Closing Bell: Interest rates the only thing steady about local markets on Tuesday

Via Getty

- ASX in retreat as RBA holds at 4.35pc

- IT Sector falls 1.8pc

- Small cap winners led by Janison and Mako Gold

At its rejigged board meeting today, the Reserve Bank of Australia chose not to rejig interest rates – keeping the cash rate steady at 4.35%.

Local markets were already in the red and traders seem to have enough of their own problems to act surprised about it.

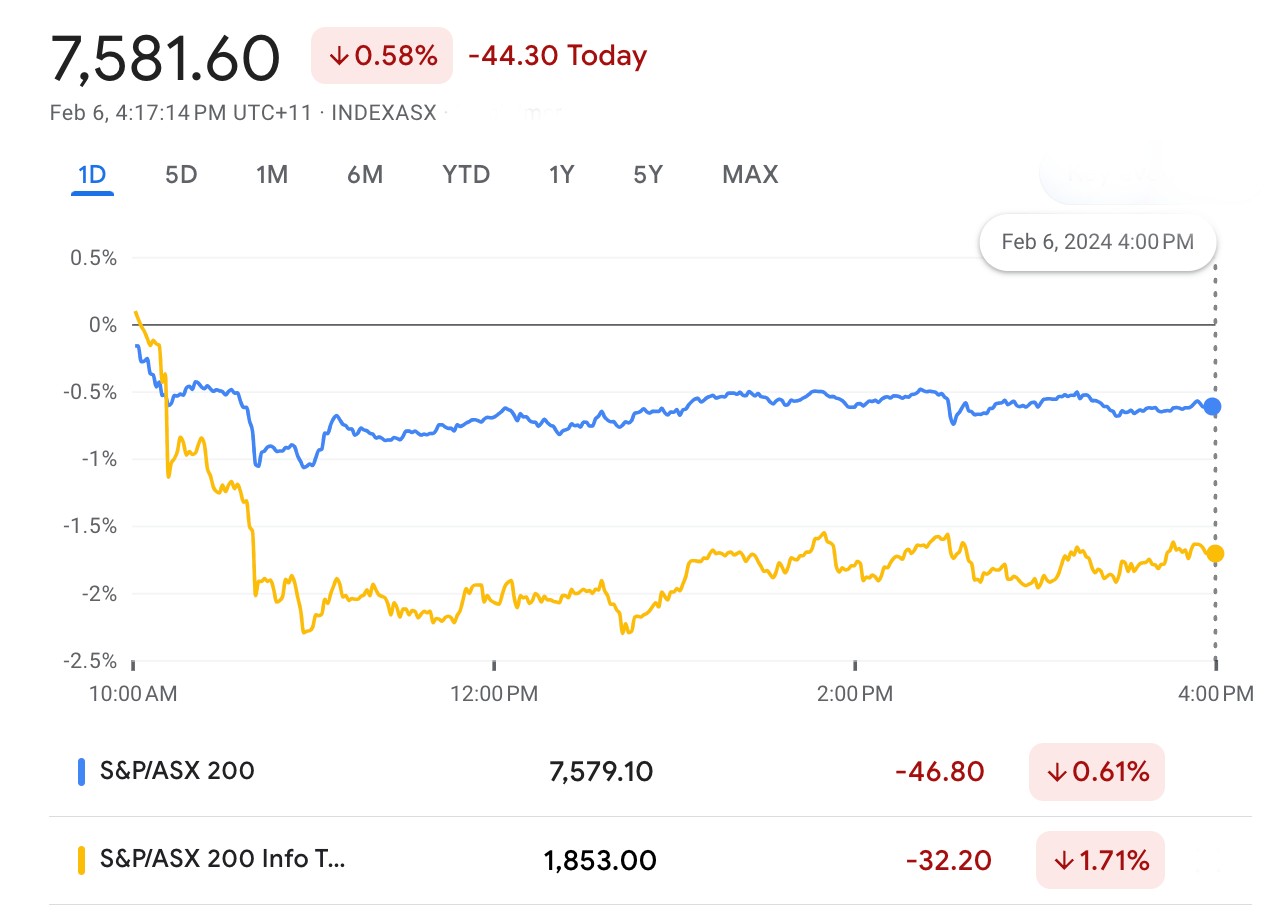

At 4.15pm on February 6, the S&P/ASX200 was down 44 points or 0.58% to 7,581.6.

