News

Sydney, Melbourne house prices to weaken; Units surge as living crisis goes nuclear family

News

Westpac: It's a two-speed house market! AMP: It's simpler. There's more Australians than homes

Uncategorized

Via Getty

News

The pressure of climbing interest rates, stretched affordability, and the ‘fixed rate cliff’ stress tested the housing market through 2023, however resilience largely prevailed, says CoreLogic head of research, and author of the property data firm’s annual Best of the Best report, Eliza Owen.

According to Eliza, Aussie home values were ‘broadly resilient’ under these conditions, however, there were some signs that high housing costs were biting – with 2024 expected to be far more subdued for capital growth.

“Housing activity rebounded through early 2023 as buyers took advantage of lower prices, however towards the end of 2023 affordability constraints have become more pressing, skewing demand towards the middle-to-lower end of the pricing spectrum,” Owen said.

“Certainly, lower-priced housing markets such as Perth, Brisbane and Adelaide saw very resilient conditions through the national downswing period, and strong annual growth through to the end of November.”

Housing values made a full recovery through 2023, following a short, sharp decline of -7.5% between May 2022 and January this year.

Nationally, home values rose 8.3% from the trough in January, and increased 7.0% in the year to November. This was the equivalent of an annual uplift in the median home value of $49,583, to $753,564.

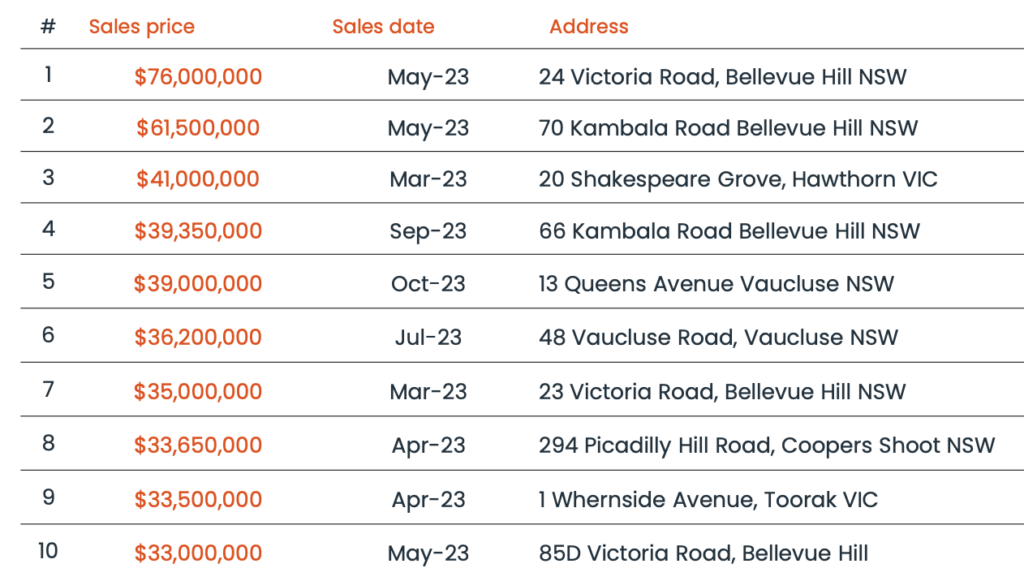

The national top 10 sales for the year featured Sydney’s usual Eastern Suburbs set, Bellevue Hill and Vaucluse, along with Melbourne’s Hawthorn and Toorak, plus Coopers Shoot in the Byron Shire of the Northern Rivers region.

Nationally, Mosman in Sydney’s Lower North Shore recorded the highest total value of house sales over the 12 months to September at $1.462 billion, with total unit sales in Surfers Paradise reaching $1.175 billion.

Across the capital city markets, Perth claimed eight of the top 10 spots for strongest growth in house values, with Brookdale, Armadale and Hilbert all up more than 30.0% annually and median house values sub-$550,000.

For unit markets, Perth (5), Brisbane (4) and Adelaide (1) took out the top 10 for largest gains, with units in Brisbane’s Slacks Creek surging 27.4% over the year, with seven of the top 10 recording median values under $400,000.

