ASX Tech September Winners: Sluggish September cures Wall Street’s IPO fever

Via Getty

- The tech sector had a down month in September

- The return of the IPO has been badly overstated

- We take a look at the ASX tech winners for the month

Sentiment towards growth stocks got another reality check in September as traders took a post-hold hawkish Federal Reserve to heart.

The tech-heavy Nasdaq Composite was off 5.8% in September, and down 4.1% for the quarter. The Nasdaq 100 lost 0.7% and spent the month of September in a happy tailspin.

The S&P/ASX 200 Information Technology (XIJ) index fell by 7.5% last month.

ASX 200 Information Technology (XIJ) Vs ASX200 (XJO) quarter

The precious American depositary receipts of Chinese-based, US-listed PDD Holdings (PDD) led the Nasdaq 100 over the the quarter with a gain of 42%.

The owner of online marketplace Temu reported Q2 earnings of US$1.44 a share on revenue of US$7.2 billion, while Wall St had expected US$1 a share from revenue of $5.95 billion.

Shares of the Chinese company also benefited from a Bloomberg report last month which suggested Beijing was toying with easing the rules that limit foreign ownership in domestic publicly traded companies.

Fed hits pause on US tech IPO party

US venture capitalists are advising their interest-rate struck start-ups to just hold off on any revivified plans to go IPO, according to the Financial Times, which says the stymied headline debuts of September have created more fear than fire.

After a conga-line of circling start-ups put a pin in any IPO plans once the market turned sour last year, the arrival of September thrilled fans of the initial public offering – long thought dead in the water for 2023 – after the Brit-based Arm and the online grocer Instacart pumped the field for future tech listings.

However, the honeymoon was short.

Instacart surged ahead 40% on September 19 within hours of the bell ring, but has ended the month below its US$30 listing price.

Much was made about Instacart’s barometric value for the orbiting 80-or-so IPO candidates which data firm PitchBook believes has built up over the last 12 months.

Arm, meanwhile was viewed as the great white hope for anyone with a fondness for chips, AI or British innovation.

After the bell, the SoftBank-backed chip designer enjoyed broad support, before eventually wobbling back down about its US$51 listing price in the weeks following. Arm is up, but the 5% gain etched in by Friday in New York is underwhelming.

Both companies were among the big names smacked by the Federal Reserve’s hawkish description of its September hold; US traders emotionally locking in another interest rate rise in the near future.

The hostile trading conditions last month have frustrated Silicon Valley investors, the FT says, who’d been banking on a door being opened ‘to dozens more private tech companies going public’.

Interest rate rises are particularly painful for unprofitable private start-ups, which are valued on the basis of their future cash flow. Until rates stabilised, instead of a resurgence in IPOs, expect an increase in M&A activity among private companies over the next six months.

China’s chips off the old block

Revenue from China’s top chip equipment makers surged in the first half of the year, research released Thursday showed, as Beijing continues to aim for self-reliance for its semiconductor industry.

The money poured in for China’s top 10 homemade chip equipment manufacturers, as revenue surged over 1H, according to new data from Shanghai-based CINNO Research.

The largest 10 firms shared revenue of circa 16.2bn yuan (US$2.2bn) in the first half of the year, up 39% year-on-year.

The chips and their components that go into everything from smartphones to Nintendos have been in the crosshairs of the White House and Chinese chip companies have been right at the axis of a broader tech war between the States and China.

Washington has sought to use export restrictions to cut off Beijing from key semiconductor equipment and technologies.

CINNO reports that Naura Technology Group became the biggest Chinese semiconductor equipment maker by revenue. Naura’s first half revenue hit more than 7 billion yuan, up 68% year-on-year.

Here are the top ASX Tech Winners for September 2023

Scroll or swipe to reveal table. Click headings to sort.

