The energy transition helped copper and lithium soar in 2021. Will commodities be more predictable in 2022?

Pic: Getty

The markets for key energy transition metals will remain tight into 2022 as market watchers upgrade their forecasts to account for the momentum behind the commodities.

But analysts for pricing agency Fastmarkets say metals for the electrification and decarbonisation narrative – aluminium, copper, lithium, cobalt, nickel and graphite – will be less volatile than 2021, when supply shortages and Covid-19 impacts caused massive price spikes.

“The energy transition – combined with the disruptive effects of Covid-19, a bump in the road for the commodity supercycle and, in the second half of the year, the signs of a coming period of stagflation – made for an interesting year, with record-breaking levels of volatility and record-high prices,” they said.

“In 2022, the energy transition is even higher up the agenda for governments, investors and corporates alike.

“Copper, aluminium and battery raw materials will be needed in ever greater quantities to build the electric vehicles (EV), batteries and power grids of the future.

“Despite growing demand from EVs in particular, we expect 2022 to be a smoother year, as the global economy continues to put distance between itself and the most acute period of the Covid-19 pandemic.”

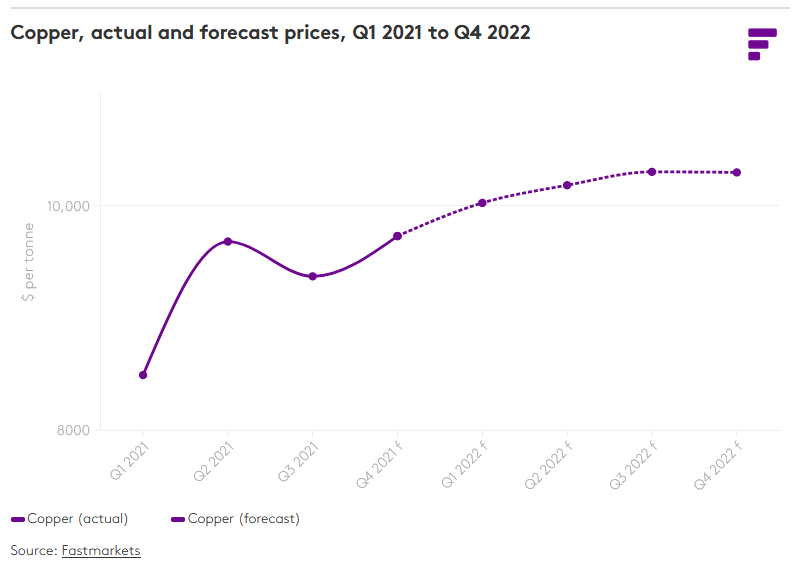

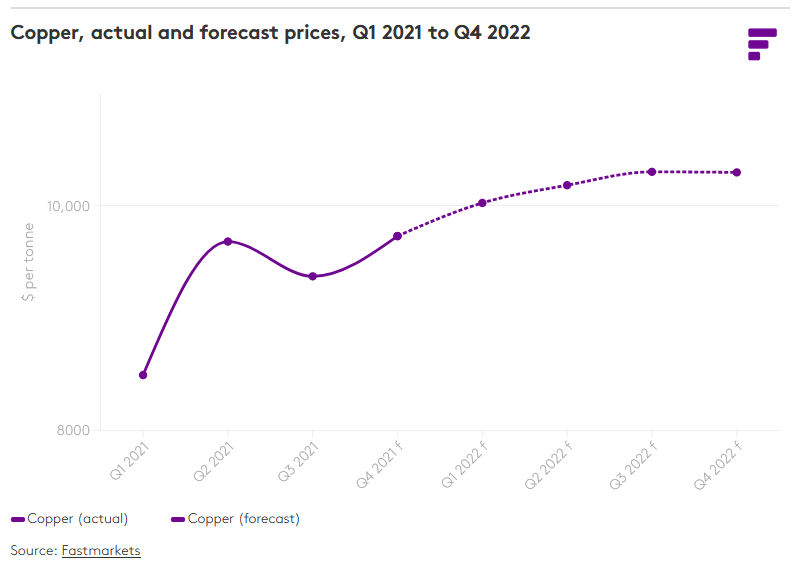

Copper market deficit to continue in 2022

Fastmarkets is forecasting copper prices to rise steadily to above US$10,000/t as it predicts a deficit will remain in 2022 despite expectations mined production will increase by 7% next year.

