Lithium stocks guide: Here’s everything you need to know

Pic: Getty

Lithium – that silvery, white metal – captures the zeitgeist of the new battery age.

This is, because unlike other elements, lithium cannot be replaced as part of the next generation of lithium-ion batteries for electric vehicles and stationary storage.

Spearheaded by this electric vehicle (or EV) thematic, lithium prices have tripled since 2010.

But these higher prices naturally incentivised an aggressive supply response.

Production in Australia and overseas has boomed, increasing from around 149,000 tonnes in 2012 to 211,000 tonnes in 2017.

This is expected to reach almost 1.3 million tonnes by 2027, driven by rising demand for EVs.

But this production growth also stoked fears that the market was going to be flooded with an oversupply of lithium, and battery metals stocks in 2018 suffered as a result.

In this guide we’ll explain the factors that have been driving ASX lithium stocks and what could drive demand – and stock prices — into the future.

What is lithium?

Highly reactive and flammable, lithium is the lightest metal, and so soft it can be cut with a knife.

It has a very low density (similar to pine wood) which means it is one of only three metals that can float on water.

Lithium is actually pretty abundant, and due to its solubility, an estimated 230 billion tonnes of lithium is found in ocean water.

Lithium batteries: A short history

Due to its superior electrode potential, lithium has been an important component of battery electrolytes and electrodes since the late 20th century.

People began experimenting with lithium batteries way back in 1912, but it wasn’t until the 1980s that the first lithium-ion prototype was made – a rechargeable, more stable version of previous iterations.

First commercialised in 1991 with little fanfare, the market for these lithium rechargeable batteries quickly grew into a $3 billion industry by 1998.

At that time, the value of the lithium sold for battery production was estimated to be $US111 million.

In 2007, driven by the heavy-duty power tool market, batteries became the major market for lithium for the first-time, accounting for 25 per cent of all production.

In 2009, global sales of these rechargeable batteries were estimated at $US7.7 billion.

That grew to $US11.7 billion by 2012, when consumer applications including cameras, smartphones, computer tablets, and laptops accounted for 64 percent of global lithium-ion battery market revenues.

In 2017, the lithium-ion battery market was worth $US25 billion, with consumer electronics still the largest segment.

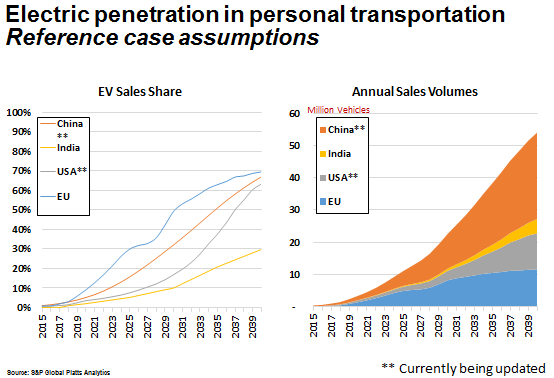

The next demand ‘driver’ (pun intended) will be the rapidly growing EV market.

Exponential EV sales growth – from 2 million vehicles in 2017 to an estimated 50 million per year by 2030 — is expected to create huge demand for battery-grade lithium.

A shift to higher energy density batteries could also increase lithium demand.

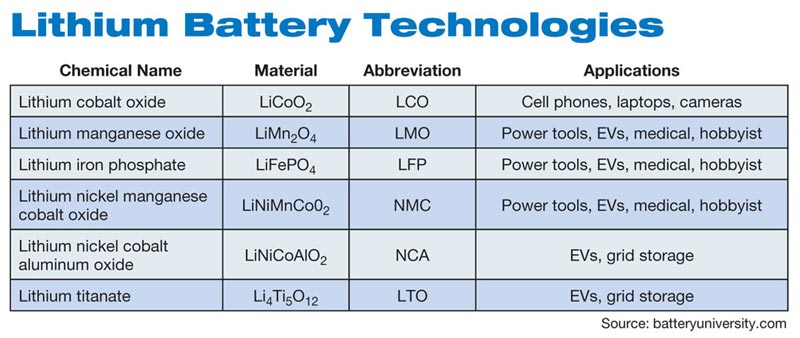

Traditional lithium iron phosphate batteries are about 7 per cent lithium, but the “almost overnight shift” in preference towards nickel-manganese-cobalt (NMC) and nickel-cobalt-aluminium (NCA) batteries increased the requirement of lithium by up to 50 per cent.

Mining lithium: Hard Rock v Brine

Lithium is mined from two main sources — hard rock (hosted in spodumene ore) and brine (lithium-enriched salt water).

Spodumene is the main lithium bearing mineral mined from most hard rock lithium mines around the world.

