Guy on Rocks: Tales from Ancient Greece and the case for nuclear

‘Guy on Rocks’ is a Stockhead series looking at the significant happenings of the resources market each week. Former geologist and experienced stockbroker Guy Le Page, director, and responsible executive at Perth-based financial services provider RM Corporate Finance, shares his high conviction views on the market and his “hot stocks to watch”.

Market Ructions: Gold tumbles after a breakout run

Gold (figure 1) plummeted in late trading Friday after a stronger than expected jobs report out of the US (adding 272,000 new jobs against market expectations of 180-200,000) coupled with an announcement by the Chinese Government they intended to place a pause on further gold purchases after 18 months of aggressive accumulation.

The Chinese are masters at the fake pass and are no doubt gearing up for another round of buying after softening up the market. The US$80 drop which saw the yellow metal finish the week at US$2,294/ounce was the largest one day drop since January 8, 2021.

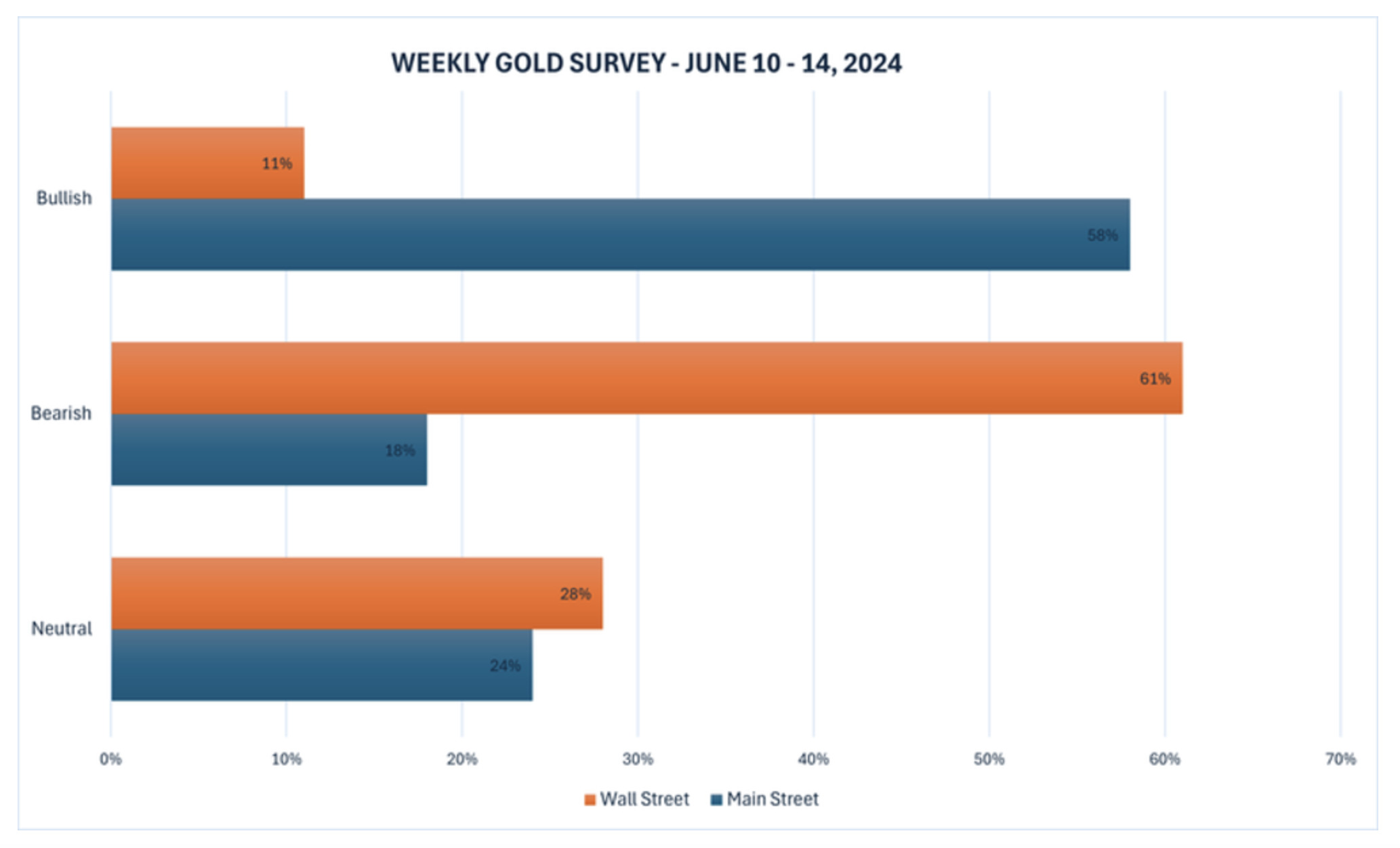

It shouldn’t be any surprise that last week’s Kitco gold survey has turned overwhelmingly bearish for this week (figure 2).

As the learned Stockhead faithful would be aware, and those that follow Chris Joye from Coolabah Capital, the fact that we didn’t have positive real interest rates in response to rampant inflation means the monetary response from global federal banks was always going to fall short of what was needed. Inflation in the US now appears to be running at around 2.7% compared to the target rate of 2%.

Not surprisingly, the US dollar was stronger with the DXY gaining 90 basis points on Friday to close at 104.94.

No doubt the FOMC meeting over 11/12 June will be watched carefully which will include a Summary of Economic Projections (SEP) containing a revised projection of possible rate cuts moving into 2026.

The Consumer Price Index for May will also be released at this meeting. Next week will revolve around the Wednesday morning release of US CPI for May, followed by the Federal Reserve’s monetary policy decision in the afternoon.

Other news out later in the week includes US PPI for May and weekly jobless claims. On Friday morning, the Preliminary University of Michigan Consumer Sentiment survey will be released.

Platinum (figure 3) and palladium (figure 4) also suffered. Platinum came off 7.5%, or US$78, to close at US$969/ounce as rising demand for EVs over ICEs – which accounts for around 40% of platinum demand as a catalyst, has seen the demand outlook soften.