“Total world copper mine production growth could surge to 7% in 2022 from just 2% in 2021. Such strong growth will bring the global concentrate market back to balance in 2022 after two deep deficit years,” analysts said.

“However, we expect a higher rate of supply disruptions next year given so much new and expanded capacity due to come online or ramp up.

“We expect a bigger deficit of refined copper of 571,000 tonnes for 2021 as a whole, assuming 2.2% growth in refined output and 2.5% growth in refined usage. We also expect the refined market to remain in a deficit in 2022.”

Copper prices soared to all time highs of around US$10,700/t in May as supply shocks hit and Goldman Sachs branded the commodity “the new oil” thanks to its role as a driving force behind the electrification of energy.

It pulled back before again rising to around all time highs in October as copper stores on the LME hit their lowest level since 1974. Despite the emergence of the Omicron coronavirus variant as a handbrake on growth, Fastmarkets remains bullish on the outlook for the red metal.

“Even though the Omicron variant constitutes a potential bearish risk to our overall copper outlook, we continue to think that the bull market is not over yet. The consolidation from May was necessary after prices rose too fast and too hard. Sentiment is now in check and positioning is clean.

“Consequently, we have a bullish price outlook for the rest of 2021 and going into 2022.”

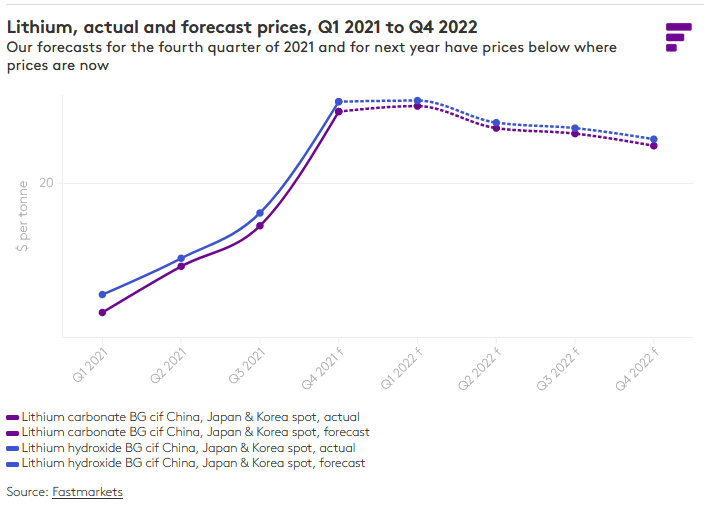

Will lithium consumers be happy to chase higher prices?

Lithium prices have gone from the lowest of the lows to the highest of the highs in the space of a year, with spodumene concentrate rising by over 300% and downstream carbonate and hydroxide chemicals for battery and EV makers also at record levels.

Fastmarkets has questioned whether consumers of lithium products will be happy to keep chasing higher prices, but says supply will still be slow to catch up to demand.

“We expect the lithium market to remain tight for the rest of 2021, because of price performance, stronger-than-expected demand growth and the slow return of idle production capacity,” they said.

“We expect additional supply to relieve the present tightness as 2022 unfolds.”

No more clear has the yawning gap between supply and demand been seen than in the rising prices for spot spodumene cargoes traded in Pilbara Minerals’ (ASX:PLS) online Battery Material Exchange auctions.

“For now, it appears as though the tightness will last well into the new year – the level of destocking by downstream processors, convertors, consumers and hoarders will determine whether prices hold at these levels, drift lower or push higher still.

“Apparent demand is expected to be stronger than actual demand – the supply chain will likely want to restock after this expected period of destocking and expanding downstream capacity will need to carry ever larger amounts of working stock.

“After a brief consolidation, the fact prices are on the rise again suggests consumers have decided they cannot afford to destock too much, with some prepared to chase prices higher in order to keep inventories topped up.

