Up, Up, Down, Down: Which commodities won and lost in January … 2023

Pic: Tetiana Lazunova/iStock via Getty Images

- Last year’s undisputed champs coal and lithium fell back into the pack as iron ore, copper and gold enjoyed strong starts to 2023

- Uranium, nickel and rare earths also rose to start the year

- China’s reopening from pandemic restrictions has proven positive for most metals

Prices correct as of January 31, 2022.

WINNERS

Iron ore (SGX Futures)

Price: US$127.14/t

% Change: +9.5%

Iron ore has enjoyed a stellar start to 2023 on unbridled optimism from traders about the reopening of the Chinese economy after a 2022 blighted by its Covid lockdowns.

With Chinese industry now out in the wilds — the official NBS PMI expanded for the first time in three months in January while the smaller independent Caixin PMI rose slightly — there are hopes for the release of pent up demand from China.

There are a couple of threats potentially hanging over iron ore prices. Firstly, is the start of State-sponsored buying by centralised China Mineral Resources Group, intended to concentrate negotiating power in iron ore purchases in the hands of China’s state-owned steel mills.

Secondly, work now appears to be motoring along on the construction of the Simandou iron ore mine in Guinea, where Rio Tinto (ASX:RIO) and a host of Chinese companies are planning to bring anywhere between 60-200Mtpa of high grade seaborne iron ore to market by later this decade.

While iron ore producers like BHP, Fortescue (ASX:FMG) and Rio Tinto are all bullish on China, some headwinds remain.

Its property market is yet to fully recover from a debt crisis and the impact of its austere Covid Zero policy, while globally steel production has taken a hit from a broad economic slowdown, with crude steel output falling 4.2% to ~1.878Bt in 2022.

Iron ore miners share prices today:

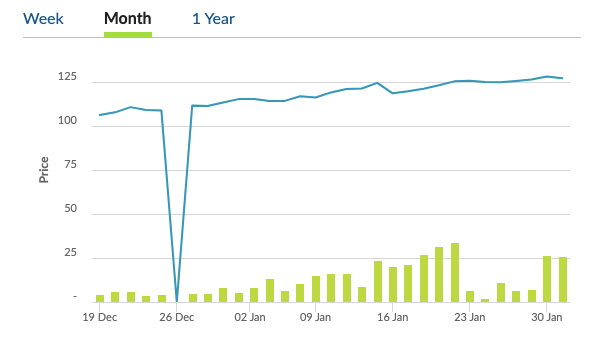

Uranium (Numerco)

Price: US$50.75/lb

% Change: +4.36

Uranium bulls always seem to be ready for this year to finally be the nuclear fuel’s year, with another false dawn in 2022 as prices rose early to their highest levels since the Fukushima nuclear incident in 2011.

They retreated, but still ended the year ahead, enabling a handful of miners such as Paladin Energy (ASX:PDN), Boss Energy (ASX:BOE) and Peninsula Energy (ASX:PEN) to announce project restarts.

Whether they have jumped the gun, or pushed the button at the right time remains to be seen.

There are expectations from within the industry that nuclear’s rebranding as a form of green energy will gain favour from governments both looking to extend the lives of their reactor fleet and build new ones as small modular reactor technology gains a foothold in the market.

Also, that the cutting off of Russia from the global economic community will lead to a growing need for utilities to purchase material from geopolitically safe sources of supply. Cameco, the west’s biggest uranium player, thinks the market is better positioned than it’s ever been.

“We’re in the early innings of a contracting cycle and we’ve never started one from this high of a uranium price before,” Cameco CFO Grant Isaac told a CIBC insto conference in Canada last month.

“If supply was outpacing demand it wouldn’t matter would it, but that is absolutely not the case.

“While I say the demand outlook is the best ever, I’d say the supply outlook is more uncertain than it’s ever been.

“On the primary production side it is absolutely a fact that the existing production assets are facing challenges, supply chain challenges, logistics challenges, anyone following us would know it’s very difficult to get central Asian supply out of Kazakhstan right now.

“On the primary side it turns out markets work. After years of low prices no one has been meaningfully investing in new supply, there are some projects being promoted but let’s be clear, nobody is seriously building a new mine right now.

“And in fact many of these projects you see that look really attractive, remember they’re trading on 2019 numbers, nobody has really updated those studies to reflect what’s been happening from an inflation and supply chain point of view.”

With inflationary pressures impacting the sector, Boss Energy MD Duncan Craib agreed with that assessment, saying utilities or the spot market would need to offer US$80/lb to incentivise undeveloped sources of production.

