US, Russia uranium tiff sees opportunity knock for Africa

ASX uranium plays in Africa are poised to benefit from Russian reprisal for US uranium import restrictions. Pic: Getty Images

- US and Russia tit for tat over imports and exports is opportunity for African uranium

- This is supported by US interest in diversifying and securing its supply chains

- ASX companies operating in Africa poised to benefit

Nuclear energy’s renaissance – propelled by the need for clean, emissions free baseload energy – has also delivered a corresponding boost for uranium.

However geopolitics being what they are, the world’s largest consumer of uranium – the US – and the largest producer of enriched uranium – Russia – are engaged in the usual bit of diplomatic tit for tat.

The US started the game by imposing restrictions on the import of Russian uranium products from 2024 to 2027 before moving to a full ban from 2028.

Uranium enrichment company – Centrus – did get a bit of a pass, securing a waiver to import low-enriched uranium from Russia for delivery to US customers in 2024 and 2025.

However, Russian President Vladimir Putin has signed off on a temporary ‘tit-for-tat’ ban on exports of enriched uranium to the US, a potentially serious hit given that Russia supplies 27% of US needs.

Unless the incoming Trump administration lifts the restriction on Russian imports, which might not be forthcoming given its preference for building domestic supply chains, it is not a stretch to believe the temporary Russian ban will continue for as long as the US maintains its restriction/ban.

Creating uranium opportunity

While the US will still need to build up its domestic uranium enrichment capacity, the stoush does highlight the need for the world’s largest uranium consumer to diversify its supply sources.

Focusing on domestic supply is well and good but might come at greater expense, which is why it behoves the US to seek out and encourage the development of uranium from other regions such as Africa, which has some of the world’s largest concentrations of the metal.

Not only will developing African uranium supplies provide a new source of the energy metal (potentially at a lower cost), it could also increase US influence in that part of the world, a potential counter to efforts by other major powers to increase their influence through programs such as China’s Belt and Road Initiative.