We’ve been tracking losses in New York overnight as the greenback and US Treasuries picked up in the wake of an unwelcome 60 Minutes appearance by Fed Chair J. Powell who took 60 seconds to further extinguish hopes of incoming interest rate cuts.

The RBA’s been holding court all day, although the ABS briefly turned heads in the AM when it revealed the fastest decline in retail trade since August 2020.

The Bureau of Stats says retail sales in Australia fell by 2.7% month-over-month in December 2023, (unrevised) after a Black Friday-inspired 1.6% growth in November.

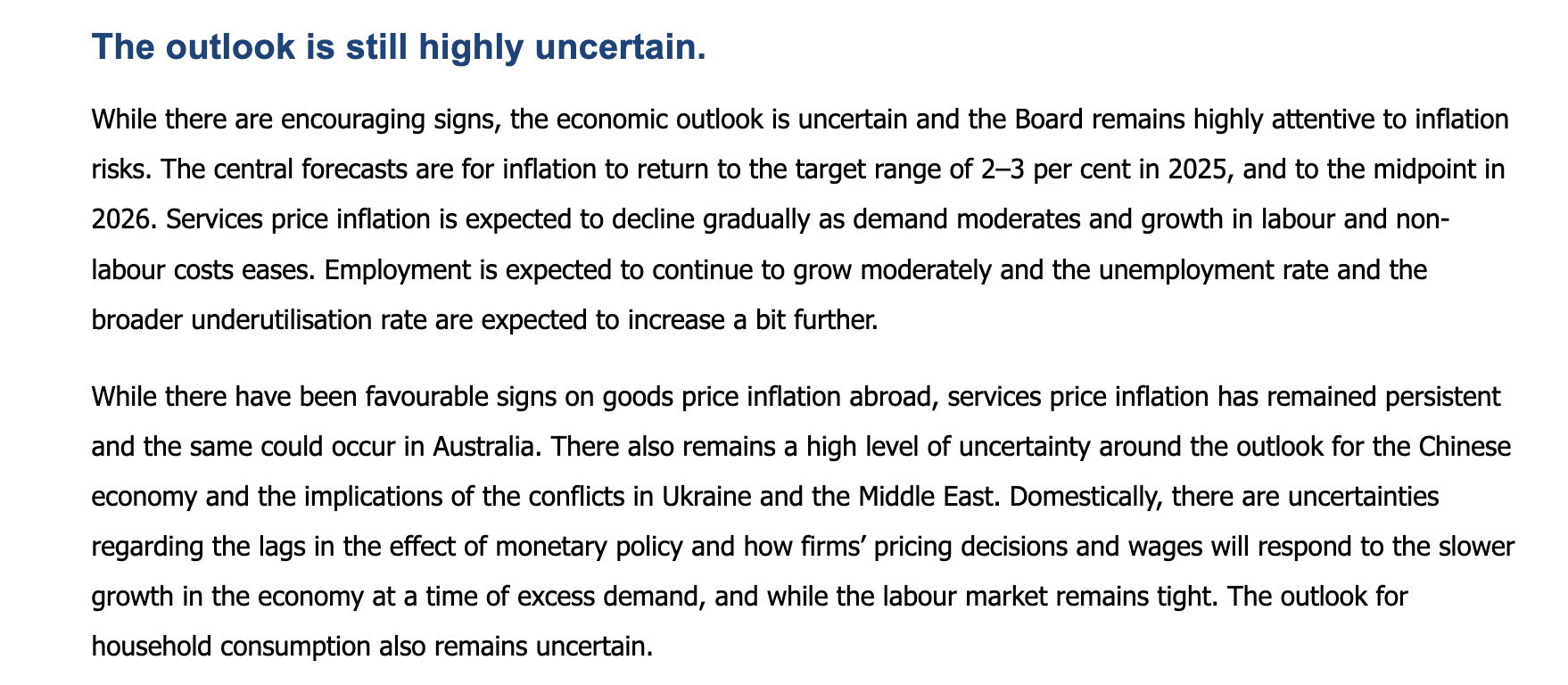

Meanwhile, the local central bank has also downwardly revised its inflation forecast for the end of the year from 3.5% to 3.2%.

Inflation is now pegged by the RBA to get back to the target range in H2 2025 and to be around the midpoint by mid 2026.

The pause from Martin Place was widely expected with almost everyone betting on the bank to hold the line on interest rates, as CBA’s top economist Gareth Aird noted.

“The Board has retained a tightening bias as we anticipated, though the language has shifted a little: “a further increase in interest rates cannot be ruled out”

“Maintaining a tightening bias signals to the fiscal authorities that it’s too early to declare the inflation fight over. The RBA would not wish to see fiscal settings loosened until further progress on inflation has been made towards the target band,” Gareth added.

According to Dr Dwyfor Evans, head of APAC macro at State Street Global Markets, the RBA but did agree with CBA that given current inflation relative to target, further tightening remains an option.

“That said, projections allude to a gradual easing cycle ahead and both growth and inflation forecasts were revised lower.

“A slightly more hawkish set of comments than anticipated, particularly after the weakness in recent inflation data, but clear sensitivity at the RBA towards inflation threats and some optionality on future policy.”

Dr Evans says that after recent CPI reports it certainly wasn’t “the neutral to dovish report that some would have anticipated.”

“We focus on weaker consumption, elevated debt servicing costs and signs of easing in the job market as pointers towards a more accommodative stance going forward, albeit one that the RBA did not necessarily deliver in its messaging today.”

Everyone but for Energy and Consumer Staples were deeply in the rouge at around lunchtime, and the various macro hand-me-downs have failed to move the dial much at all.

