Up, Up, Down, Down: Narrative flipped on its head as struggling nickel, coal lead February gains

The game is freaking cheating. All the metals everyone hates put in a decent February showing. Pic: Richard Bailey/Photodisc

- A turn up for the books: Nickel and coal the biggest gainers among major commodities in February

- Copper, lithium and graphite remain steady at low levels amid hope a bottom has been reached for battery metals

- Iron ore and rare earths come off the boil as Lunar New Year hits industrial metals hard

WINNERS

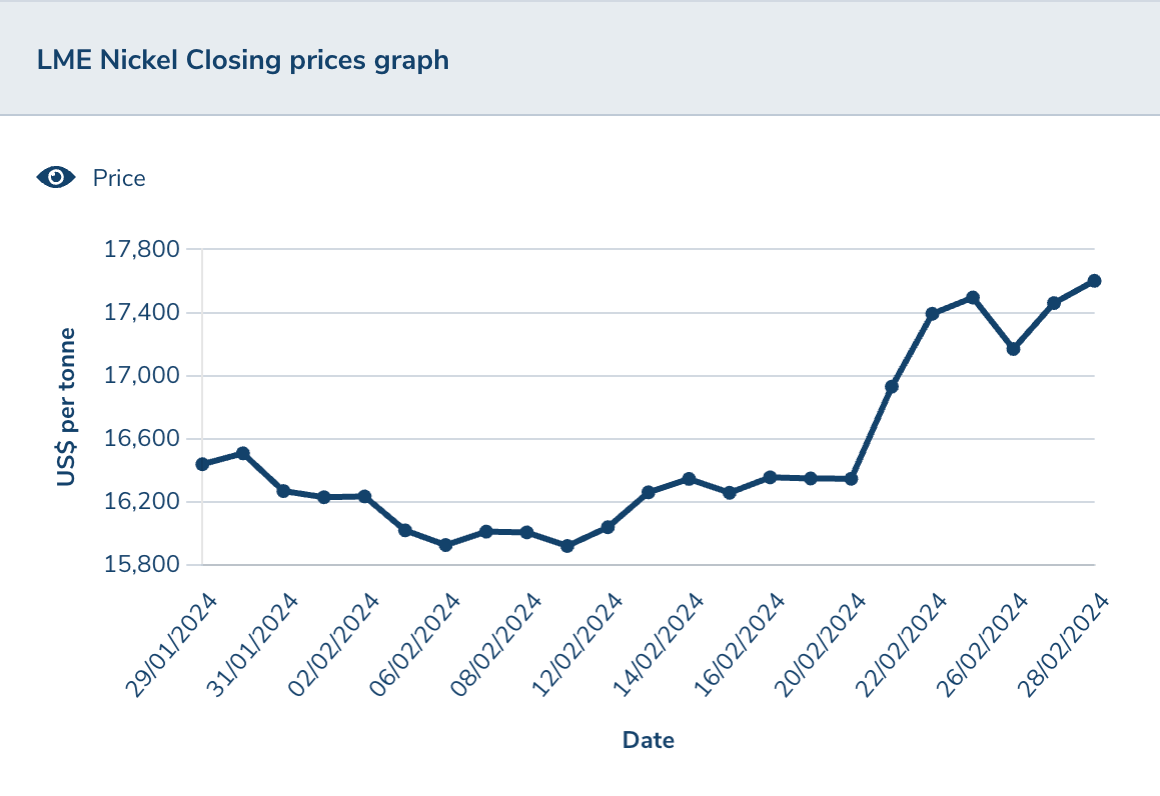

Nickel

Price: US$17,600/t

% Change: +6.62%

Well, well isn’t this a turn up for the books?

One of only two major commodities to record significant gains in February is nickel, the unloved child of the mining sector.

It has raised hopes the collapse of prices over the past year and resulting curbs to supply in Australia, China, New Caledonia and potentially Colombia could bring enough product out the market to avoid a major surplus, putting pressure on prices at current levels.