Uranium share prices today:

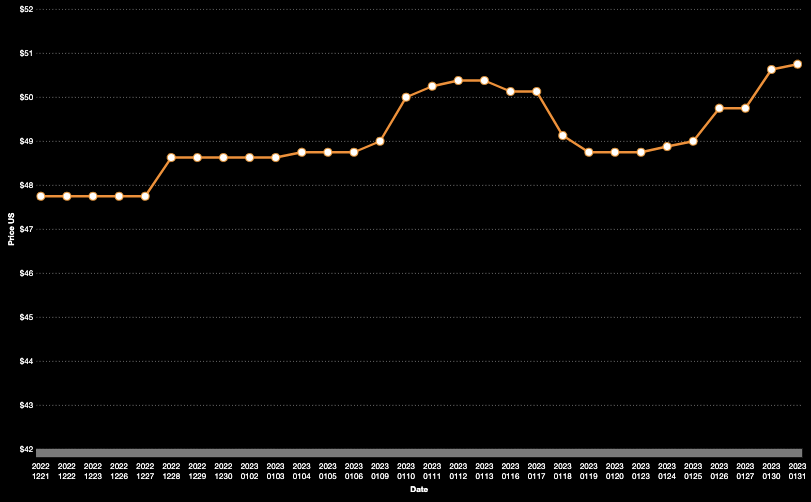

Gold

Price: US$1923.90/oz

% Change: 6.15%

Gold was volatile in 2022 but in January the only real way was up. One thing we haven’t had yet is interest rates announcements, something that may well prove a thorn in the side of the precious metal.

But with geopolitical uncertainty and economies across the globe on the rocks, there is one thing for certain — there will be investment demand for the safe haven commodity.

While much of the year was spent in a funk, with gold threatening to break below US$1600/oz at one point during the US Fed’s 75bps at a time rate hiking fever, bullion actually saw a record full year price in 2022 and its strongest levels of annual demand in 11 years, according to the World Gold Council.

Up 18% YoY to 4741t, that came off the back of a buying spree from central banks, which added more gold than at any point in the past 55 years at 1186t.

Will this translate to higher prices? That remains to be seen. While expectations are high — and they need to be given high costs mean a lot of gold miners are struggling to turn a profit even at record high prices — a lot will depend on how severe American rate rises get to contain inflation in 2023.

Gold miners share prices today:

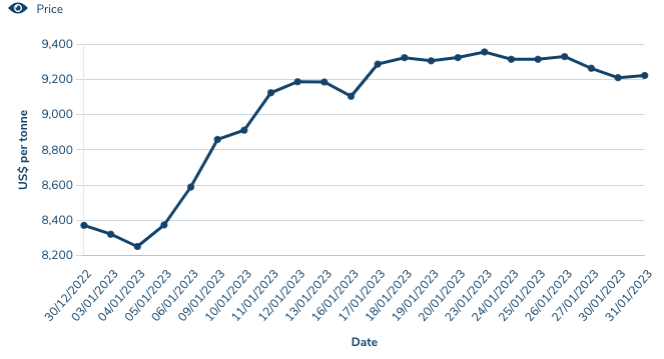

Copper

Price: US$9222.50/t

% Change:+10.16%

Can copper return to sky high levels predicted by backers like Goldman Sachs. Or are we heading into Musk’s metals cornucopia, whereas opposed to virtually every analyst on the market we have all the copper we need to power the energy transition right now.

Copper is a major beneficiary of strong economic conditions and, more specifically, of Chinese industrial activity.

With bullish expectations on China post-pandemic, traders are going long on copper at increasing rates. That has raised concerns from some market watchers the red metal may have gone too far, too fast.

Capital Economics commodity economist Kieran Tompkins wrote last month that industrial activity in the Middle Kingdom didn’t actually have as far to rebound as many people thought:

“Even though infections were more widespread in the reopening wave, manufacturing activity still remained remarkably resilient,” Tompkins said.

“Our China Copper Demand Proxy suggests that demand growth proxied by activity in end-use industries was, outside of the period around the Shanghai lockdowns, robust for much of last year. What’s more, China’s imports of copper ore and semi-refined copper actually rose last year.”

However, he thinks it is looking good for the second half of 2023.

“That said, we expect copper demand by end-users to rebound later in the year alongside the recovery in economic growth that we forecast,” Tompkins said.

“So, if we are right in this view, we expect the copper price to drop back towards $8,500 per tonne over the next few months.

“But, once growth outside of China accelerates and some recovery in China’s housing market starts to come into view, we think the price could make a subsequent recovery to $9,250 by the end of the year.”