ASX plays in Africa’s uranium heartlands

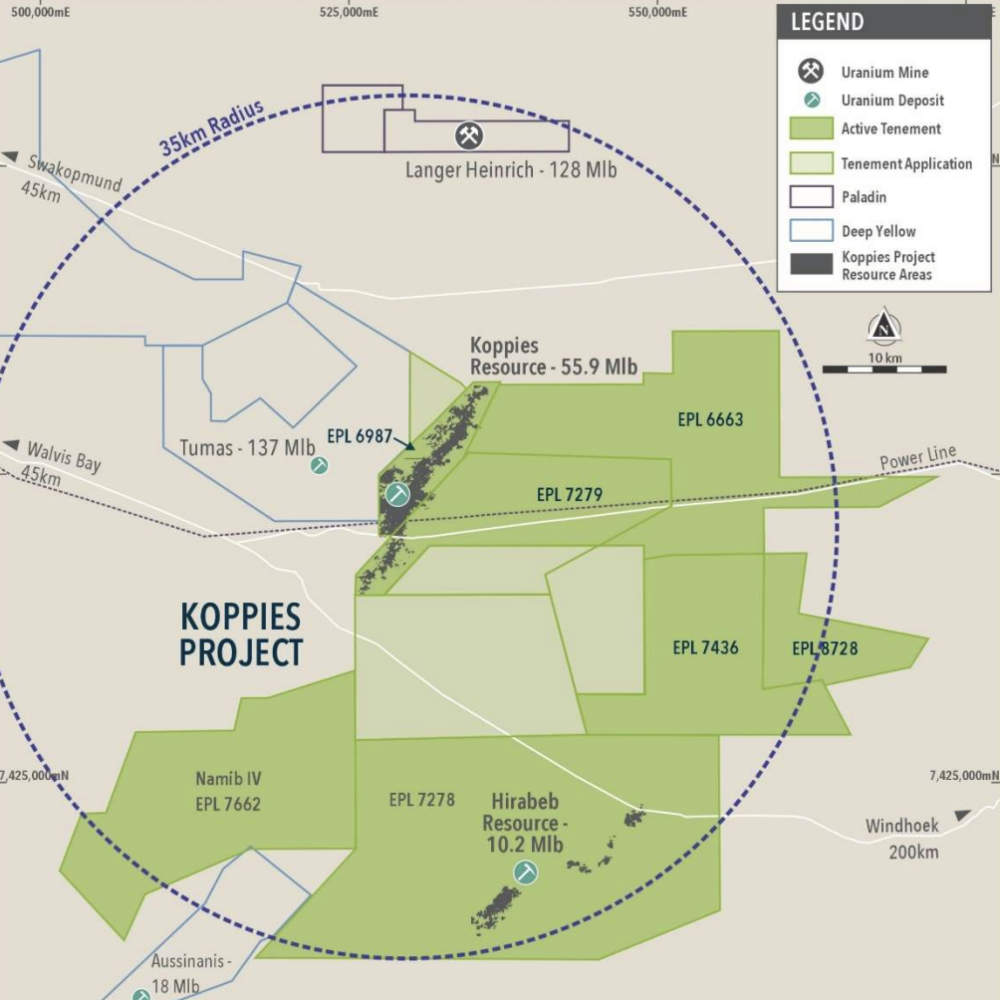

Countries such as Namibia – Africa’s top and the world’s third largest producer of uranium – are ripe for a development push and ASX companies such as Elevate Uranium (ASX:EL8) are perfectly poised to benefit.

EL8 operates the Koppies project. It boasts a global resource of 156.7Mt at 192ppm eU3O8, or 66.1Mlb of contained U3O8 with 78% of that (or 43.6Mlb) in the higher confidence indicated category that has enough geological certainty for mine planning.

It also has other projects that take its Namibian inventory up to 112.1Mlb U3O8.

The indicated resource is contained within a large continuous area about 7km from north to south and 3.5km east to west in the central area of the Koppies deposit with smaller pods to the west and north, a level of continuity that will undoubtedly benefit any future mining operation.

That Koppies is one of the shallowest uranium resources globally with ~95% being within 18.5m of the surface and 50% within 7m of surface – meaning potentially low strip ratios and low cost mining – certainly doesn’t hurt its chances.

Metallurgical testwork is currently underway using the company’s U-pgrade beneficiation process, that can upgrade calcrete ores like Koppies using less reagents.

Results will inform design of the demonstration plant which the company expects to start operating in mid-2025.

Another African uranium play is Moab Minerals (ASX:MOM), which is accelerating exploration of its Manyoni uranium project in Tanzania that was previously explored and extensively drilled by Uranex from the early 2000s until 2013, but was abandoned due to depressed uranium prices post the Fukushima incident.

The company is currently carrying out a 105 hole drill program to verify historical data and allow for the definition of a JORC 2012 compliant resource.

A recent $2m placement to raise exploration funds also including monies set aside for the completion of the $175,000 acquisition of four prospecting licences covering 488km2 that effectively consolidates the historical Manyoni project that were held by Uranex before 2013 under the company’s umbrella.

MOM is also planning to carry out exploration drilling to locate extensions to the known mineralisation.

This will be aided by ground geophysical surveys designed to locate buried alluvial channels and concealed faults, which are believed to control the high-grade uranium mineralisation.

It has already acquired high quality airborne geophysical data sets from the Geological Survey of Tanzania, which will assist exploration targeting.

Manyoni is just 5km from Manyoni town and benefits from access to modern railway and sealed highway infrastructure, as well as readily available power and water resources.

Aura Energy (ASX:AEE) is rapidly progressing its Tiris development in Mauritania to realise the significant inherent value in the project.

In its recent production target update study, the company outlined the potential for the project to deliver net present value of US$499m and an internal rate of return of 39% on the back of a resource upgrade to 91.3Mlb that can support the production of 43.5Mlb U3O8 over a 25 year mine life.

Post-tax life of mine cash flow has increased by 42% to US$1.5bn while payback will occur a couple of months earlier, improving from 2.5 years to 2.25 years.

Capex is estimated at US$230m with payback in just 2.25 years while all-in-sustaining cost is a low US$35.7/lb thanks to simple shallow pit mining and screening to beneficiate the ore before it is sent to a central leach plant using a slurry pipeline.

At Stockhead, we tell it like it is. While Aura Energy, Elevate Uranium and Moab Minerals are Stockhead advertisers, they did not sponsor this article.

Related Topics

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.