News in the sector was of course headlined by BHP’s (ASX:BHP) decision to write down its Nickel West business so hard it’s now costing the mining giant US$300 million to keep the assets on its books.

It will spend the next few months deciding whether to place the entire division on care and maintenance, risking over $3 billion of investments in a new large scale nickel and copper sulphide mine at West Musgrave on WA’s border with South Australia and a rebuild of its 52-year-old Kalgoorlie Smelter.

The issue, of course, is a flood of supply from Indonesia and technological advances that has seen its traditionally lower quality nickel pig iron output diverted through upgrading to nickel matte into the battery market, previously the domain only of established Western producers.

UP

- The Australian Government is considering a proposal from the Association of Mining and Exploration Companies that would see $1.7 billion diverted from future budgets to fund a 10% tax credit to make local battery metals refining more competitive.

- Prices rebounded in February after falling to under US$16,000/t, raising hopes that price support has been reached with BHP estimating over 50% of global nickel suppliers are losing money.

DOWN

- BHP thinks the rise of Indonesian supply will see surpluses of 5% of global demand into the 2030s.

- Indonesia’s new president Prabowo Subianto is likely to continue the protectionist nickel policies of his predecessor Joko Widodo, with a 15-year tax holiday still in place for refining operations.

Nickel miners share price today:

Coal (Newcastle 6000 kcal)

Price: US$129.50/t

% Change: +9.65%

Another big loser in 2023 and the start of 2024, thermal coal prices rebounded in February, suggesting we are around support levels for the energy commodity.

In the US$130/t range most of the larger thermal coal producers are collecting a decent margin, receiving in excess of $200/t in Australian dollar terms with little new supply to come into the market.

On the steelmaking coal side, prices for premium hard coking coal remain strong with weak relativities for pulverised coal for injection — cheaply supplied in large volumes out of Russia — an exception.

Demand for met coal assets continues to remain high, especially from non-traditional buyers as diversified miners continue to shift out of fossil fuels and towards battery and critical minerals.

South32 (ASX:S32) announced the sale of two met coal assets, with plans to collect close to a combined US$2 billion for its 50% stake in the Eagle Downs project in Queensland (sold to Stanmore (ASX:SMR)) and its Illawarra coal mines in New South Wales, which will be purchased by Indonesia’s Golden Energy and Resources and Aussie coal trader M Resources unless BlueScope Steel (ASX:BSL) exercises a pre-emptive right to buy the 5Mtpa ops.

The deals come after Whitehaven Coal (ASX:WHC) won a hotly contested bidding process for BHP’s Daunia and Blackwater mines in Queensland last year, pledging to pay up to $6.4 billion for the projects which will turn it into a predominately met coal miner.

WHC is already looking to raise additional cash by selling a minority stake in the Blackwater mine to a steelmaking partner, with India’s JSW Steel reportedly keen on a deal and demand from Japanese mills for Aussie coal also strong.

UP

- Met coal prices continue to outperform, fetching over US$300/t for much of the past 12 months.

- Heavy rainfall in January could hit coking coal supply out of Queensland, putting further strain on supplies of coal for Asian steelmakers.

DOWN

- Trading Economics says Indian coal imports could drop 3-6% in 2024 on the back of rising domestic production and solid energy inventories.

- Reuters says Asian thermal coal imports fell from record highs seen in December in January, with rises in Japan and Korea countering big drops from China and India. Columnist Clyde Russell said vessel tracking data from early last month showed the big four importers were going to see lower imports for February.

Coal miners share prices today:

Gold

Price: US$2048.50/oz

% Change: +0.01%

As the US Fed cooled hopes of early rate cuts, gold prices threatened to fall back below what is now a long standing support level of more than US$2000/oz.

But the safe haven commodity to rule them all reverted to type later in the month to end up virtually where it started give or take a few cents.