Copper prices have also been propped up by the threat of supply cuts in Peru, where political unrest has led to the suspension or potential suspension of major copper mines such as the Las Bambas operation owned by China’s MMG.

Copper miners share prices today:

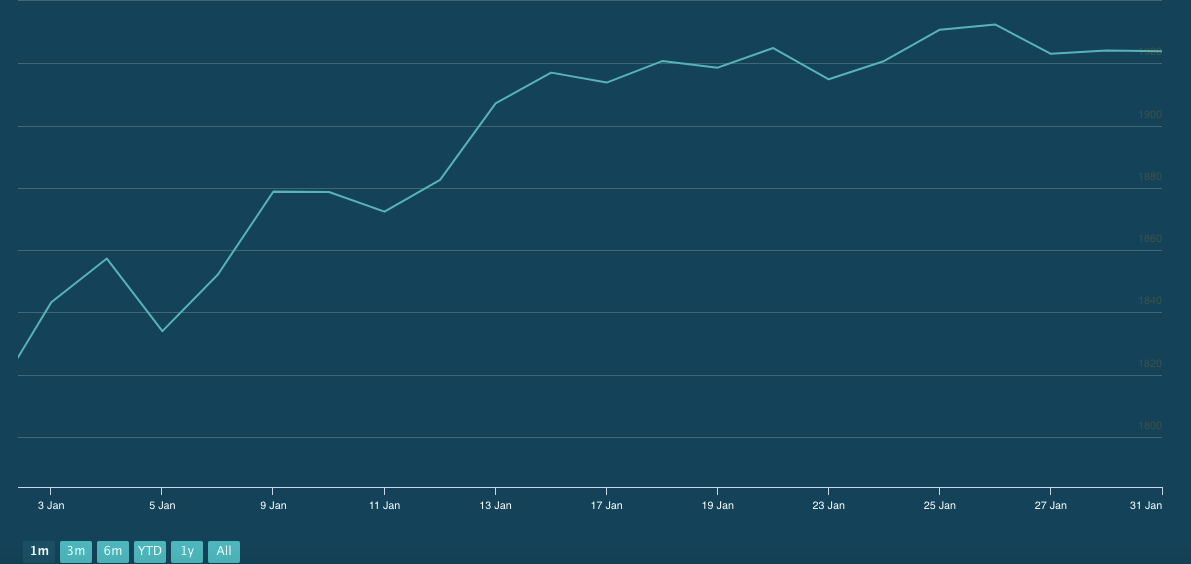

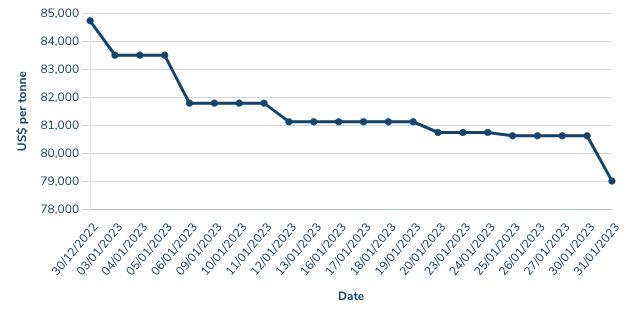

Rare Earths (NdPr Oxide)

Price: US$110.30/kg

% Change: +6.06%

Rare earths has become the latest rich person’s play thing in the Australian resources market, with the iron ore moguls who made it big off the iron ore boom — think Andrew Forrest, Gina Rinehart and Chris Ellison — piling into the future facing commodity.

The mail on rare earths, and particularly the most-prized metals in the group of 17 elements neodymium and praseodymium, is that the rise of electric vehicle production and wind turbine generation will see major growth in the market over the coming decade.

“The question being where will demand come from? Is it from China or is it from outside China and that’s the game that is being played at the moment … and there is a lot to do in the West to not lose this fight against China, and that is that is yet to be seen,” Pol Le Roux, COO of ex-China market leader Lynas Rare Earths (ASX:LYC), said on a recent conference call.

“We see a lot of announcements of new magnet projects (but) so far outside China, I’ve seen only one new factory in Vietnam — Fujitsu — but that’s an existing magnet maker. And that’s a very excellent customer of Lynas. But that’s the only one which did actually increase production outside China so far, so we’ll see.”

Prices for NdPr averaged US$83/kg after VAT in China through the December quarter, but have begun to tick up steadily as the country has emerged from its Covid isolation.

