Sydney, Melbourne house prices to weaken; Units surge as living crisis goes nuclear family

Beautiful Pripyat, Chernobyl exclusion zone. View of the city center and residential buildings. Via Getty

Investment manager Ekam Capital has come out with some good stuff on the property prison encircling the nation.

The take-out messages:

- The Reserve Bank of Australia (RBA) is mean and will probs stay mean

- Big city prices will feel the squeeze first

- The slowing flow of housing finance historically foreshadows a similar slowdown in property prices

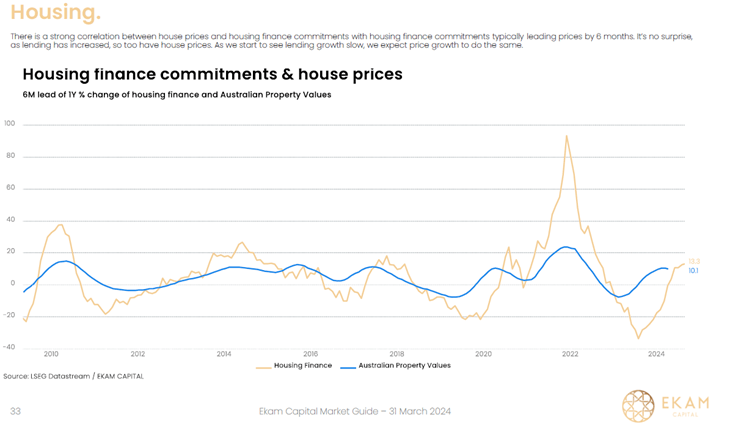

Soft as houses

Ekam’s research suggests that some gorgeous weakness in house prices is to emerge in the second half of 2024.

“Especially in Sydney and Melbourne, (as) the Reserve Bank of Australia (RBA) could keep interest rates on hold until the year’s end given the stickiness of inflation.”

Ekam Capital co-founder and director Robert Baharian expects the central botherers to keep rates where they are for now, and for the preposterous property market to slow down, most particularly in the eastern states of Australia thanks to mounting credit costs.

That makes sense. The average mortgage size in NSW reaches $744,000, well above that in Victoria at $590,500, and compared to an Australian average of $608,000 in March 2024.

“We think interest rates could remain on hold this year given that inflation in Australia remains sticky, especially services inflation, as the RBA pointed out this week… Unemployment remains very low and that is keeping Australians spending. The relatively high level of interest rates could cap growth in house prices, especially in NSW and Victoria.

“With share market gains slowing in recent weeks, this also suggests that property prices may have peaked in the short-term, and we expect house price growth to slow,” Baharian says.

The signs say slower

Robert says there’s also a strong correlation between house prices and housing finance commitments.

“Housing finance typically leads house prices by about six months. Home lending growth has slowed and we expect house price growth to do the same. With inflation where it is today, and interest rates at current levels, it could put a lid on how much people can borrow and therefore pull down mortgage growth,” he said.

Check out this chart – Ekam reckons the recent slowdown in mortgages growth could have this sort of hit on house prices.

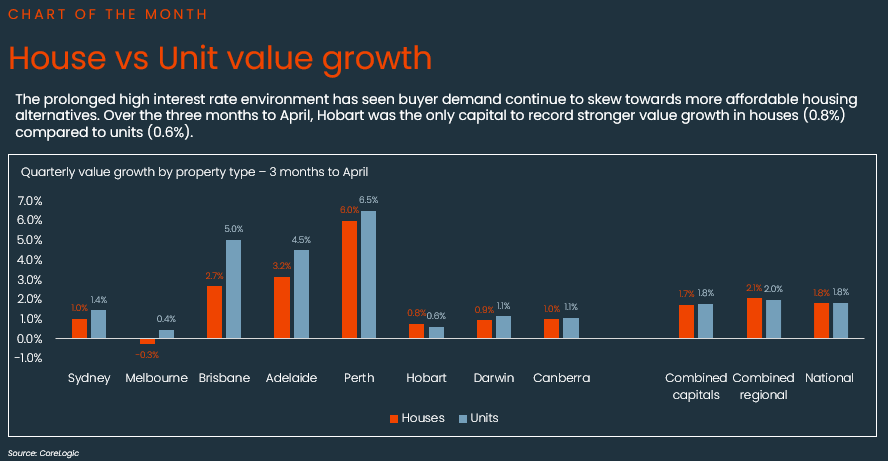

Units surge amid affordability crisis

Meanwhile, CoreLogic economist Kaytlin Ezzy has identified a decent bloody shift in buyer demand towards units, especially in capital cities where housing prices have gone quite nuts, and the already nutty buyers are being priced out.

“House values surged nearly 40% since March 2020, while unit values rose 17.9%, indicating the widening gap between house and unit values.

“Demand is now tilting towards unit and apartment living due to affordability concerns, particularly in capital cities. Hobart is the only capital that saw stronger value growth in houses (0.8%) compared to units (0.6%) over the three months to April.

“Given the worsening affordability environment and the growing possibility that interest rates could be higher for longer, it’s unsurprising that demand has skewed towards the more affordable unit sector.”

Bob: Rates on hold as inflation skews above target

“It’s hard to see the Reserve Bank of Australia cutting interest rates this year, especially with unemployment so low and services inflation remaining high. People are still spending, so inflation could remain above the reserve banks 2% to 3% target band for the remainder of the year,” says Baharian.

“Australians are funding their consumption out of their wages and also household savings, and this is pushing up the cost of services such as travel, leisure activities and eating out. I expect services inflation to stubbornly remain above the central bank’s target band.

“While both the unemployment and underemployment rate have been rising slowly, it continues to remain historically low which may keep inflation stickier for longer.”

Related Topics

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.