Joe Biden’s decision to hold a — probably melting — ice cream as he fielded questions about a ceasefire in Gaza last week will leave few onlookers with any optimism one is genuinely around the corner.

Instability like that obviously drives investment in gold. Hopes of rate cuts also remain high with underlying US inflation seemingly trickling down towards target levels of ~2%, falling 2.4% in the year to January.

Rate cuts are good for investments like gold because bullion does not pay interest. As rates fall the attractiveness of liquidating solid investments like gold to cash dissipates.

In the equity space investors were treated to solid financial results from a number of major gold miners, notably Northern Star Resources (ASX:NST) and Westgold (ASX:WGX), which offered a record half-year dividend and first dividend since 2021 respectively.

Regis Resources (ASX:RRL) recorded a loss and became the subject along with vendor IGO (ASX:IGO) of a $120 million claim for unpaid royalties on its 30% owned Tropicana gold mine from South32 (ASX:S32). But its results were also reflective of a broader trend for Aussie gold producers, copping a $98 million hit to retire its hedge book early in a sign miners see high prices staying in place.

M&A also evolved, with Silver Lake Resources (ASX:SLR) and Red 5 (ASX:RED) announcing a $2.2 billion merger, Horizon Minerals (ASX:HRZ) and Greenstone Resources (ASX:GSR) getting engaged in the junior space and Denver gold giant Newmont kicking off a US$2 billion process to sell a string of unwanted assets including its Telfer and Havieron projects in WA.

UP

- The World Gold Council said gold demand remained robust in China during the Lunar New Year holiday, typically a down period as Chinese workers return home for the holidays.

- Cleveland Fed President Loretta Mester said her baseline view remained that three rate cuts would come out of the US Fed this year.

DOWN

- The US economy may be stronger than people think, adding 353,000 jobs in January to beat economists’ expectations.

- That could mean a delay to rate cuts as flagged in a heavily hedged commentary from US Fed chair Jerome Powell with the sideways decision in late January.

Gold miners share prices today:

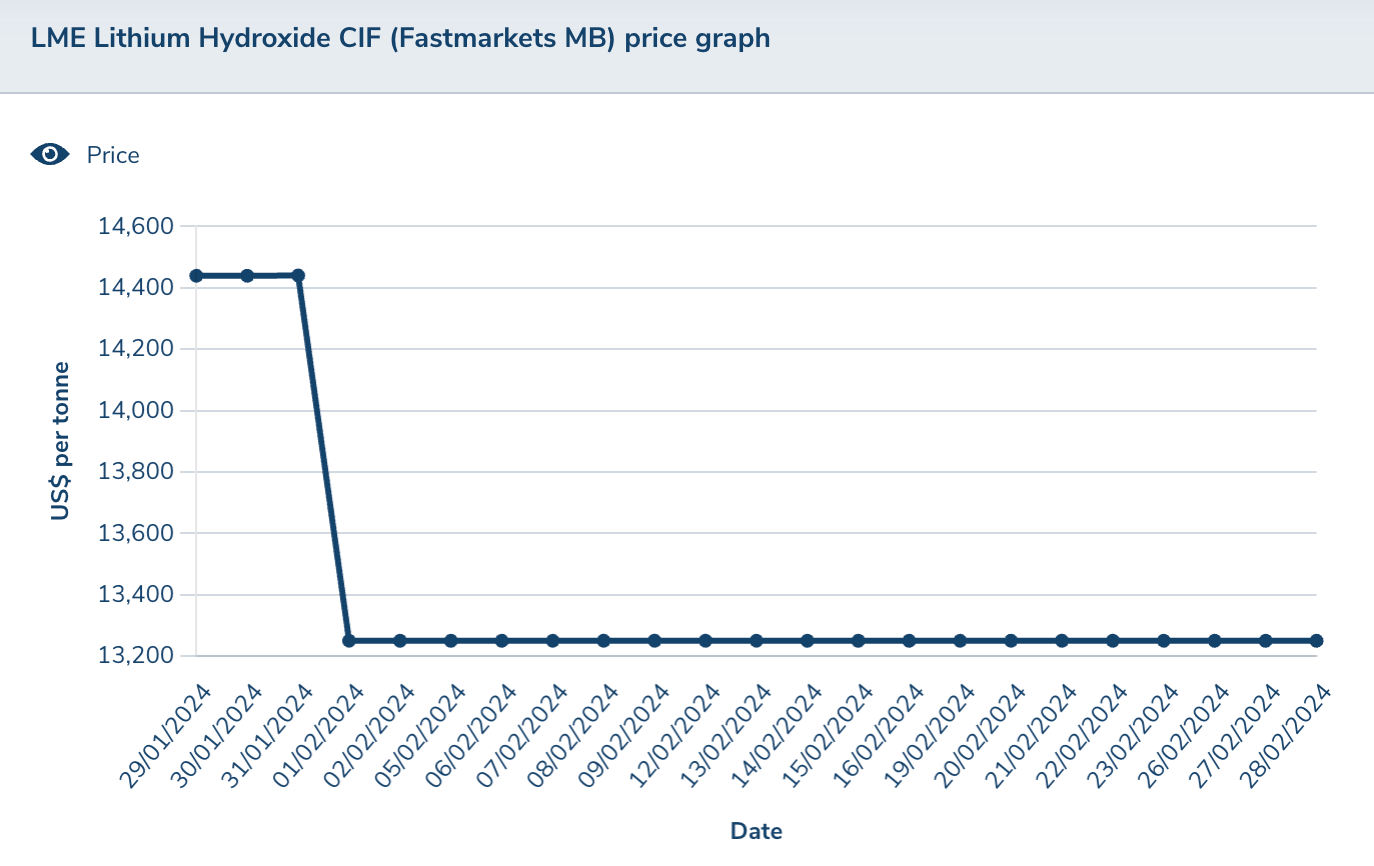

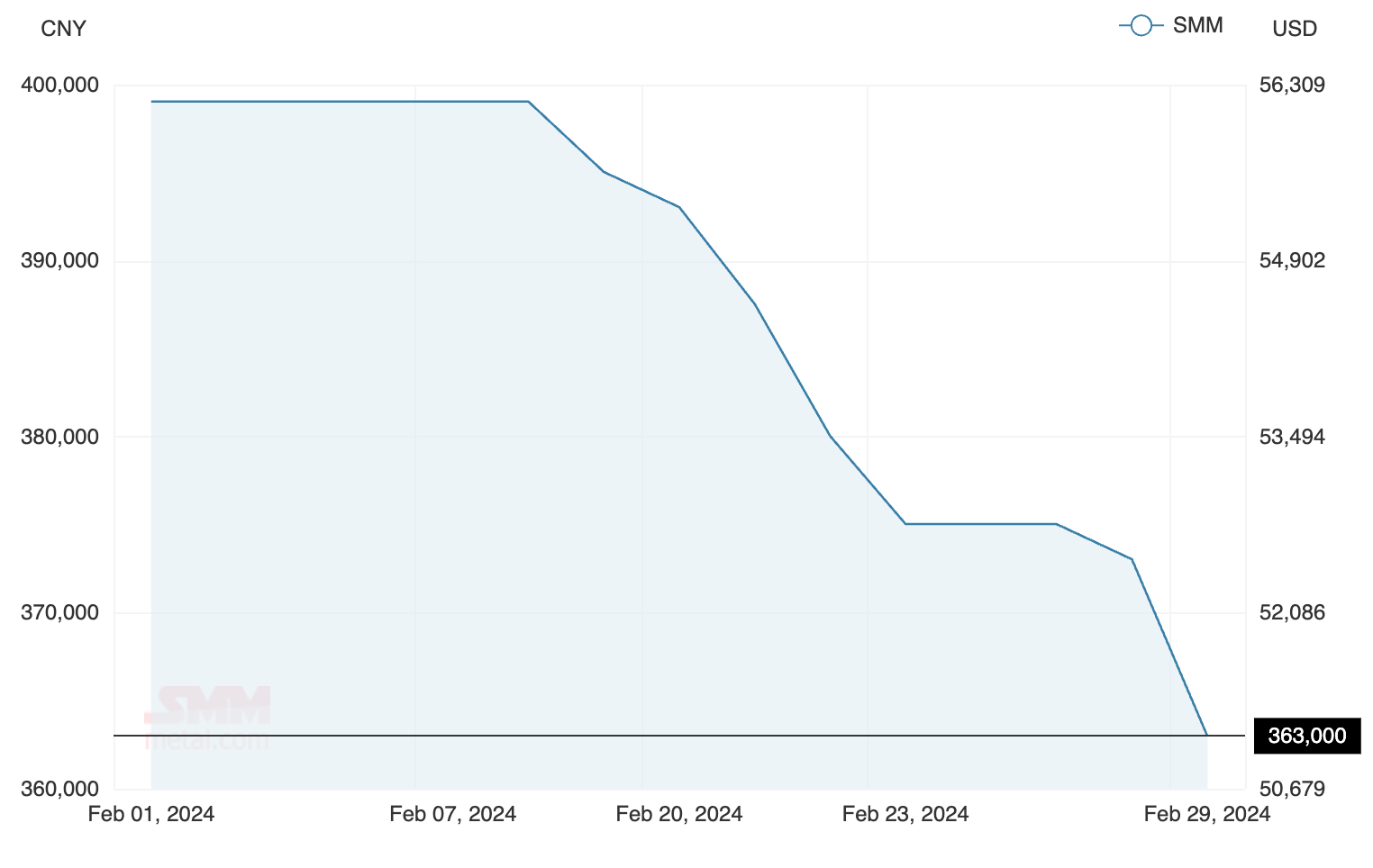

Lithium (Fastmarkets Hydroxide CIF China, Japan and Korea)

Price: US$13,250/t

% Change: Unchanged

Lithium prices, according to Fastmarkets at least, have remained effectively unchanged across February with Chinese New Year grinding purchasing activity in lithium chemicals and spodumene to a virtual halt.

It has given some producers hope that after the radical shift from seemingly endless supply shortages to a supply glut last year — despite global EV sales growth rates in excess of 30% — has reached a tipping point.

The theory would be that prices at current levels — below US$15,000/t for chemicals and US$850/t for spodumene — are unsustainable because a number of producers across the supply chain including lepidolite miners in China, smaller and higher cost hard rock miners in Australia and Canada and converters reliant on lepidolite or merchant spodumene supply are unprofitable right now.

That’s great of course for battery and EV makers, who enjoyed record low battery back per kwH costs at the end of last year. But no so good for the security of long term supply.

Already a number of projects have been curtailed. Core Lithium (ASX:CXO) halted extraction at its Finniss operation and sacked its mining contractor in a bid to trim costs.

The Greenbushes JV cut 100,000t from their ~1.5Mt guidance for FY24, MinRes (ASX:MIN) said it would not operate a recently commissioned third train at its Wodgina mine in the Pilbara and Arcadium Lithium (ASX:LTM) will trim production by ~75,000t at the Mt Cattlin mine near Ravensthorpe in WA and put back the start of production at its Sal de Vida brine in Argentina and James Bay project in Canada.

But battery metals stocks ended February on a high thanks to northwards movements in lithium futures in China — the result of concerns about environmental crackdowns at Chinese lepidolite and brine operations and the reported shutdown of a marginal mine operated by world-leading battery giant CATL.

UP

- SQM believes sale prices for lithium will remain stable for the next three months, predicting a pick up as lithium demand grows 20% this year.

- Pilbara Minerals announced a second expanded offtake with Chinese customers last month as local producers report anecdotally say interest in securing long term spodumene supply is ramping up.

DOWN

- European EV sales growth could slow with he roll off of subsidies in Germany.