The typical grades of a hard rock lithium mine range between 0.9 and 1.6 per cent, while lithium concentrations from brines is between 0.07 and 0.16 per cent.

Mined material is processed into lithium carbonate or lithium hydroxide, which can be sold to make cathode material for lithium-ion batteries.

(Batteries include an anode (positive) and a cathode (negative) and the electrical current flows between the two.)

The cathode is then shipped to a battery maker, who sells the final battery product to car makers, stationary storage manufacturers, and other electronics manufacturers.

Found mostly in Chile, Argentina, and Bolivia, brine deposits – which produce a lithium carbonate — occur when underground lakes, geothermal waters or petroleum brines are enriched with lithium.

The lithium-rich salty water is pumped to the surface into evaporation ponds, before the concentrated solution is processed into carbonate.

Lithium from hard rock deposits, like those found in Australia, can be more expensive to extract initially but have an important advantage in EV markets.

That’s because the lithium-bearing spodumene ore can be transformed into lithium hydroxide – which commands a higher price than carbonate — after a relatively simple process and can produce cathode material more efficiently.

This gives Australia — now the world’s largest lithium producer — a cost advantage of 10 to 15 per cent compared to the largest South American brine producers, according to the Australian Department of Innovation, Industry and Science, especially if you consider that lithium hydroxide could account for about 25 per cent of all lithium compounds used in batteries by 2021.

As EVs increasingly dominate the market, this share is could rise to almost 60 per cent over the next decade.

Two of the world biggest producers, Albemarle and SQM, are already stepping up investments in Australian hard rock mines because of “a significant acceleration in demand for lithium hydroxide” from battery makers.

How much does lithium cost?

That short answer is it’s complicated.

Most lithium — processed or not — is currently traded in very private long-term contracts between major producers (the miners) and consumers (the anode or battery makers).

The prices that punters usually see are based on Chinese spot or market prices, which represent only a small portion of total lithium purchases.

“Lithium prices have shown a mixture of trends in 2018, depending on which price set you look at,” said David Merriman, lithium supply specialist at Roskill.

“While Chinese ‘spot’ or ‘internal’ prices for lithium carbonate have fallen back dramatically, they represent only a small portion of total lithium carbonate purchases.”

So basically, prices did fall in 2018 but is wasn’t as dramatic as many believe.

For example, long term contract prices for spodumene in China – where Australia sells most of its ore – went for between $700 and $900 per tonne in 2018.

At these prices Australian miners still made very healthy margins.

And then there’s the price for refined lithium hydroxide, which sold for around $17,000 per tonne – a huge mark-up in comparison.

This has driven a huge wave of investment in value-added processing facilities in Western Australia, designed to refine huge amounts of spodumene ore into hydroxide.

Miners including Albemarle, SQM, Mineral Resources (ASX:MIN), Talison Lithium (ASX:TLH), Kidman Resources (ASX:KDR), and Neometals (ASX:NMT) are currently planning or constructing at least five large beneficiating plants worth a collective $3 billion in Western Australia alone.

Is the lithium boom over?

Not even close. It’s only just starting.

Canaccord Genuity mining analyst Reg Spencer says lithium stocks took a beating in 2018 because investors concerned about oversupply didn’t understand the “depth and complexity” of the lithium supply chain.

The supply chain from “mine or brine to market” could take up to a year — and that was before delays and other potential bottlenecks in processing, he said.

“A lot of analyst work that I see models lithium demand in terms of how many EVs are sold in any particular year.

“But when you factor in this 9-to-12 month supply chain lag, the lithium that’s going into the EVs that are getting sold today was actually produced and mined last year.”

Bloomberg estimates the world’s lithium battery-making capacity will more than triple from 175 gigawatt hours to 630GwH by 2022.

Battery metals data leader Benchmark Minerals Intelligence had similar forecasts.

It says there were 42 battery mega factories built or in the pipeline by August this year – up from three in 2015.

In September that number had already increased to 45, and by November 2018 that number was over 50.

By 2028 these mega battery factories — such as the gigafactories being built by Elon Musk’s Tesla — would need 840,000 tonnes per year of lithium.

But these projections are constantly being revised upwards, as the rapid pace of development amazes even the most bullish of analysts.

EVs are in the driver’s seat

“We need to remember there are not many electric vehicles out there yet,” S&P Global Platts analyst Marcel Goldenberg says.

“Electric vehicles are the driver. That’s where the disruption is coming from, and that’s where you will see raw material demand coming from.”

In September 2018, the number of electric vehicles sold throughout the world passed 4 million — and sales are increasing at an exponential rate, say researchers at Bloomberg New Energy Finance.

This is a drop in the bucket compared to recent worldwide car sales of about 88 million cars and light vehicles.

But that could soon change. 2019 marks the start of an expected EV ramp-up for the world’s biggest carmakers.