| Code | Name | Price | % Change | Market Cap |

|---|---|---|---|---|

| DXN | DXN Limited | 0.002 | 100% | $3,446,680 |

| SRJ | SRJ Technologies | 0.1 | 67% | $13,352,642 |

| ELS | Elsight Ltd | 0.395 | 44% | $59,376,234 |

| CNW | Cirrus Net Hold Ltd | 0.06 | 43% | $55,800,383 |

| RKT | Rocketdna Ltd | 0.014 | 40% | $7,474,497 |

| VTI | Vision Tech Inc | 0.305 | 39% | $10,625,268 |

| PIL | Peppermint Inv Ltd | 0.011 | 38% | $22,416,425 |

| ROC | Rocketboots | 0.14 | 33% | $4,880,775 |

| BCT | Bluechiip Limited | 0.025 | 32% | $17,841,762 |

| DUB | Dubber Corp Ltd | 0.145 | 26% | $54,711,142 |

| CT1 | Constellation Tech | 0.0025 | 25% | $2,942,401 |

| FBR | FBR Ltd | 0.0275 | 25% | $100,465,402 |

| ADS | Adslot Ltd. | 0.005 | 25% | $16,122,478 |

| ATV | Active Port Group | 0.125 | 25% | $25,007,178 |

| ZMM | Zimi Ltd | 0.04 | 25% | $4,671,996 |

| EIQ | Echoiq Ltd | 0.185 | 23% | $96,408,853 |

| WCG | Webcentral Ltd | 0.135 | 23% | $41,140,779 |

| SPX | Spenda Limited | 0.009 | 20% | $36,714,222 |

| GTK | Gentrack Group Ltd | 4.71 | 18% | $453,716,625 |

| EOS | Electro Optic Systems | 1 | 18% | $167,811,286 |

| AXE | Archer Materials | 0.505 | 17% | $121,052,331 |

| EML | EML Payments Ltd | 1.15 | 17% | $440,157,664 |

| EXT | Excite Technology | 0.007 | 17% | $8,464,692 |

Visioneering Technologies (ASX:VTI)

The US-based medical device producer, VTI is today welcoming its new Chief Executive Officer and executive director, highly-rated industry veteran Dr Juan Carlos Aragón.

Announced at the end of August, Aragón is a bit of a scoop for VTI and brings some 30 years of leadership in the vision care industry to VTI. His experience includes senior executive leadership positions in several large international vision care companies, and managing divisions for the Americas, Asia Pacific, and Europe.

Visioneering Technologies has a portfolio of technologies to address eye care issues such as presbyopia and myopia. The company has grown operations across the US and recently launched its products in Australia and New Zealand.

Market Cap at end of September: $10,625,268. Share price at end of September: 33.5cents, up 52%.

SRJ Technologies Group (ASX:SRJ)

SRJ Technologies Group provides specialised engineering services and containment management solutions, elevating customer’s integrity management performance. SRJ’s range of industry accredited products are designed to maintain and assure the integrity of pressure containment systems and therefore play an important role in the overall integrity of operating facilities.

The specialised engineering firm announced a capital raising to raise up to $1,200,000 to repay all amounts under the outstanding convertible notes held by Mercer.

CEO Alexander Wood said the capital raising initiative “reflects our commitment to strengthening our company’s financial position and capital structure.”

SRJ’s been on the hoof for funds in September and the share price has risen from the announcement when it said its immediate strategy is to grow its business by:

1) leveraging existing strategic partnerships to exploit revenue opportunities for SRJ’s disruptive products and solutions

2) offering a range of safe, reliable and technically superior solutions through continued innovation driven by customer demand; and

3) achieve market acceleration by expanding global client relationships and locations.

SRJ Market Cap at end of September: $13,352,642. Share price 0.1 cents, up 43%.

Cirrus Networks (ASX:CNW)

Cirrus added 30% mid-month on news that its Scheme Implementation Deed, under which Atturra would acquire 100% of Cirrus, was bumped up to $0.053 per share.

A leading Aussie advisory and technology services business in designing, implementing, and maintaining IT solutions, Attura and Cirrus agreed to amend the Scheme Implementation Deed (SID) dated 10 September 2023 by increasing the total value of Scheme consideration payable from $0.053 per Cirrus share to $0.063.

CNW is a Managed Service and IT solutions provider of technology solutions to SME and government organisations in Australia.

The company advise, integrate, manage, and secure customer IT environments with a modern, flexible approach and focuses on providing an independent flexible approach to designing, building, and managing IT infrastructure.

CNW Market Cap at end of September: $56,730,389. Share price $0.06, up 40%.

Elsight (ASX:ELS)

ELS is one of the more interesting ASX defence tech makers – a drone connectivity specialist. ELS says its flagship Halo delivers “absolute connection confidence” for drones and other unmanned systems.

A connected drone is a good drone.

In September, the company won Type Certification by the US Federal Aviation Administration (FAA) to the Halo-enabled Airobotics Optimus-1EX drone.

In historic news from @ExpoUAV the @FAA has granted @Elsight’s (#ASX: $ELS) #Halo enabled the @AiroboticsUAV Optimus-1EX system a Type Certificate to allow operations over people and infrastructure without case-by-case waivers: https://t.co/kDf7q7bt2x#BVLOS #DesignWin #drones pic.twitter.com/qq53bcg3mq

— Elsight (@elsight) September 7, 2023

Making the Optimus-1EX has now become the first and only non-air carrier drone in the world to have been granted the FAA Type Certification, allowing the drone to fly over people and infrastructure without the need for case-by-case waivers.

Elsight says this certification will significantly broaden the range of operational scenarios and scale up operations for automated Uncrewed Aircrafts (UAs).

ELS has already secured recent high-profile clients across US, Europe, South America, the Middle East and Asia.

These include delivery service provider DroneUp, used by US retail giant Walmart, Brazil’s SpeedBird Aero and Spright, the drone division of US medical services company Air Methods.