Lynas faces a potentially tight deadline to complete a cracking and leaching plant at Kalgoorlie in WA by the middle of this year, though the miner is appealing conditions placed on the three-year licence extension it received in 2020 allowing it to keep importing ores with naturally occurring radiation from its Mt Weld mine in WA until mid-2023.

Its Kuantan processing plant has operated for around a decade, but has long been the subject of political opposition in the local community over its disposal of low-level radioactive waste. Lynas boss Amanda Lacaze said this week the miner’s safety record showed it was a responsible operator in Malaysia.

“Our position is very strongly that we … run a low risk operation. We are a lawful company, which is compliant with all regulations and we have never been involved in any sort of health or environmental incident,” she told analysts.

“The most compelling data that we have is now our 10 years of safe operations in Malaysia.”

Rare Earths share prices today:

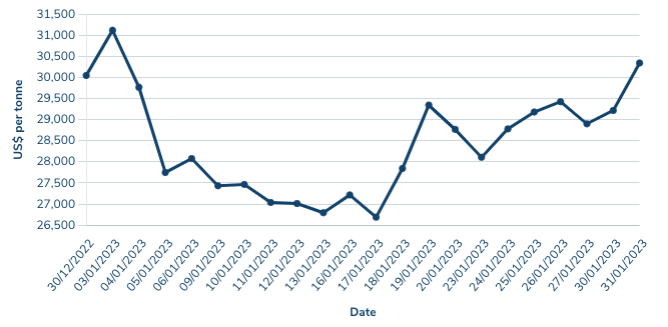

Nickel

Price: US$30,344/t

% Change: +0.95%

Nickel prices enter the year at their strongest position in well over a decade, with electric vehicle sales growth supporting the strongest nickel fundamentals since a brief run to US$50,000/t in 2007 at the height of the China boom.

They’ve fluctuated since entering the year at over US$30,000/t, ending January at a slight premium to their 2022 finish.

Nickel production on the other hand has been hit by escalating costs, with both IGO and Panoramic Resources (ASX:PAN) flagging a big increase due to inflationary forces.

Mincor Resources (ASX:MCR), meanwhile, will need to increase its deliveries to BHP’s Kambalda nickel concentrator by 300pc through the second half of FY23 to meet its 8000-10,000t guidance for its first year back in production since 2016.

Much of the growth to fill orders from battery makers seems likely to come from fast-moving jurisdiction Indonesia, where nickel pig iron producers are increasingly focused on delivering nickel into batteries.

Among those joining the party are ASX-listed Nickel Industries (ASX:NIC), which announced a US$471 million capital raise in early January, used to purchase a stake in a new HPAL development and options in two future battery grade nickel projects.

It had previously been assumed Indonesian low grade lateritic nickel would be more suited to the stainless steel market, but the country with the aid of Chinese and other international companies has moved fast to build out a battery supply chain based on its high level of nickel endowment.

Nickel Industries was barely a drop in the ocean in terms of global nickel producers five years ago before its $200 million ASX IPO. Now if all its project options are exercised it could be producing as much as 156,000tpa of nickel metal, two-thirds of that in the class 1 market.

Nickel miners share price today:

LOSERS

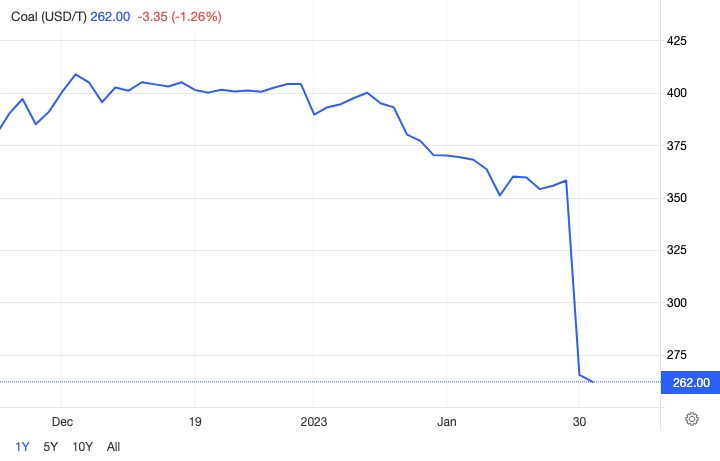

Coal (Newcastle 6000 kcal)

Price: US$262/t

% Change: -35.17%

Thermal coal’s front month futures have suffered a big fall since the start of the month.

Don’t get us wrong, at these prices coal miners shipping out of the Port of Newcastle should still make handsome profits, if they can ensure the NSW Government’s attempts to sequester production for the local market don’t hit them too hard.