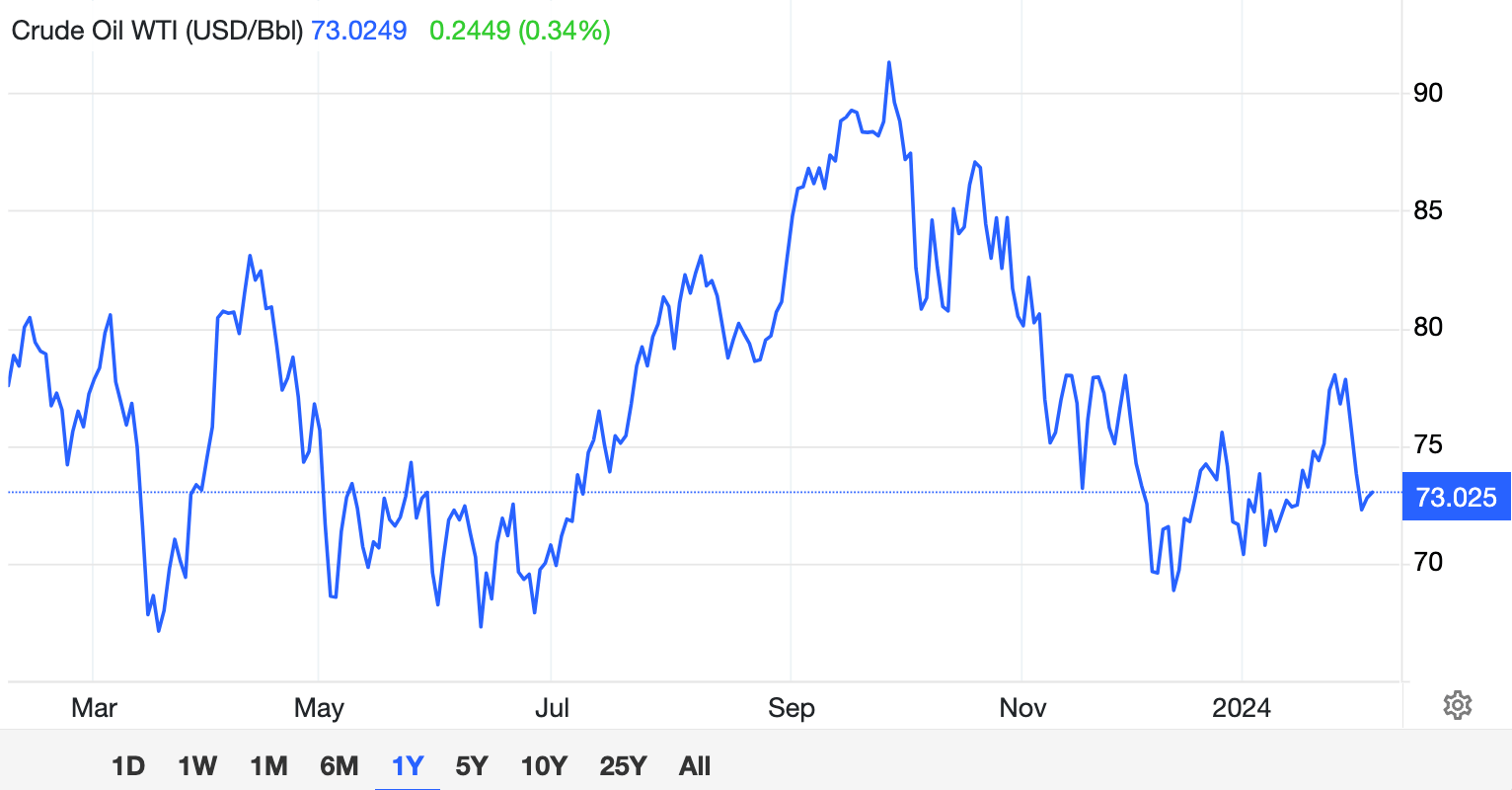

Oil futures (WTI) which have taken a right beating lately, solidified a bit during the session at a little over US$73 per barrel.

That meant the local energy majors enjoyed some respite, with the sector climbing off the matt it’d been pinned to since oil prices plunged more than 7% over the last seven days, thanks to these accursed ceasefire negotiations between Israel and Hamas.

That kind of loose talk can significantly reduce supply risks in the Middle East and take the pressure off oil prices.

Of course, there is no ceasefire. And instead now the US and its allies (that’s us) are merely at the early days of a ‘proportionate response’ to the three soldiers killed by a reported Houthi drone strike last week.

