Carmakers, battery manufacturers are calling nickel companies direct as supply shortfall looms

Pic: Bloomberg Creative / Bloomberg Creative Photos via Getty Images

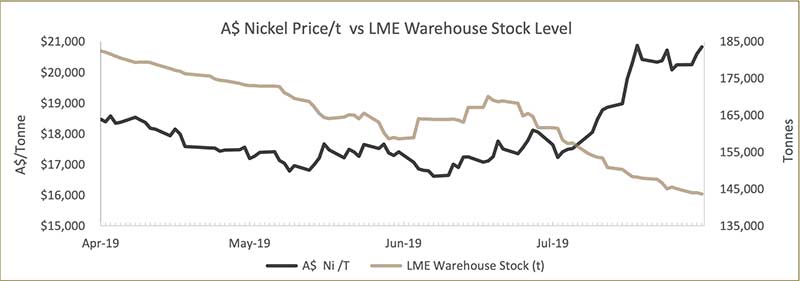

It’s great to be a nickel company, for the first time in a very long time.

The traditionally volatile metal has brushed off fears of a global recession to rate as one of the year’s top performers.

The recent surge to $US16,690/t — triggered by speculation over Indonesia’s on-again, off-again nickel export policy — isn’t necessarily tied to market fundamentals.

Still, those fundamentals look good.

An extended period of low prices means that new mines are not being developed and so global stockpiles are dwindling.

All while stainless-steel markets – accounting for ~70 per cent of today’s consumption – are growing and long-term demand estimates from the battery sector become more real by the day.

You can see why experienced forecasters like Wood Mackenzie are predicting a pretty substantial supply crunch in the mid-2020s.

“Although the battery sector share of nickel demand is much smaller than other metals, getting the quantity of nickel that EVs will need [called tier 1 nickel] by the mid-2020s will be a challenge,” Gavin Montgomery, Wood Mackenzie research director said in late July.

“A low nickel price has hindered any project development and with lead times often up to 10 years, investment needs to happen now.”

Major EV manufacturer Tesla is one that has voiced concerns that underinvestment by the mining sector could lead to global shortages of battery metals, like nickel.

Vivas Kumar, principal consultant at Benchmark Mineral Intelligence was former head of battery supply chain management at Tesla.

“Two or three years ago, carmakers generally left the responsibility to source battery raw materials to their cell suppliers,” Kumar told Stockhead.

“Now, because of impending shortages and a continuous push towards lowering $/kWh cost of battery cells, automakers are becoming more educated about battery metals procurement.

“As a result, we have seen that automakers are now staffing up their own battery metals procurement teams and are signing direct contracts with mining and chemical supply chain players.”

He also says it is important to differentiate between class 1 and class 2 nickel supply. Class 1 (low impurity) nickel is ideal for batteries; class 2 is not.

More steel-based demand is shifting into class 2, Kumar says, and the market trends for battery versus steel will start to diverge as a result.

Class 1-focussed nickel producers are already responding to the projected demand.

Nickel West, formerly the punching bag of BHP’s global portfolio, is now revitalised by the EV thematic.

Last year, it announced that 90 per cent of projected nickel sulphide production will be sold into the battery sector.

In early August, it formalised a nickel sulphide deal with near term producer Mincor Resources (ASX:MCR) to shore up future ore supply for its Nickel West operations.

“With hundreds of billions of dollars earmarked for investment in the battery industry over the next decade, I believe Mincor’s timing could not be better as we head into a development phase, given the dynamic shift in forecasted nickel consumption over the coming years,” Mincor managing director David Southam says.

The $3.2bn market cap Independence Group (ASX:IGO) – owner of the Nova nickel mine – is currently progressing nickel sulphate downstream processing studies.

Even advanced explorers like Blackstone Minerals (ASX:BSX) and Pure Minerals (ASX:PM1) are investigating the development of downstream processing to produce a nickel and cobalt product for burgeoning battery markets.

Carmakers, battery manufacturers knocking on the door

Still, these developments wont be enough to satiate impending demand, and the battery supply chain knows it.

At this year’s Diggers & Dealers forum producer Western Areas (ASX:WSA) said it was getting a ”significant increase in inbound off-take enquiries for nickel sulphide concentrate post current contract period, primarily linked to the EV battery sector”.

Even junior explorer St George Mining (ASX:SGQ) is receiving inbound enquiries – and they haven’t even delineated a resource yet.

“We have also had battery manufacturers come to us direct asking ‘can we made an investment in St George; we want to secure long-term supply’,” says St George exec chairman John Prineas told Stockhead.

“They can obviously see a supply crunch coming.

“Experienced predictors like Wood Mackenzie have a long-term price target of $US21,000/t. I’ve got no doubt that will be revised upwards as we go along.”

READ: St George Mining’s John Prineas on why BHP has no chance of getting its ‘freakish’ nickel belt back

Queensland nickel laterite play Australian Mines (ASX:AUZ) has just signed its nickel-cobalt offtake agreement with battery maker SK Innovation.

This offtake is an important step towards locking in Sconi project finance.

The SK deal covers 100 per cent of production but this hasn’t stopped other inbound enquiries, managing director Benjamin Bell says.

“Yes, I certainly noticed that I’m being contracted a lot more from battery manufacturers and car companies directly,” Bell told Stockhead.

But it’s not necessarily desperation, he says. These companies are just trying to get ahead of future shortfalls.

“I think they are looking at that period between 2021-2025 when there’s a predicted deficit in both nickel and cobalt,” Bell says.

“In the case of SK, it took us 12 months to go from a term sheet to an offtake.

“And that’s because for these sorts of companies, it’s the first time working with a mining company which means there’s a lot more ‘hand holding’ required.

“A lot of these [battery makers/ car manufacturers] will be talking to nickel explorers with the thinking that ‘I don’t need you immediately, but I might need you in 2-3 years’ time — so let’s form a relationship now’”.

- Subscribe to our daily newsletter

- Join our small cap Facebook group

- Follow us on Facebook or Twitter

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.