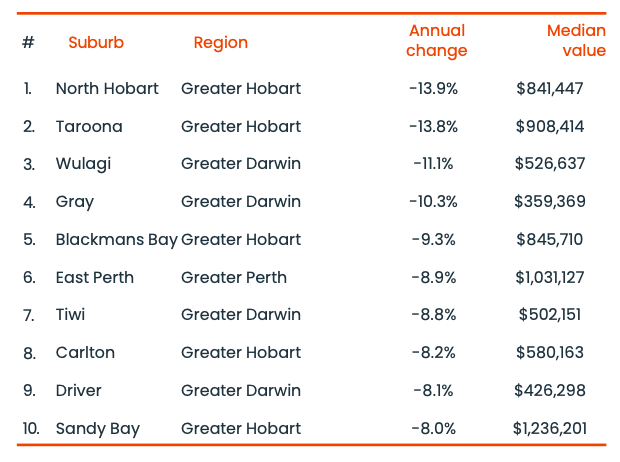

The weakest capital city house suburbs featured Hobart’s upper end, with North Hobart and Taroona down -13.9% and -13.8% respectively, while the top 10 worst performing unit markets were more diverse, spanning Hobart, Darwin, Melbourne and Canberra.

Across regional Australia, NSW’s Tralee was the top performing house market with 34.2% capital growth, while QLD’s Emerald saw the highest value growth for units at 20.9%. Rochester (VIC) was the worst performing house market, with values down -26.0%, while Mudgee (NSW) units recorded value falls of -11.4% over the past year.

2023 was marked by staggering levels of net overseas migration, largely influenced by the disruption that COVID-related border closures had on migration patterns.

Eliza says while this likely added some upwards pressure to home values, the most obvious response in housing metrics was in the rental market.

“Since the re-opening of international borders, strong rent growth was exhibited in markets with historically high exposure to overseas migration, and this is also reflected in the Best of the Best results for 2023.”

Nationally, Kensington in Sydney’s Eastern suburbs had the highest house rent growth in the year to November, up 24.9%.

And Lakemba in Sydney’s Inner South West saw the best unit growth, where rents soar 28.1%, closely followed by Wiley Park up 28.0%.

WA’s Kambalda East (15.5%) and Boulder (12.0%) recorded the highest gross rental yields nationally for houses and units respectively.

Looking ahead, Eliza reckons the recent deterioration in a range of market metrics are pointing towards a more subdued residential housing market in 2024.

“We’ve seen the pace of capital growth ease gradually from June and most notably through November. Transaction volumes nationally have declined an estimated -1.7% over November as well, which is unusual given sales volumes typically increase from October to November. These have coincided with a decline in the combined capitals clearance rate since June, which averaged just 61.7% through November.

“The RBA is forecasting a rise in the unemployment rate, we’re seeing a subdued pace of growth for GDP, slowing growth in disposable household income and the lowest household saving rate since the GFC at just 1.1%. Combined with an expectation that interest rates could hold higher for longer, households are likely to see their budgets further stretched, and more households may fall into acute financial stress.”

While the weakening in market conditions has so far had a greater impact on the upper end of Australia’s housing market, Owen said this may change over 2024.

“It is not uncommon for downswings to eventually cascade down to the more affordable segments at a lag. For this reason, even markets with very strong performance could see a reduction in the pace of growth through 2024. However, market conditions could once again strengthen towards the end of the year if there is a loosening in monetary policy,” Owen said.

On rents, Eliza expects rental growth will continue to slow, but may not decline nationally.

“In 2024, there are several factors which should support a further deceleration in rental growth. The first is that net overseas migration may start to normalise, as the ‘catch-up’ from overseas arrivals eases and departures increase through 2024.

“Secondly, stretched rental affordability is likely to see a gradual restructuring of rental demand. This includes migration to more affordable rent markets, both geographically and towards more affordable housing types such as units, and an increase in share housing and larger households.

“Thirdly, ABS lending data shows investment housing activity has seen a solid increase through 2023, while CoreLogic listings data indicates the rate of investment sales has been normalising. This should add to the supply of rentals in the coming months, helping to ease the rate of growth in rents.

“Finally, as more dwellings associated with the ‘HomeBuilder’ stimulus move to completion, we could see rental demand easing as tenants inhabit their newly built home. Annual growth in rent values has also broadly trended in line with interest rate movements over time, so if there is an easing in monetary policy next year, this will help to stem rent value increases.

“Unfortunately for renters, a slowdown in the rate of rent increases does not necessarily mean rents will fall. Some markets such as Canberra and Hobart have seen distinct falls in rent values through 2023, but even these declines are small relative to the upswing in rents.

“Hobart rent values fell -3.3% annually, while Canberra rents fell -2.0%. However, this follows strong rent value uplifts in both cities in recent years, and in Canberra the pace of decline in rents appeared to be slowing toward the end of 2023.”

News

News

Uncategorized

Mining

Mining

Mining

Get the latest Stockhead news delivered free to your inbox.