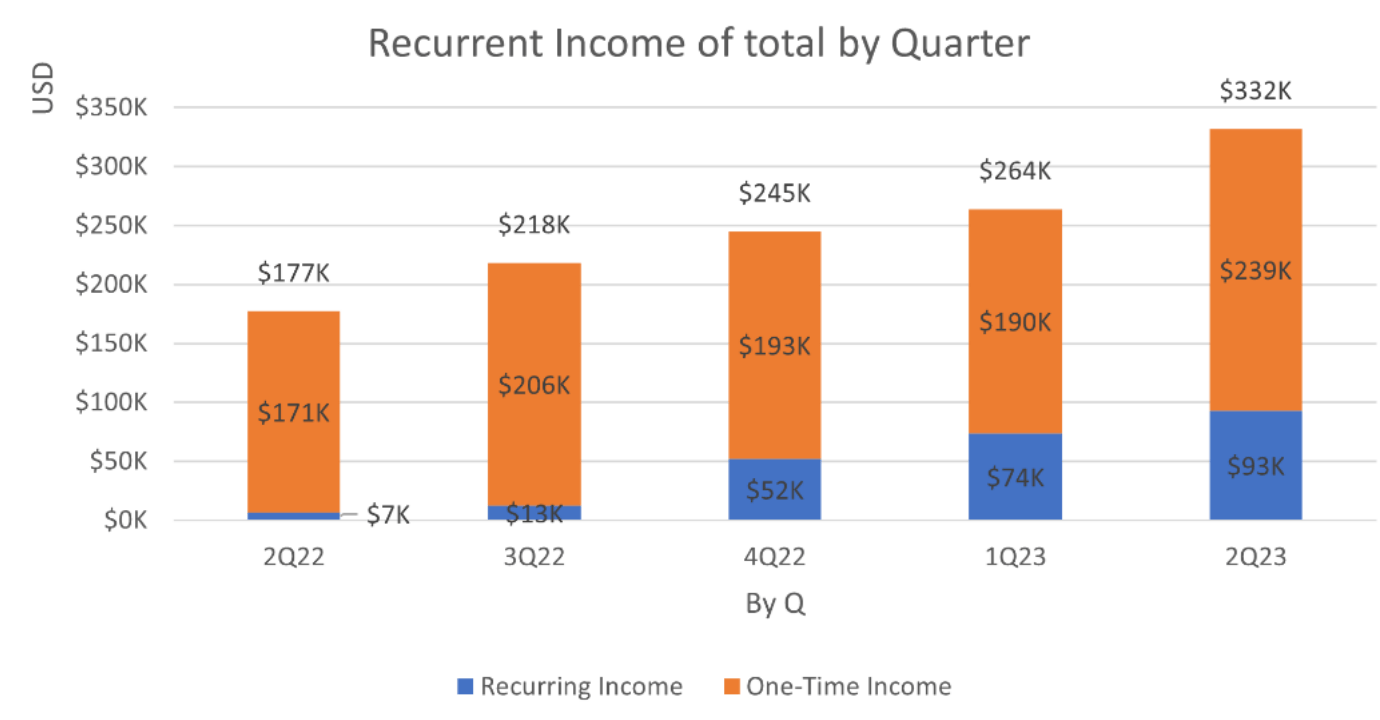

For the half-year ended 30 June, ELS halved its net loss on the same period in 2022 (which was US$2,246,917), largely the co said due to a renewed focus on trimming operational costs and an increase in sales revenues.

Despite the early stage nature of the drone industry, the group continued to deliver robust revenue growth, with the significant increase in recurring revenues a particularly promising metric.

Airobotics’ Optimus-1EX drone

Our Eddy Sunarto told me that the FAA Type Certificates (TC) hold significant importance and value in the aviation industry, being a mandatory prerequisite for all manned aircraft.

“Since the FAA began offering TC for Uncrewed Aerial Systems (UAS) in 2019, many drone companies have initiated this process… although Airobotics, focused on data capturing in urban environments, stands as the first to achieve it among numerous companies pursuing the TC.”

The company’s Optimus System is said to be among the most mature automated drone platforms in the market in terms of proven reliability and safety.

“We are proud that Airobotics has chosen the Elsight Halo as their connectivity solution,” says Elsight CEO, Yoav Amitai. “Their completion of the Type Certification with the Halo onboard is a vote of confidence in Elsight and in the Halo, and we expect many more to come.”

According to Custom Market Insights, the global UAV market size & share revenue was valued at circa US$26.8bn last year and is expected to reach US$29.1 billion this year.

By 2032, that number is expected to hit US$50.4bn at a CAGR of 8.2% between 2023 and 2032.

Elisght’s market cap at the end of September was $57.89mn. It’s share price was 0.39 cents, up about 25%

Related Topics

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.