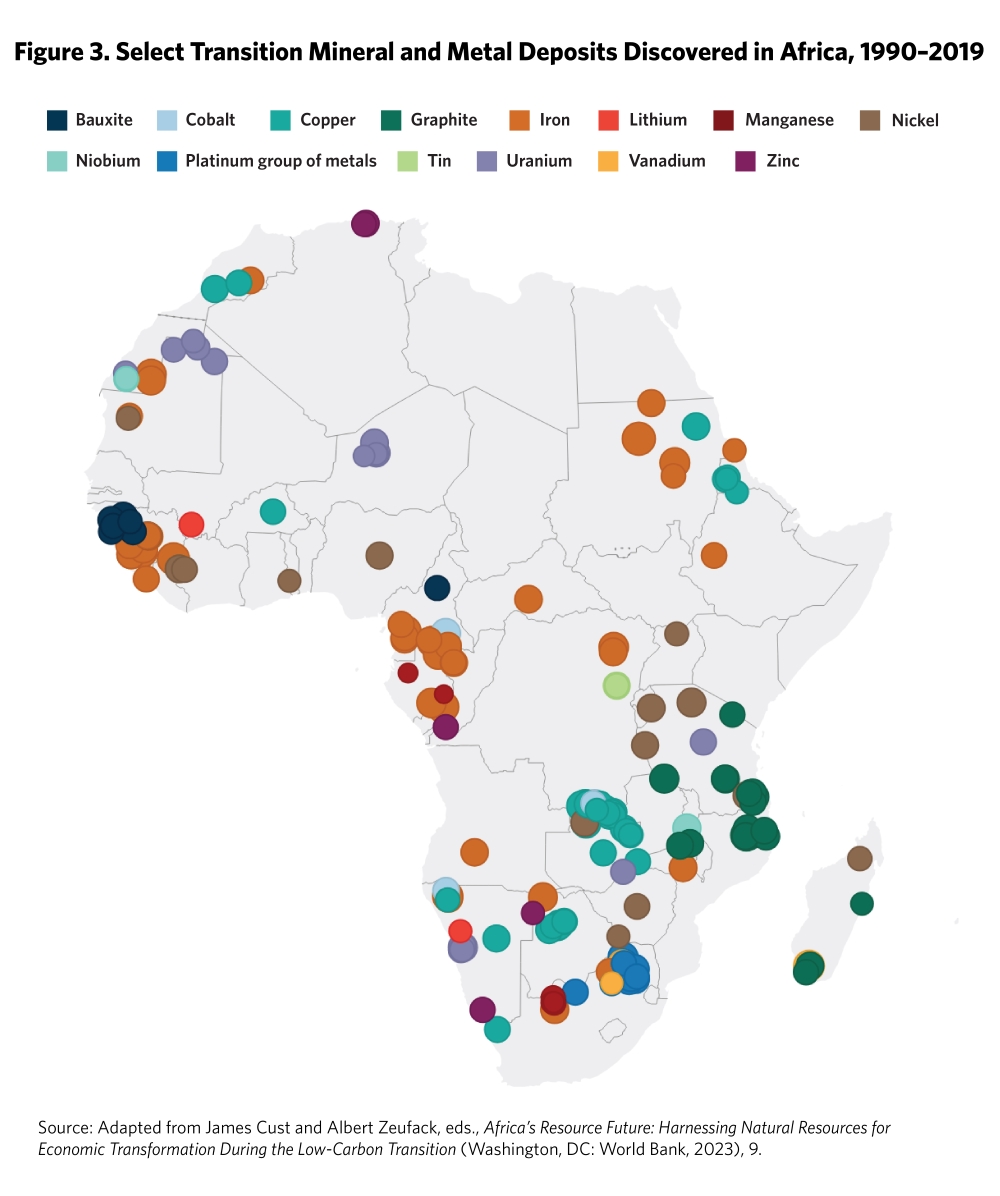

The Carnegie Institute says the African Union is well aware of its mineral endowment and countries such as Ghana, DRC, Namibia, Nigeria, Tanzania, Mali, Mozambique, Malawi and Zimbabwe, among others, all have such country-level strategies to leverage their deposits.

The graph below shows most, yet not all discoveries to-date, but it sure does give you an idea of what the continent holds.

Africa is primed for a critical minerals surge

Speaking with Stockhead, Matthew Johnson, partner at global resources specialist law firm Allen & Overy, says the opportunities for mining projects are greatly increasing on the continent.

“What we’re seeing is that companies will [carte blanche] go wherever the opportunities are,” Johnson says.

“Our sense of this is that they are willing to take on board perceived geopolitical risks over the potential time delays to get projects off the ground in other jurisdictions such as WA and Canada.

“Part of the attraction of places like Africa – and we’re even seeing it in South America – is the speed of being able to get projects permitted from start to finish much quicker.

“From what we see, they’re still undertaking all of the right environmental impact assessments in much the same way, but there’s also that willingness across the board to process these things quicker than it might be in other, more robust jurisdictions.”