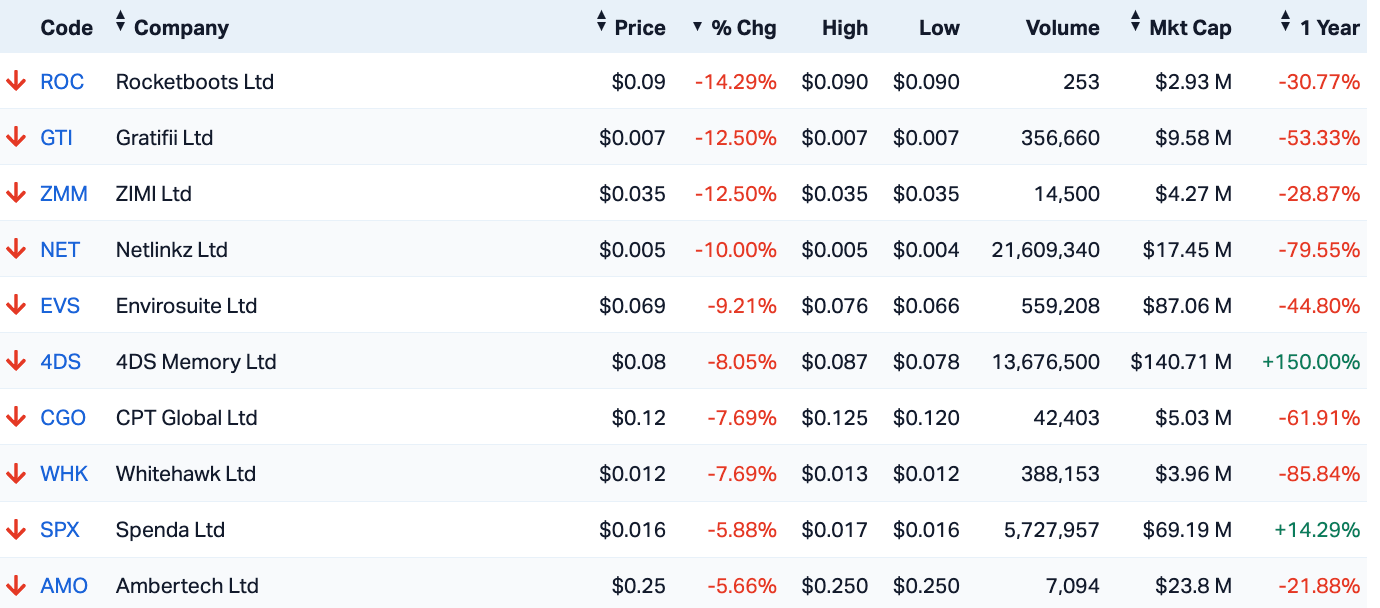

Back on the local bourse, it was the IT Sector’s turn to out-disappoint…

ASX Tech Sector Laggards on Tuesday

The minnows may’ve copped the sell-offs, but the local versions of the mega-tech were behind the sector losses – both Xero (ASX:XRO) and WiseTech Global (ASX:WTC) were between 3% and 4% lower.

The iron ore trio copped a second day of bleeding as the price of iron ore slid again, China-facing Fortescue had the worst of it, down 3%.

But the saddest of the diggers on Tuesday – down around 15% – is the turbulent goldie West African Resources (ASX:WAF) which has slashed production guidance at its Burkina Faso goldmine.

Kicking it with small caps is obscure Aussie retailer Myer (ASX:MYR) , which collected about 14% eight-month high of 75.5c after the department store reported the slightest of improvements in 1H same-store sales. Like about 0.1% better vs the same time a year ago.

Finally Cochlear (ASX:COH) shares have been in the firing line after UBS downgraded the stock after speaking directly with the world’s top CMV specialists, who reckon there’s a good chance Moderna will have some success with its phase III trials for a vaccine.

The idea that a CMV vaccine could have an impact to Cochlear’s top line isn’t new, but so far none have materialised.

UBS now think 5-6% of Cochlear’s total sales are at risk over the long-term and have cut their forecasts by low single digits from FY26.

This drops their forecast mid-term (FY24-28) revenue growth from 7.4% p.a. to 6.5% p.a.

And both the XSO Small Ordinaries and the XEC Emerging Markets Indices were slightly lower, although you’d be forgiven for hoping the XEC was handed a pity gain by the market gods, which have seen fit to strip it of circa 15% already this year.

ASX Sectors on Tuesday

![]()

And regional markets…

China’s tech heavy Shenzhen Component was surging by around 3% and stocks on the Hang Seng were ahead 2% at lunchtime in Hong Kong buoyed by the implementation of stimulus measures announced last month by Beijing, as China’s sovereign wealth fund, (Central Huijin) has “vowed” to go on an ETF buying spree to help prop up broader sectors.

Something scary out of Bloomberg this arvo, as a major Chinese macro hedge fund has revealed to clients that it cut and ran on bottoming out stock positions last month to stave off a collapse amid the escalating sell-off across Chinese equity markets.

