Is this the bull market we've all been waiting for? Pic via Getty Images

Crypto Espresso: Hold onto your butts – BTC’s on track to smash through US$30,000 any min-… ok it just did

Coinhead

Is this the bull market we've all been waiting for? Pic via Getty Images

Coinhead

Morning Coinheads! I trust you’ve all had an enjoyable Easter break, filled with love, happiness and chocolate – because while you were off doing Sweet FA for four days, Bitcoin was preparing a small Easter miracle for us all.

Rob “If I don’t take a break my head will asplode” Badman is taking a break, so here’s a lightning round of crypto news to keep you ticking over for the morning – and it’s all fantastic, provided you’re not up to your chin in Dogecoin and nothing else.

After hovering around the US$28,000 mark for a few days, last night – right around the time that many God-Fearing Americans would have been symbolically rolling the stone away from the entrance to Jesus’ Easter hideaway to find him missing (presumed alive), Bitcoin went soaring.

At the time of writing, it’s up better than 5.0% and is still climbing, albeit a little slower, but it’s past US$29,850 and making what looks like a pretty solid run at the $30k high-water mark.

Update – it just broke through the US$30,000 mark. Who’d be a crypto “journalist”?

That’s territory that BTC hasn’t seen since mid-June, 2022 – which is, like, 1,000 years in Crypto Time.

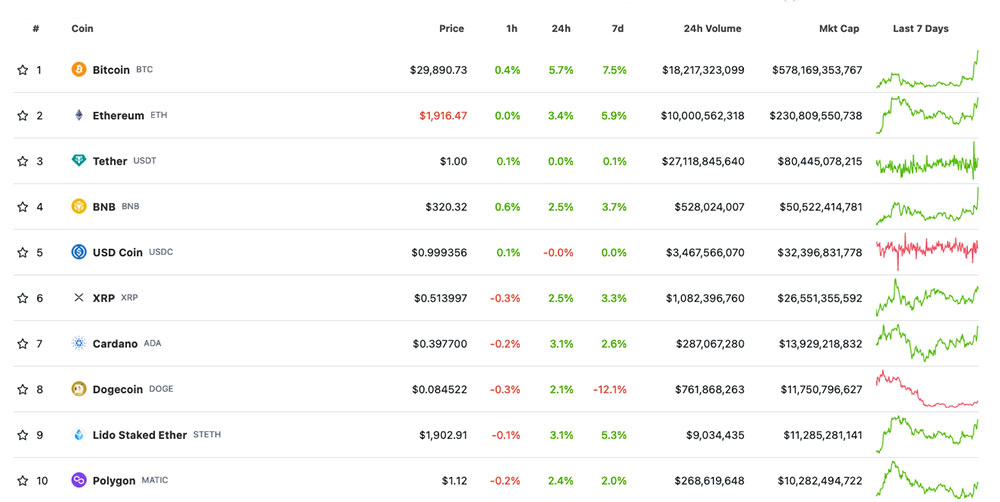

Broadly speaking, the Top 10 coins’n’stuff are all trending higher this morning, with the notable exception of Dogecoin, which… isn’t.

Some stats out of the internet, because that’s where stats come from, shows that searches for Dogecoin “surged 1,992 percent worldwide over the last seven days after Elon Musk changed Twitter’s bird logo to Dogecoin’s shiba inu on Monday, 3rd April”.

Our source on that is “research done by online casino guide 6Takarakuji” – so you know it’s 100% iron-clad legit, because nothing quite says “AbSolUtEly NOT DegENeRatE GamBLing” than crypto search stat research from an online casino ratings website.

Anyhoo… without wanting to dive too deep into The Musk (I’m definitely not a Muskovite or whatever his Loyal Followers are called), his not-even-vaguely transparent ploy to manipulate Dogecoin again (allegedly) seems to have backfired. Not just a little bit, either.

While the international search volume for Dogecoin has climbed nearly 2,000%, Dogecoin is the only non-pegged coin in the Top 10 that’s not done very well in the past seven days – in fact, it’s sunk 11.7% since Musk’s effort at a touch of crypto-theatrics. #WhataMug.

The next-worst performer is Polygon, up 2.07% for the week, and if you’re super-keen on the rest of the numbers, here’s a snapshot of where we’re at as of 11:30am today.

Fresh facepalming from the rubble of FTX this morning after the holder of crypto’s Most Poisoned Chalice, FTX CEO John Ray III, had to drop the court overseeing the bankruptcy debacle a note on Sunday, with a truly baffling little detail.

“FTX ‘kept virtually all crypto assets in hot wallets’,” John Ray III wrote in the filing. And for those wondering why that’s a bad thing, it’s because “hot wallets” are connected to the internet, and are – just like everything else connected to the internet – susceptible to interference from so-called “bad actors”.

(Not the Elon Musk-style bad acting, like the time he ruined an entire episode of The Simpsons. The other style of bad acting, like the time he changed the Twitter logo and crashed Dogecoin.)

Anyway, having an entire platform’s funds in hot wallets is hugely problematic on its own, but keeping the keys to the kingdom stored on AWS is kind of like leaving the welcome mat out and the door open for anyone who happens to wander by and feel like helping themselves.

Mining

Mining

Mining

Get the latest Stockhead news delivered free to your inbox.