Johnson also says that while new tech looks promising, they may take years – if not decades – to become mainstream, so it’s critical for companies and governments alike to meet their current, long lead project timelines and clean energy targets using commercially proven end products.

“We’re increasingly seeing OEMs coming in from electronics and automotive companies that are willing to get involved in trickier to operate jurisdictions due to the scarcity of supply and tight timetables for getting products to market,” he says.

“Government EV targets are definitely driving pressure for OEMs to secure supply chains and we don’t see that letting up any time soon.”

The ASX gazelles leaping to the occasion

Leo Lithium (ASX:LLL), meanwhile, has come out of the fog from the stalled development of its Goulamina lithium project in Mali where its backer, Chinese battery maker Ganfeng, has floated its progress – another example of an OEM willing to get projects into production at all costs.

Nearby is First Lithium’s (ASX:FL1) Blakala lithium prospect; which, according to CSA Global, is one of the only other Tier 1 critical minerals projects in the country.

FL1 is hard at it unlocking Blakala’s potential, with the latest hits from diamond drilling showing a whopping 111m @1.57% Li2O from 33m and up to 1.94% from wide spodumene targets west of the main target area.

Backed by Piedmont Lithium (ASX:PLL) (which will take a 50% stake in the project) Atlantic Lithium (ASX:A11) aims to become Ghana’s first lithium producer as it advances its 35.3Mt @ 1.25% 350,000tpa Li2O Ewoyaa project.

Staying in West Africa, Mako Gold (ASX:MKG) just completed a program of detailed geological mapping and rock chip sampling that has turned up several multi-kilometre manganese-rich zones at its Korhogo project in Côte d’Ivoire.

According to its MD Peter Ledwidge, the results achieved from this low-cost mapping and rock chip sampling program add to the potentially significant discovery already made on the company’s Ouangolodougou permit at Korhogo.

On to rare earths (REEs) and Ionic Rare Earths (ASX:IXR) is looking to be Uganda’s – and Africa’s – first ionic adsorption, clay-hosted (IAC) REE project to get off the ground.

The explorer owns 60% of the Makuutu project which has a current (and massive) resource of 532Mt @ 640 parts per million (ppm) total rare earths oxide (TREO) containing 71% magnet and heavy rare earth carbonate (MREC) which contain high value neodymium and praseodymium (NdPr). It’s also currently proving up extensions to the known mineralisation.

Just last month the company received a Large Scale Mining License for Makuutu, a reflection of strong support from the Ugandan government and the first ever such licence under its Mining Act of 2022.

Tanzania is not well known for REEs, yet Peak Resources (ASX:PEK) is pursuing the high-grade Ngualla project, where recent trench samples confirmed widespread high-grade fluorspar mineralisation across a ~3.7km Breccia zone, which is known to contain high-value percentages of NdPr oxides.

And, as graphite stocks are on the move due to Chinese supply fears, Evolution Energy (ASX:EV1) is progressing its Chilalo graphite project also in Tanzania and it couldn’t be better timing.

Then there’s Rio Tinto (ASX:RIO) backed Sovereign Metals (ASX:SVM), which is basically nailed on to get into production of its world-scale Kasiya rutile/graphite project in Malawi.

With support not only from one of the world’s largest miners, it also has the backing of the Malawian government.

Outside Harare in Zimbabwe, Prospect Resources (ASX:PSC) has discovered high-grade spodumene within its Step Aside lithium project after assays returned up to 1.49% Li2O at the WinBin prospect.

It’s no stranger to success in the country – PSC had great success with its 72.7Mt Arcadia project, subsequently selling it to China’s Huayou Cobalt in mid2022 for ~US$422m cash – and the explorer reckons Step Aside could be within the same mineralised system.

Uranium is a critic… hang on, what?

Yep, pretty much anyway. To power our clean energy transition the world is going to need a lot more consistent energy for the grid.

That’s why the price of yellowcake has shot through the roof in the last year, surging to almost two-decade highs >$US100/lb to feed the rising amount of nuclear reactors coming online.

READ MORE: Clean, reliable baseload power: Here’s why nuclear energy is a no brainer

Looking to repeat the success of Namibia’s robust uranium production industry, ASX juniors like Aura Energy (ASX:AEE) are branching out to countries such as Mauritania, where it believes its Tiris project can grow to represent a globally significant uranium province as it targets a 100Mlbs U3O8 resource.

Economically significant calcrete-type uranium deposits had not been reported in Mauritania prior to Aura’s discoveries, spurring the government to grant the company a 30-year security for exploration and development of the project.

In Senegal, Haranga Resources (ASX:HAR) is using termites – yes termites – as an exploration technique at its Saraya project to identify several anomalies outside the current contained inferred resource of 16.1Mlb @ 587ppm U3O8.

Termite mound sampling followed by auger drilling has proven to be a cost-effective method of exploration for decades – you just need to have lots of termite mounds at the surface of the deposit.

At Stockhead, we tell it like it is. While Ionic Rare Earths, Haranga Resources, Mako Gold, Prospect Resources, Aura Energy and First Lithium are Stockhead advertisers, they did not

sponsor this article.

Related Topics

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.