Palladium dropped below US$900/ounce representing its lowest levels since mid-February and bringing its decline to around 18% year-to-date. Like platinum, weak auto demand has continued to weigh on the price.

Copper (figure 5) also got caught in the downdraft last week trading below US$4.48/lb off 15 cents or 3.3% for the week after the official Chinese PMI in May showed a 7.1% drop in imports of copper ore turnover despite the recent spike in the copper price. Chinese inventories, as I pointed out here last week, were at their highest levels since 2020.

I thought it would be worth responding to the recently released CSIRO report on nuclear energy that claims nuclear energy is more expensive than firmed renewable energy.

So here is a response from one of our esteemed analysts at RM that didn’t want to be named, but we can call him Dr No for the time being (hint: received the worst dressed award at the 2023 end of financial year lunch if you want to stand outside our office and watch the passing parade).

CSIRO GenCost Report

Any bastardised spreadsheet monkey knows these sensitive outputs can be adjusted to what is politically convenient through inputs – or as I prefer to call them – goal-seek values.

Fortunately, some smarter folks at the Centre for Independent Studies (CISOZ) have interrogated the assumptions and have made some very reasonable adjustments, which are illustrated in figure 6.

Not surprisingly, adjusting the pitiful 53% utilisation rate to 93% (average utilisation in US fleet), extending the model to 60 years (one could argue it should be longer) and applying minor adjustments to fuel prices, delivers a levelised cost of energy (LCOE) that is in line with firmed renewables.

“Firmed renewables” is an oxymoron as they can only be firmed with fossil fuels. CISOZ also acknowledges the other flaws in LCOE modelling including a nil cost assumption for transmission, nil capital cost for firmed energy or batteries, and more.

So, in summary, nuclear is roughly equivalent to renewables, even on CSIRO’s biased metric.

Funnily enough, even though nuclear power seems to be a strong investment case in other countries with energy alternatives cheaper than Australia’s, e.g., Russia and UAE – if nuclear makes sense in those gas-rich countries, how could the case not be equally compelling in Australia?

