Pic via Getty Images

ASX Small Caps Lunch Wrap: It’s ‘hurry up and wait’ for the ASX ahead of US jobs data tonight

News

Pic via Getty Images

News

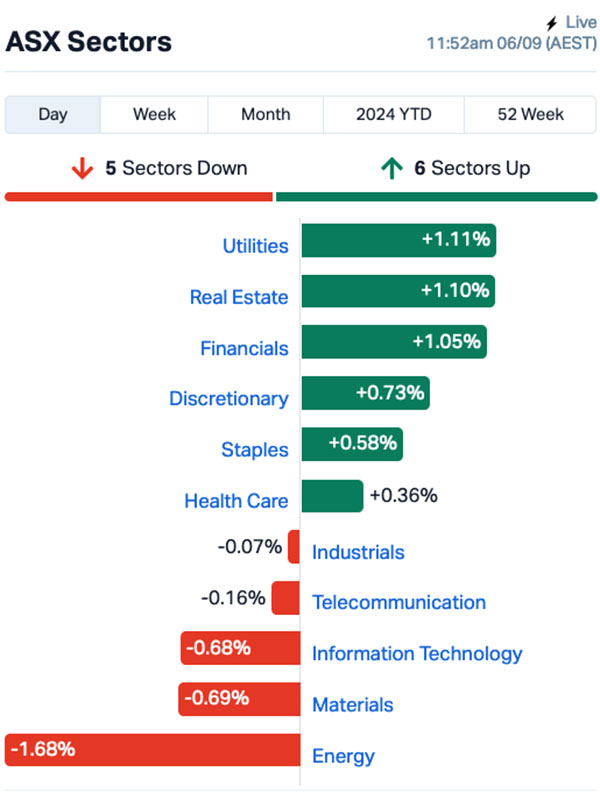

Local markets opened ever-so-slightly higher this morning, up 0.2% in the early moments of the session after another mixed session on Wall Street overnight, but was trending higher by lunch.

The Aussie tech sector has given back some of yesterday’s gains, and was about 0.7% in the hole on the way into lunch, while Resources continued to cop a pouding as investors maintained the sell-off momentum.

But it’s a good day to be a bank stock or a building, with Financials and Real Estate doing well enough to move the needle into the black for the ASX 200 benchmark.

Today is a case of “hurry up and wait”, though – there’s jobs data on the horizon for the US tonight which is being watched very closely, and we’re all bracing for more market volatility over the coming days.

How that’s going to play out for the ASX today, though, is very much up in the air, as the benchmark is trending higher immediately before lunch. Let’s go and see why.

Right off the bat this morning, it was clear that Energy and Materials were in for another difficult day, despite a decent bump for oil prices, which climbed around 2.0% overnight, with Brent Crude around US$72.80 a barrel pre-market.

There was some decent movement among the metals overnight as well, with iron ore seeing a 1.95% bump to US$92.70 per tonne, and copper rising 1.7%.

However, zinc and nickel both fell around 1.7% while you were asleep, which has left them down 6.0% and 5.4% for the week – alongside tin prices, which have also dived close to 6.5% since last Friday.

Gold is holding relatively steady around US$2,514/oz – but that hasn’t been enough to keep the goldies off the sell-list this week.

At midday, the market sectors looked like this:

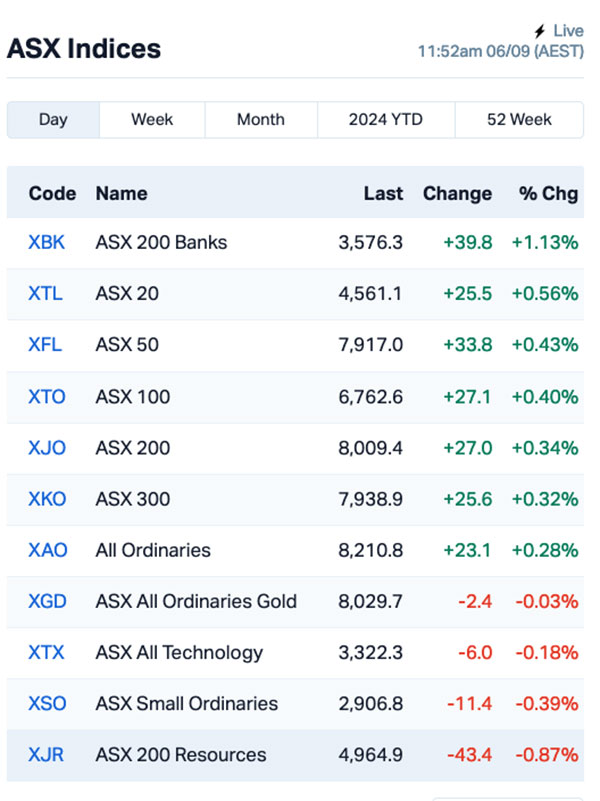

The banks were doing the heavy lifting through the opening portion of the session, with ANZ performing best of the Big Four on +1.2%, with Westpac and CBA neck and neck around +0.8% for the morning.

That might have something to do with RBA chief Michele Bullock’s comments yesterday that made it unequivocally clear that we aren’t going to see rate relief for a long time yet – at least until 2025, which is months away.

The US, however, is on track for its rate cut in September, which should help push markets along a bit – but that’s still about two weeks away from happening, and there’s some important (and dreaded) US job data due out tonight that will help answer the burning question that is fuelling the current volatility.

Is the US headed for a recession? Stay tuned to find out.

Meanwhile, up the big end of Ol’ Sydney Town, the latest ABS data bundle to drop has been our national home lending rates,

So… home lending is rising, rates are at blood-from-a-stone levels for at least 5% of mortgage holders… and the Banks are at the top of the ASX Indices chart. That makes sense.

And in other Aussie business news, the famed King Island Dairy is reportedly set to close by mid-2025, after owner Sapuro couldn’t find a buyer for the 120-year-old business.

Closure of the facility on King Island will impact 58 workers and their families, after Sapuro said that it has exhausted all avenues in its search for someone to take the business on.

The brand has been a staple among Australian cheese lovers for decades. I was particularly fond of the company’s Triple Cream Brie, so I – and my helplessly clogged arteries – salute you King Island Dairy, and thank you from the bottom of my cheese-riddled heart.

Wall Street was all muddled again overnight, ahead of key US jobs data due to land tonight (our time) that will offer more insight into precisely where the US economy is headed – because at the moment, no one seems entirely sure.

That’s largely because the US economy is undoubtedly slowing, but the rate at which it’s slowing isn’t all that clear – the numbers coming out of the US have been harder to read than a Russian textbook, with lower than expected unemployment and near-stagnant job growth pointing in both directions at once.

So, all eyes are on the August jobs report, due out at 10.30pm AEST tonight, which could be a game changer, Eddy Sunarto said this morning.

“If the report reveals fewer new jobs than expected and a rise in the unemployment rate, stocks might take a hit. The worry is that the Federal Reserve might not have acted fast enough to cut rates and prevent a recession,” Eddy wrote.

“The danger in really ‘bad news’ is that even if the Fed is prepared to react aggressively, it might be too late to stave off real economic weakness,” said Steve Sosnick at Interactive Brokers.

“Markets are still trying to figure out if the economy is slowing too much, and whether the Fed is behind the curve,” said Chris Larkin at E*Trade.

At the end of the US session yesterday, the S&P 500 was down 0.3%, the blue chips Dow Jones fell by 0.54%, and the tech heavy Nasdaq lifted by 0.25% after tech stocks climbed – but, unusually, that hasn’t been matched by our local techies, with that sector off by 0.4% this morning.