- The crunch on marginal producers may not yet be over, with Sayona Mining still to complete the review of its loss making North American Lithium mine in Quebec

Lithium stocks prices today:

LOSERS

Uranium (Numerco)

Price: US$94.50/lb

% Change: -5.5%

After 10 months of solid, rolled gold gains, uranium prices finally came back to reality with a late dive taking them back under US$100/lb.

That hasn’t dulled the dreams of uranium explorers, who see a long run for the commodity amid the most ambitious new build program for nuclear power in decades.

“Globally, you’re seeing a massive shift for nuclear power where it’s got 437 nuclear power stations in operation around the world, there’s 63 getting built now. Another 111 are being planned globally,” Andrew Grove, MD of Mauritania focused uranium developer Aura Energy (ASX:AEE) told delegates at a WA Mining Club function last week.

“And above that there’s some more longer term plans, so they’re looking at doubling nuclear power production.”

That certainly sounds promising, especially with the world’s biggest miner — Kazakhstan’s Kazatomprom — announcing it will fall short of production targets in the next two years because of shortfalls in sulphuric acid supply.

But that’s been weighed down by Cameco, the west’s largest producer. The Canadian giant wants to ramp up its flagship McArthur River mine in the Athabasca Basin from 16Mlbpa to its approved capacity of 25Mlbpa “when the time is right”.

It has also flagged additional flex capacity in its network of ‘Tier 2’ assets, many of which have previously been in operation.

Cameco’s supply announcement caught the eye, but less noticed were its strong financial results. Despite missing its production guidance, Cameco more than doubled cash generation to C$688 million in 2023 on higher price realisation. That bodes well for new producers, who will likely contract at higher levels than Cameco’s legacy deals.

UP

- Lotus Resources (ASX:LOT) recently raised $30 million as it fine tunes plans to restart its Kayelekera mine in Malawi, showing the appetite in the market for uranium company financing.

- Despite long term contracting rising from 124.6 to 160.8 million lbs last year, Sprott analyst Jacob White says we have not reached replacement levels yet. Contracting peaked at 250Mlbs in the last up-cycle.

DOWN

- Miners are increasingly announcing plans to increase supply into the market, which could become an issue if any demand shock hits the market a la Fukushima.

- The recent reversion in uranium prices is a reminder sentiment can still turn sharply despite widespread positivity in the sector.

Uranium share prices today:

Copper

Price: US$8448.50/t

% Change: -1.93%

Copper prices continue to tread water despite increasing concerns over supply shortages, prompted by production failings at large miners like First Quantum Minerals and Anglo American.

Shaw and Partners became the latest analysts to ratchet up their copper forecasts.

They have lifted their 2024 outlook slightly by 0.4% to $4/lb (US$8800/t). But the firm’s 2025 and 2026 outlooks have been ramped up 10.5% and 20.3% respectively to US$4.50/lb (US$9900/t) and $5/lb (US$11,000/t) in 2025 and 2026 respectively.

Long term real prices (based on 2024 money) are up 10.7% to US$4.26/lb (US$9372/t).

Steve Schoftstall, Sprott’s director of ETF product management, said that despite weaker historical prices copper M&A had overtaken gold.

“M&A activity in the copper sector has recently overtaken that in gold, with several companies receiving premiums of over 20%,” he said in a note.

“This reflects the strength and positive outlook of the copper mining industry. As a long-valued asset, copper is entering a new era with the global energy transition.

“The demand for copper in energy grids, electric vehicles and clean energy technologies, combined with diminishing ore grades and limited inventories, underscores its growing importance and potential for price support. Copper miners may likely be positioned to benefit from these developments.”

Copper prices peaked at over US$10,700/t in May 2021.

UP

- Copper treatment and refining charges in Asia have hit levels many observers say they’ve never seen, with Chinese processors desperate for tight raw material supply after a massive build out of refining capacity.