New Ideas… copper hopeful in elephant country

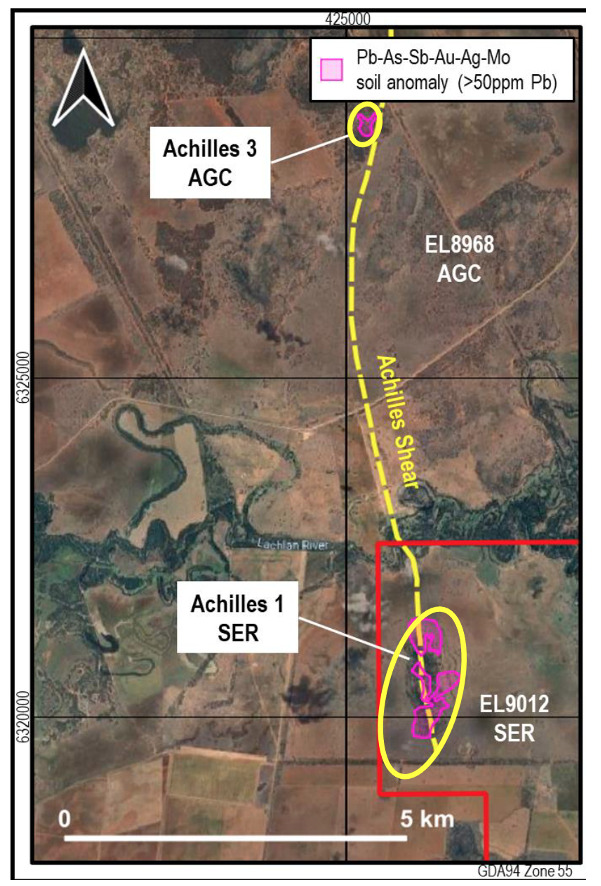

Strategic Energy Resources (ASX:SER) (figure 7) is led by David DeTata and has a portfolio of exploration ground in Australia (figure 8).

The company recently completed a placement at 1.1 cents to raise $2 million to provide funds principally for their South Cobar polymetallic project just 8km south of Australian Gold and Copper’s (ASX:AGC) Achilles 3 project where recent drilling has returned some impressive intersections including A3RC030 with 5m @ 16.9g/t Au, 1667g/t Ag & 15% Pb+Zn.

The provenance of the Cobar district is well known, with the CSA Mine, now owned and operated by Metals Acquisition Limited, one of the highest-grade copper mines in Australia with a mineral inventory of 20Mt @ 4.9% Cu for 1Mt of contained copper.

The near-term interest is focusing on the Achilles 1 prospect (figured 9 and 10) which the company believes is analogous to Achilles 3 as far as having a similar geochemical footprint along the same structure, namely the Achilles Shear.

The point of difference being the company interprets the Achilles 1 anomaly to be three times larger than Achilles 3.

Airborne magnetics/radiometrics were completed over the prospect at 100m line spacing with an Ultrafine+TM soil geochemistry program identifying a coincident Cu-Au and multi-element anomaly over 800m of strike.

An RC drill program has been designed to test Achilles 1 with land access agreement in place and drill pads already cleared.

While copper and uranium equities on the junior end have been slow to respond to recent commodity price volatility, the market does like a good nearology story with some meat on the bone, particularly in a district with a proven history of producing high-grade polymetallic deposits.

At an enterprise value of around $7m with approximately $3 million in cash, I think SER represents good leverage to any exploration success if AGC is anything to go by after its share price rocketed from 10c to 60c, giving the aspiring junior a market capitalisation a few weeks ago of over $140m at its peak.

Many of the Stockhead faithful would no doubt be Latin scholars and would vividly recall Achilles’ feats of bravery in Homer’s Iliad, including the slaying of Hector outside the gates of Troy.

I have a copy at my office and am more than happy to translate a few passages if anyone feels the need. Let’s hope Achilles is good for at least one more spectacular run…

The views, information, or opinions expressed in the interviews in this article are solely those of the interviewees and do not represent the views of Stockhead. Stockhead does not provide, endorse or otherwise assume responsibility for any financial product advice contained in this article.

Guy Le Page is a director and responsible executive at Perth-based financial services provider RM Corporate Finance. A former geologist and experienced stockbroker, he is involved in a range of corporate initiatives from mergers and acquisitions, initial public offerings to valuations, consulting and corporate advisory roles.

He was head of research at Morgan Stockbroking Limited (Perth) prior to joining Tolhurst Noall as a Corporate Advisor in July 1998. Prior to entering the stockbroking industry, he spent 10 years as an exploration and mining geologist in Australia, Canada, and the United States.

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.