In US stock news, Nvidia jumped 1% following an 11% slump over the past two sessions. Analysts from Bank of America suggested that this recent drop presents a good buying opportunity.

Tesla rose 5% after announcing that its Full Self Driving service, which is a paid add-on for driver assistance, is set to launch in Europe and China in early 2025 – so if you’re there, stay off the footpath.

It’s worth noting here that Tesla is yet to finalise the necessary regulatory approvals in those markets… so, yeah. Definitely stay off the footpath.

And Broadcom, which supplies chips to Apple and other major tech firms, has given a weak revenue forecast, suggesting that slower demand for products beyond AI is affecting its growth. Broadcom shares fell 7% after hours.

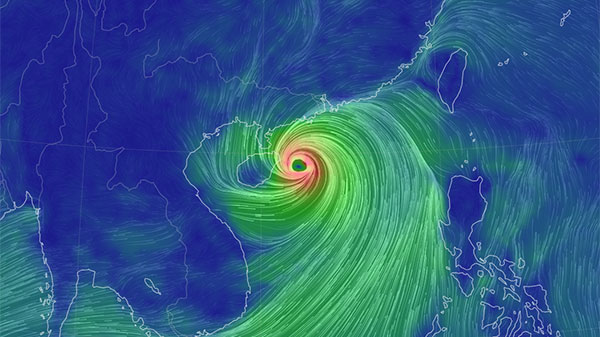

In Asian markets this morning, the major news is that Hong Kong has suspended trading this morning, as Super Typhoon Yagi, packing maximum sustained winds of 245km/h near its eye, descends on the region after giving The Philippines something to think about earlier this week.

It’s no surprise, really… it’s a mighty big storm, as you can see here on this awesome global windspeed map that I remembered to look at about 30 seconds ago.

Japan’s Nikkei is up 0.16%, and Shanghai markets – which remain open despite the inclement weather – are up 0.23%.

Here are the best performing ASX small cap stocks for 06 September [intraday]:

Swipe or scroll to reveal full table. Click headings to sort:

Code Name Price % Change Volume Market Cap OSM Osmond Resources 0.18 157.1 2,912,467 $4,435,389 ERA Energy Resources 0.007 40.0 1,321,316 $110,741,496 NSM Northstaw 0.017 30.8 322,824 $1,818,385 GCM Green Critical Min 0.0025 25.0 1,811,683 $2,937,085 MQR Marquee Resources 0.02 25.0 11,318,759 $6,662,150 SKN Skin Elements 0.005 25.0 104,516 $2,357,944 TSL Titanium Sands 0.005 25.0 1,300,000 $8,846,989 MKG Mako Gold 0.009 20.0 1,291,020 $7,399,643 ICG Inca Minerals 0.006 20.0 10,000 $4,052,682 PRM Prominence Energy 0.006 20.0 3,112,223 $1,556,882 BSX Blackstone 0.049 19.5 113,943 $21,645,414 AXL Axel Ree Limited 0.105 16.7 53,652 $6,697,699 HHR Hartshead Resources 0.007 16.7 668,835 $16,852,093 NRZ Neurizer 0.0035 16.7 507,839 $6,543,358 WBE Whitebark Energy 0.008 14.3 3,431 $1,766,334 ADG Adelong Gold 0.0045 12.5 1,057,750 $4,471,956 CCZ Castillo Copper 0.0045 12.5 100,000 $5,198,021 EFE Eastern Resources 0.0045 12.5 410,000 $4,967,786 MVL Marvel Gold 0.009 12.5 912,902 $6,910,326 VEN Vintage Energy 0.009 12.5 100,000 $13,356,250

George R. R. Martin, eat your heart out… Osmond Resources (ASX:OSM) was off to a flying start on Friday morning, coming back from a trading halt called while it announced that it has executed a staged acquisition for 80% of Iberian Critical Minerals, which currently holds a 100% interest in the capital of Omnis Mineria, which in turn holds a 51% interest in the capital of Green Mineral Resources, which in turn holds a 100% interest in the rights and title to the Orion EU Critical Minerals Project in Jaén Province, Andalucía, Southern Spain.