For example, Volkswagen Group — which owns Audi, Bentley, Bugatti, Lamborghini, Porsche, SEAT, Škoda and Volkswagen — says it plans to spend more than $68.5 billion in the coming five years on EVs, autonomous driving, new mobility services and digitalisation.

Volkswagen sees an EV future as inevitable and wants to “speed up the pace of innovation” from a position of strength and wants to produce one million electric cars per year globally from 2025.

To accomplish this, Volkswagen reckons it needs battery capacity in excess of 150GWh per year through to 2025 just to equip its own electric fleet.

That’s equal to the annual battery cell capacity of more than four Tesla Gigafactories.

…But stationary storage will also play a key role

Stationary storage systems are big batteries often designed to store excess power from the power grid, including from renewable sources, for use during expensive peak demand periods.

It also includes residential and industrial ‘behind the meter’ systems.

By 2028, Benchmark Minerals Intelligence predicts 50 per cent of the burgeoning stationary storage market will be lithium-ion.

But once again, analysts and industry insiders are constantly revising their stationary storage projections upwards as the industry accelerates.

Bloomberg New Energy Finance (BNEF), for example, has significantly increased its forecast for global deployment of behind-the-meter and grid-scale batteries over coming decades.

In 2016, BNEF expected 25GW of installed storage by 2028, and for the market to be worth $US250 billion by 2040.

Last year, it predicted 125GW of batteries would be sold for global energy storage by 2030.

In November 2018 it revised those figures again. Now, global installed battery storage capacity could reach 100GW as early as 2025, with 300GW breached around 2030.

By 2040, BNEF reckons the global energy storage market will grow to a cumulative 942GW, worth about $US620 billion in investment.

(Incredibly, batteries for stationary storage will make up just 7 per cent of total demand by 2040, with EVs taking dominant market share.)

Investing in ASX lithium stocks

On the production side of the equation, you can (almost) count the number of ASX-listed lithium producers on one hand – at the moment, they include Pilbara Minerals (ASX:PLS), Altura Mining (ASX:AJM), Galaxy Resources (ASX:GAL), Orocobre (ASX:ORE), Alliance (ASX:A40) and Mineral Resources (ASX:MIN).

But at the junior end of the market there’s a lot more choice for investors than there used to be.

Explorer AVZ Minerals’s (ASX:AVZ) Manono project is one of the few lithium projects globally that have low levels of impurities of mica and iron oxide.

This enables AVZ to meet the standards required of the next generation of lithium batteries, as requirements become more stringent.

Lithium battery manufacturers are demanding higher purity levels, as impurities can result in poor battery performance or battery failure.

In August this year the Manono project was confirmed as the largest hard rock lithium project in the world, and the second-highest grade.

A scoping study in October 2018 concluded that the project was the world’s largest undeveloped lithium project according to grade, mine life and expandability.

These factors give AVZ Minerals an edge amidst the growing global demand for high-quality lithium.

Near term producer Kidman Resources (ASX:KDR) wants to start construction of its Mt Holland project, a joint venture with the world’s largest lithium miner SQM, in the second half of 2019.

Ioneer (ASX:INR) is developing one of only two major lithium-boron deposits in the world.

(Boron is a versatile element used in everything from computer screens, fertilisers, and powerful magnets for wind turbines)

The company believes the Rhyolite Ridge project in the US can be the lowest cost lithium operation in the world at under $2000 per tonne of lithium carbonate.

Meanwhile, innovative companies like Lepidico (ASX:LPD) and Lithium Australia (ASX:LIT) are using their own technologies to produce lithium carbonate from non-conventional sources, including tailings — the materials left over after processing ore to separate valuable material from uneconomic material.

Lepidico plans to build a $3 million Perth-based pilot plant — or demonstration facility – to show off its technology to potential sales and finance partners ahead of development of its larger phase one processing plant.

The company is targeting commercial production for 2020.

Lithium Australia plans to be the first Australian company to do everything from mining lithium to making batteries.

Stage 1 of Lithium Australia’s Sileach pilot plant trial produced “outstanding results” in 2018 as the company aims to convert mine waste into lithium-ion batteries – a world first.

At Stockhead, we tell it like it is. While AVZ Minerals is a Stockhead advertiser, it did not sponsor this article.

This advice has been prepared without taking into account your objectives, financial situation or needs. You should, therefore, consider the appropriateness of the advice, in light of your own objectives, financial situation or needs, before acting on the advice. If this advice relates to the acquisition, or possible acquisition, of a particular financial product, the recipient should obtain a disclosure document, a Product Disclosure Statement or an offer document (PDS) relating to the product and consider the PDS before making any decision about whether to acquire the product.

Related Topics

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.