Shanghai Banxia Investment Management “significantly reduced” its equity assets in the middle of January to cut losses, only keeping exposure to safer high-dividend stocks and bigger companies in the CSI 300 Index.

According to a Sunday night letter to investors, Shanghai Banxia Investment Management made a decent attempt at full disclosure for some bad bets:

“Banxia recognised its mistakes two weeks into the year, realising it “must lose an arm for survival,” the firm, led by founder Li Bei, said in the Feb. 4 letter seen by Bloomberg, using a Chinese proverb. That allowed it to “luckily dodge the more fierce declines of the most recent week.”

However, stock markets on the mainland remain close to five year year lows despite the efforts of China’s sovereign fund, Central Huijin Investment Ltd., vowed to buy more ETFs to support the market

Local investors will be waiting on domestic inflation numbers later this week to gauge the state of the world’s second-largest economy.

In Tokyo, equity markets were about 0.5% lower at lunch Tuesday, tracking losses on Wall Street.

Meanwhile, in the States…

We have a choker.

The S&P500 ended 0.3% lower overnight. Seemingly unable to surmount the”psychological” 5000 mark.

The Nasdaq dropped 0.2%, while the Dow Jones gave away 0.7%

US corporate earnings are at the midway mark, beats have exceeded expectations. But that also means any miss usually cops the full brunt of the naughty stick about the head and body.

Of the US market-driving Magnificent Seven, only Nvidia remains fully clothed. And for the rest, only Elon’s Tesla missed, and that’s cost it.

Overnight, TSLA crashed -3.7% to a nine-month low, after the company and its loopy genius of a chief executive endured a very rough few days.

For starters, the company has been forced to recall more than 2 million cars in the US because apparently some of the warning lights on the dashboard are “too small”.

Meanwhile, Elon’s been the subject of reports out of the Wall Street Journal that he’s freaking out numerous executives over his alleged drug-taking.

US Futures were lower in Sydney at 3.30pm on Tuesday.

ASX SMALL CAP LEADERS

Today’s best performing small cap stocks:

Swipe or scroll to reveal full table. Click headings to sort:

| Code | Company | Price | % | Volume | MARKET CAP |

|---|---|---|---|---|---|

| JAN | Janison Edu Group | 0.375 | 47% | 1,903,339 | $65,178,741 |

| T88 | Taitonresources | 0.125 | 47% | 97,772 | $4,570,836 |

| ACS | Accent Resources NL | 0.01 | 43% | 1 | $3,311,891 |

| YOJDA | Yojee Limited | 0.038 | 41% | 79,225 | $4,581,978 |

| TOY | Toys R Us | 0.008 | 33% | 368,323 | $5,894,781 |

| MKG | Mako Gold | 0.031 | 29% | 59,315,447 | $15,897,826 |

| AUR | Auris Minerals Ltd | 0.009 | 29% | 614,044 | $3,336,382 |

| ERL | Empire Resources | 0.005 | 25% | 2,410,000 | $4,451,740 |

| ESR | Estrella Res Ltd | 0.005 | 25% | 4,707,222 | $7,037,487 |

| PNX | PNX Metals Limited | 0.005 | 25% | 16,080,000 | $21,522,499 |

| XST | Xstate Resources | 0.02 | 25% | 2,902,138 | $5,144,306 |

| KNB | Koonenberrygold | 0.037 | 23% | 75,298 | $3,592,473 |

| ENV | Enova Mining Limited | 0.027 | 23% | 46,100,704 | $14,100,445 |

| NOX | Noxopharm Limited | 0.067 | 22% | 393,078 | $16,073,087 |

| BMG | BMG Resources Ltd | 0.017 | 21% | 11,703,005 | $8,873,160 |

| BRN | Brainchip Ltd | 0.2 | 21% | 14,723,611 | $297,959,423 |

| SNS | Sensen Networks Ltd | 0.03 | 20% | 49,897 | $19,306,790 |

| CCZ | Castillo Copper Ltd | 0.006 | 20% | 3,974 | $6,497,527 |

| RR1 | Reach Resources Ltd | 0.003 | 20% | 2,334,099 | $8,025,743 |

| TMK | TMK Energy Limited | 0.006 | 20% | 4,850,275 | $30,612,897 |

| WML | Woomera Mining Ltd | 0.006 | 20% | 3,456,220 | $6,090,695 |

| ADR | Adherium Ltd | 0.056 | 19% | 275,357 | $15,671,679 |

| SGC | Sacgasco Ltd | 0.013 | 18% | 1,490,000 | $8,576,558 |

| RHY | Rhythm Biosciences | 0.175 | 17% | 127,546 | $33,171,388 |

| AL8 | Alderan Resource Ltd | 0.0035 | 17% | 4,000,000 | $3,320,584 |

Janison Education Group (ASX:JAN) has been having a field day on Tuesday posting a 43% gain in the AM, on news that the company has inked a deal with the New South Wales Department of Education to deliver the state’s selective education placement tests as computer-based tests via Janison’s digital assessment platform.

The deal, which also includes Cambridge University Press & Assessment, is reportedly worth up to $45 million over the initial five-year term – provided all stages are approved – with an option for the department to extend for a further five-year term.

Mako Gold’s (ASX:MKG) position as market darling seems secure with the company landing another 25% jump this morning on the back of a string of happy announcements that kicked off at the end of January with the company’s quarterly.

Since then, Mako has revealed positive rock chip sampling results that suggest a “very high grade” find at Tchaga North, on the company’s 90% owned flagship Napié Project in Côte d’Ivoire.

Since 30 January, Mako has improved from a close of $0.011 to be at $0.032 per share at lunchtime today, and up 220% for the year so far.

And another junior goldie, Koonenberry Gold (ASX:KNB), was up 23% early in the day, improving on the previous session’s gains when it announced that Phase 2 drilling at the company’s Bellagio prospect has defined widespread gold mineralisation >1g/t Au over >125m area, with the target remaining open down dip and plunge.

The afternoon session saw a couple of small goldies meandering around on no news, including BMG Resources and Australasian Metals.

ASX SMALL CAP LAGGARDS

Today’s best performing small cap stocks:

Swipe or scroll to reveal full table. Click headings to sort:

| Code | Company | Price | % | Volume | MARKET CAP |

|---|---|---|---|---|---|

| HXL | Hexima | 0.011 | -31% | 980,000 | $2,672,634 |

| DY6 | Dy6Metalsltd | 0.063 | -26% | 144,462 | $3,357,145 |

| GTI | Gratifii | 0.006 | -25% | 538,660 | $10,953,781 |

| YPB | YPB Group Ltd | 0.0015 | -25% | 1,290,990 | $1,580,923 |

| WC1 | Westcobarmetals | 0.042 | -24% | 212,852 | $6,644,018 |

| EG1 | Evergreenlithium | 0.099 | -21% | 22,000 | $7,028,750 |

| TG1 | Techgen Metals Ltd | 0.031 | -21% | 2,795,659 | $4,958,170 |

| AZY | Antipa Minerals Ltd | 0.012 | -20% | 13,216,376 | $62,022,119 |

| SCN | Scorpion Minerals | 0.02 | -20% | 918,181 | $10,236,405 |

| AOA | Ausmon Resorces | 0.002 | -20% | 80,000 | $2,647,498 |

| CTO | Citigold Corp Ltd | 0.004 | -20% | 10,000 | $15,000,000 |

| NET | Netlinkz Limited | 0.004 | -20% | 24,089,340 | $19,392,242 |

| RMX | Red Mount Min Ltd | 0.002 | -20% | 895,074 | $6,683,940 |

| ROG | Red Sky Energy. | 0.004 | -20% | 3,688,950 | $26,511,136 |

| VML | Vital Metals Limited | 0.004 | -20% | 2,041,943 | $29,475,335 |

| OD6 | Od6Metalsltd | 0.11 | -19% | 127,086 | $7,427,092 |

| LPM | Lithium Plus | 0.165 | -18% | 563,360 | $17,197,640 |

| AMM | Armada Metals | 0.024 | -17% | 90,000 | $6,032,000 |

| BVR | Bellavistaresources | 0.1 | -17% | 150,000 | $5,953,317 |

| NAG | Nagambie Resources | 0.025 | -17% | 2,470,057 | $23,899,070 |

| CZN | Corazon Ltd | 0.01 | -17% | 130,200 | $7,387,175 |

| FAU | First Au Ltd | 0.0025 | -17% | 535,003 | $4,985,980 |

| GCM | Green Critical Min | 0.005 | -17% | 1,808,357 | $6,819,510 |

| IEC | Intra Energy Corp | 0.0025 | -17% | 7,117,258 | $4,982,345 |

| MSG | Mcs Services Limited | 0.01 | -17% | 70,728 | $2,377,196 |

In Case You Missed It

Altech Batteries (ASX:ATC) says it’s made great progress with the manufacturing of two 60kWh Cerenergy battery prototypes, to be used for conducting performance tests and qualifying them for customer use.

Strickland Metals (ASX:STK) has executed a series of acquisitions to consolidate the entire northeast flank of the prolific Yandal Greenstone belt in WA’s Goldfields region, about 50km north of Northern Star’s (ASX:NST) underground Jundee operation.

De Grey Mining (ASX:DEG) has signed an exclusive option agreement to potentially acquire the 1.44Moz Ashburton gold project, a move which could ultimately increase the production rate and mine life of DEG’s massive Hemi gold project

Arizona Lithium (ASX:AZL) has appointed Rhythm Engineering as the drill contractor for the upcoming program that will test two deeper brine formations at the 6.4Mt Prairie lithium project in Saskatchewan, Canada.

First drilling into the Julia vein system at the Papayal prospect has turned up epithermal gold and silver, confirming Titan Minerals’ (ASX:TTM) ability to grow the 3.21Moz gold resource at Dynasty.

Uvre (ASX:UVA) says that a geological mapping and sampling program has returned up to 1.64% U3O8 and 6.72% V2O5 from eight undrilled prospects at the company’s East Canyon project in Utah.

A maiden eight-week field program along the premium La Grande lithium trend in Canada’s James Bay has identified over 250 high priority targets, in what is set to be a landmark year for James Bay Minerals.

WA gold miner Ora Banda Mining (ASX:OBM) has delivered further news from Sand King that bolsters the firm’s belief the prospect could be developed into an underground gold mine of significance.

A soil sampling program returned strongly anomalous lithium grades from 383 infill samples for Belarox, at the company’s Bullabulling project some 50km west of Coolgardie.

Western Yilgarn (ASX:WYX) has renamed its Bulga project to the Ida Holmes Junction project to reflect the significantly enlarged footprint which results from its joint venture with Fleet Street Holdings.

Resource drilling at iTech Minerals’ (ASX:ITM) Lacroma Central graphite prospect has more than tripled the strike of mineralisation, which now extends over 1.7km.

Victory Metals’ (ASX:VTM) North Stanmore project is becoming an increasingly prominent heavy rare earths play after follow-up metallurgical testing achieved strong recoveries with low forecast costs, with about 54% of the resource classified as ‘critical metals’ by the US government.

Galilee Energy (ASX:GLL) has revealed that a number of industry participants are currently evaluating its Glenaras gas project in Queensland for potential investment as the company looks to strengthen its advance towards commercialisation.

African-focused explorer Haranga Resources’ (ASX:HAR) uranium prospectivity in Senegal continues to strengthen after results from the Sanela and Mandankoly prospects confirm RC drill targets after auger drilling.

TRADING HALTS

Culpeo Minerals (ASX:CPO)– pending an announcement on a proposed capital raising.

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.