Prominence Energy (ASX:PRM) was also climbing, on news that Hartshead Resources has taken up a strategic investment in Prominence, in a private placement to HHR of $389,000 (before costs), giving HHR a 19.9% stake in the company. Managing Director Alex Parks has indicated that he will be leaving the company, while Bevan Tarratt has joined PRM as Executive Director and Quinton Meyers has also agreed to join PRM as a Non-Executive Director.

Marquee Resources (ASX:MQR) has revealed that it has recently completed a slim-line RC drilling program at the Redlings Rare-Earth Element project, with assays coming back from the lab showing 10 holes from this first sample batch have each returned + 10m at >1,000ppm TREO, including multiple near surface intercepts with peak assays of up to 5,850 ppm TREO.

Axel REE (ASX:AXL) was up mid-morning on an announcement that a geological reconnaissance and scouting program at its 100% owned, highly prospective and unexplored Itiquira Project is imminent, as the company goes in search of REE and niobium in Brazil. The project has 396km2 of granted exploration permits covering a significant portion of the Itiquira Complex, which is where the Araxá niobium mine is owned by CBMM, the world’s largest niobium producer and which accounts for approximately 80% of global supply.

Here are the most-worst performing ASX small cap stocks for 06 September [intraday]:

Swipe or scroll to reveal full table. Click headings to sort:

Code Company Price % Volume Market Cap AIV Activex 0.006 -33.3 60,000 $1,939,523 CNJ Conico 0.001 -33.3 982 $3,302,291 ECT Env Clean Tech 0.002 -33.3 11,594 $9,515,431 BIT Biotron Limited 0.019 -32.1 13,903,813 $25,264,659 AMM Armada Metals 0.01 -28.6 11,500 $2,912,000 LPD Lepidico 0.0015 -25.0 11,686,362 $17,178,250 RIL Redivium Limited 0.003 -25.0 598,295 $10,923,419 RML Resolution Minerals 0.0015 -25.0 2,447,620 $3,220,044 AL8 Alderan Resources 0.002 -20.0 375,000 $3,182,153 JAV Javelin Minerals 0.002 -20.0 1,755,783 $10,692,115 TX3 Trinex Minerals 0.002 -20.0 13,085 $4,571,631 GED Golden Deeps 0.061 -17.6 11,302,849 $8,974,154 HAR Haranga Resources 0.034 -17.1 302,646 $3,670,704 MRZ Mont Royal Resources 0.05 -16.7 65,636 $5,101,788 IS3 I Synergy Group 0.005 -16.7 169,742 $2,137,307 FCT Firstwave Cloud Tech 0.016 -15.8 548,440 $32,490,368 AKO Akora Resources 0.097 -15.7 387,561 $13,856,048 CMB Cambium Bio 0.305 -15.3 330 $4,295,162 BMM Balkan Mining 0.042 -14.3 166,169 $4,215,985 PAB Patrys 0.006 -14.3 325,440 $14,402,131

Strong support from institutional and sophisticated investors have allowed Lumos Diagnostics (ASX:LDX) to successfully wrap up the institutional component of its $10m entitlement offer, which offered one new priced at 3.8c each for every 1.82 shares held.

The institutional component raised ~$3.1m through the issue of about 81.7 million new shares.

LDX expects to open the retail entitlement offer, which seeks to raise the remaining $6.9m, on September 11, 2024. This is underwritten by the lead manager Bell Potter with sub-underwriting from Tenmile and Ryder Capital up to ~$6m.

Proceeds from the entitlement offer will be used to fund completion of the FebriDx CLIA waiver trial in the US, product development as well as sales and marketing activities.

At Stockhead, we tell it like it is. While Lumos Diagnostics is a Stockhead advertiser, it did not sponsor this article.