- LME copper stocks have been drawn down significantly in 2024 so far, falling from 165,700t at the start of the year to 121,375t on February 29, around 1.7 days of global demand.

DOWN

- Poor factory activity in China has seen warehousing the commodity rise 500% year to date to 181,323t as of February 23.

- Continued weakness in the global economy and China is keeping copper — heavily driven by macroeconomic sentiment, from reflecting fundamental supply-demand metrics.

Copper miners share prices today:

Iron ore (SGX Futures)

Price: US$115.18/t

% Change: -14.85%

An unimpressive return from the Lunar New Year holiday for the Chinese steel sector saw iron ore fall from its long run above US$130/t in February.

Prices remain solid for large producers, whose costs sit around the US$20/t range. All of them are still looking to ramp up output aside from Vale, which has moved from a return to 400Mtpa stance to a quality over quantity mantra.

Its latest move is a deal to take a 15% stake in Anglo’s 26Mtpa Minas-Rio operation, which has the potential to supply high grade pellet feed for lower emissions direct reduced iron steelmaking.

The deal will unlock the development of Vale’s adjacent Serpentina deposit down the line.

The Aussies are all still making strong profits at their iron ore operations in the current price environment. Fortescue’s (ASX:FMG) 41% lift in profits and 44% rise in interim dividend payments were a standout, even if questions continue to mount on its green energy diversification.

UP

- Australia’s big three iron ore miners will pay over $15 billion in dividends in a sign profitability in the sector remains high.

- China is still emerging from the Lunar New Year slowdown, a period often followed by peak construction season.

DOWN

- Steel mills are sitting on higher inventory levels amid weak downstream demand.

- The ability of steelmakers to maintain production levels seen in 2023 could again hinge on export demand if the upcoming two sessions policy meetings fail to lead to domestic stimulus.

Iron ore miners share prices today:

Rare Earths (NdPr Oxide)

Price: US$51.10/kg

% Change: -9.02%

Despite calls for the market’s rebound rare earths prices continue to falter amid still rising Chinese production quotas, which have come in earlier than expected in 2024 after a shock third quota was issued last year.

It has some local miners looking to link up with China to get off the ground, with locally listed Hastings (ASX:HAS) notably announcing an offtake deal that would see it toll treat material with Baotou in the Middle Kingdom.

There are moves afoot to try consolidate the market outside China, with Lynas (ASX:LYC) and major US producer MP Materials reportedly holding secret but failed talks about a tie-up.

At current prices there’s little doubt new developments will be challenged, but we’ve also been here before.

It remains to be seen what role the Government will play there. Iluka Resources’ (ASX:ILU) Eneabba refinery will be a test case. Its budget has blown out by up to 50% to US$1.7-1.8 billion, meaning it will need more support from Aussie taxpayers to get up and running and supplement a landmark $1.25 billion low cost loan issued through Canberra’s Critical Minerals Facility in 2022.

UP

- Rare earths prices are verging on levels where even Chinese producers are struggling to turn profits, raising the prospect price support could be hit soon.

- Lynas Rare Earths remains a buy for a number of brokers, with Goldman Sachs saying while medium term demand is balanced, long term deficits are still likely for rare earths.

DOWN

- Rare earths quotas of 135,000t of mined and 127,000t of refined metal in the first half have been issued in China — up on last year’s initial levels but a slower growth rate than 2023

- Chinese rare earths imports rose 45% last year, creating an oversupply situation alongside higher quotas which saw major China Northern Rare Earths announce lower profits and forecast pricing.

Rare Earths share prices today:

OTHER METALS

Prices correct as of February 29, 2023.

Silver: US$22.34/oz (-3.25%)

Tin: US$26,556/t (+1.23%)

Zinc: US$2414.50/t (-4.47%)

Cobalt $US28,550/t (-2.00%)

Aluminium: $2190.50/t (-3.93%)

Lead: US$2083/t (-3.50%)

Graphite (Fastmarkets flake) US$524/t (0.00%)

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.