Even with a major lift in costs reported across pretty much all the major operators including BHP (ASX:BHP), Whitehaven (ASX:WHC) and New Hope Group (ASX:NHC), exports remain very much in the money for the cashed up coal crowd.

The main driver of thermal coal’s dramatic January drop (to levels that would still have been a record in late 2021), has been a milder than expected northern winter, which has seen strong gas reserves and lower natural gas prices in Europe, along with an arbitrage between Newcastle and South African API4 prices.

Energy coal prices often track gas indices as when gas costs are high, coal use rises because it is cheaper to run.

On the flip side, premium hard coking coal prices have surged, moving in excess of US$330/t and reclaiming their historic premium over Newcastle 6000kcal thermal coal for the first time since June 1.

Among the driving forces has been a recovery in Chinese economic optimism post its Covid lockdowns, and signs Australian coal will be able to be sold into the key steel market for the first time since October 2020.

Coal miners share prices today:

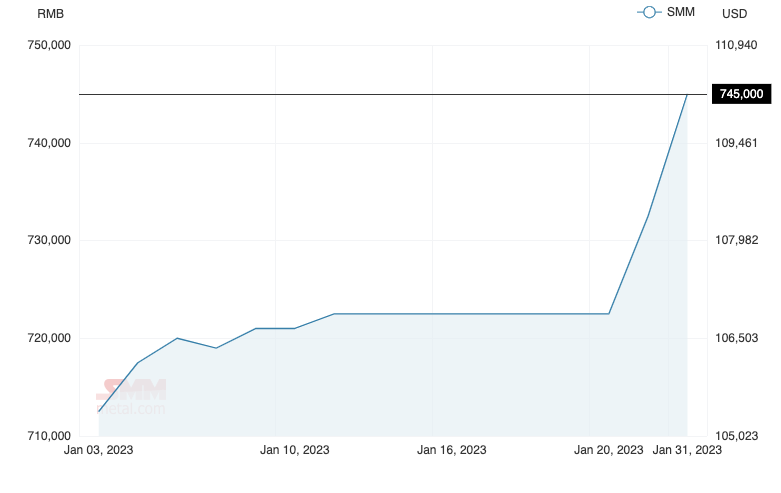

Lithium (Fastmarkets Hydroxide CIF China, Japan and Korea)

Price: US$79,000/t

% Change: -5.4%

You probably didn’t expect to see coal and lithium, up 138% and 132% in a ridiculous 2022 for the commodities on both sides of the energy transition coin, as our two losers for January.

Or maybe you did, believing in the gravitational theory of what goes up must come down or some fundamental Sachsian bearishness around the lithium market.

Good news for stonks. Lithium hasn’t collapsed yet, and those in the biz don’t think it will.

Take Patriot Battery Metals (ASX:PMT) chairman Ken Brinsden’s thorny response to Elon Musk’s suggestion all we need is refining capacity to get the lithium we need to EV producers.

“There’s no point in having refining capacity if you don’t have the raw materials and it feels like they are imagining you can generate the lithium raw material from thin air and refine it,” Brinsden said.

“Obviously, the industry just doesn’t work like that and if ever you needed evidence to indicate that it’s the raw material that’s in shortage have a look at firstly, the cost of spodumene … and then the other is the cost of the value added products.”

Those high spodumene prices are still stacking up for producers. Pilbara Minerals (ASX:PLS) raked in US$5668/t in the December quarter at a sub-grade 5.4% Li2O basis (benchmark standard is 6%, though high prices incentivise companies to deliver products with lower concentrations).

Allkem (ASX:AKE) and IGO (ASX:IGO) saw something similar for their Mt Cattlin and Greenbushes mines, with IGO announcing a record interim dividend of 14c largely attributable to its share in the TLEA JV with China’s Tianqi. At the same time there are signs inflation and regulatory issues will make new lithium harder to bring to market.

Allkem received environmental approvals for its James Bay deposit in Quebec, Canada, but not before a five-year wait. Liontown Resources (ASX:LTR) meanwhile copped a major blowout on costs at its Kathleen Valley lithium mine, up $350m to $895m as scope changes, inflationary pressures and the need for additional labour to hit a mid-2024 timeline sent capex estimates up 65%.

Lithium stocks prices today:

OTHER METALS

Prices correct as of January 31, 2022.

Silver

Price: US$23/oz

%: -3.96%

Tin

Price: US$29,490/t

%: +18.87%

Zinc

Price: US$3389/t

%: +14%

Cobalt

Price: $US49,000/t

%:-5.68%

Aluminium

Price: $2532.5/t

%:+5.87%

Lead

Price: $2136.5/t

%: -6.33%

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.