“However, given the already massive price gains in 2021, we expect consumers to be increasingly reluctant to chase prices higher and higher.”

Nickel, graphite still look bullish, aluminium elevated, but cobalt to face pressure

Fastmarkets views recent price weakness for nickel, related to Tsingshan’s promise to supply nickel matte from laterites in Indonesia to the battery market, “as a healthy correction within an ongoing bull market”.

“Nickel’s performance in the past month supports that thesis,” they said.

“While China’s economy may put the brakes on somewhat in the face of macro headwinds, history shows that the government is quick to resolve problems and preserve growth.

“Meanwhile, the rest of the world still looks structurally bullish – demand is robust, infrastructure projects are under way, electrification is accelerating, shipping congestion and supply disruptions are affecting availability, stock levels are low, and central banks seem to be in no hurry to raise interest rates.

“This picture gives us confidence to maintain a bullish bias in our price forecasts and gives traders the confidence to continue their buy-the-dip strategy.”

With the recent energy crisis easing, aluminium prices have also corrected as smelters put out of commission due to high coal prices have come back online.

Fastmarkets sees a period of consolidation but says it is bullish despite the fourth quarter dip.

Cobalt prices rose for 100 consecutive days in the latter half of the year, recalling the madness of 2018’s charge towards US$100,000/t.

They did not scale those heights this year, but still charged to more than US$70,000/t in December.

The upward run of @Fastmarkets‘ #Cobalt metal price now extends an astonishing 100 days in total, with the last downward daily step seen on Aug 31! pic.twitter.com/E4qeH1koSE

— Peter Hannah (@PHmetals) December 9, 2021

Fastmarkets expects prices to taper with semiconductor shortages and the transition in China from EVs with NCM batteries to LFP chemistries (which have less range but are more economical because of the substitution of the expensive cobalt and nickel).

“With greater interest in LFP battery chemistries and with EV sales still potentially likely to suffer from the semiconductor shortage, we would not be surprised if the current rise in cobalt prices is limited and if prices fall back again as the fourth quarter of 2021 progresses,” analysts said.

“We think prices are near their peak as we expect production increases in 2022, combined with weaker than expected demand from consumer electrics, due to semiconductor shortages, plus the surge in LFP demand, to weigh on prices.”

Graphite prices have been stable in 2021 and surged in recent weeks because of supply shocks, shipping delays and stronger than expected demand from EV batteries.

“We maintain the view that both flake and spherical graphite prices will trend stable to higher in the near term,” Fastmarkets’ analysts noted. Graphite is shielded from the NCM v LFP competition because it is used as an anode in both.

UBS cautious on iron ore and met coal, bullish on nickel and battery raw materials

UBS analysts meanwhile see commodities trading lower across the board in 2022 on expectations of falling property activity in China, which has been managing the Evergrande crisis in what has been described as a controlled implosion.

“Commodity prices looks set to trade lower into 2022 as supply growth outweighs demand growth,” analysts led by Lachlan Shaw wrote.

“China’s property activity will likely fall in 2022, while rest of world goods demand slows as services growth accelerates.

“Recent policy easing in China aims to moderate recent ~20%-30% y/y falls in property activity (which is one-quarter of GDP), rather than the start of a cyclical expansion in property construction.

“Supply should lift as winter and power shutdowns ease into mid-2022 and as industry catches up on new capacity development post-Covid

disruptions.

“Prices rarely lift sustainably with such fundamentals, and we expect key commodities, including iron ore, met coal, copper and nickel, to trade down and closer to cost support in 2022.”

UBS said recently policy easing is a “‘False Dawn’ rather than a ‘New Dawn'”.

“Recent policy easing by Chinese authorities is about slowing the pace of property retrenchment, and is consistent with weaker commodity demand and prices into 2022,” Shaw and Co. wrote.

However, UBS, which has bearish below consensus forecasts of US$85/t for iron ore and US$154/t for met coal, is becoming more bullish on energy transition metals nickel and copper.

It has updated its long term price forecasts for copper from US$3/lb to US$3.50/lb and for nickel from US$6/lb to US$8/lb.

“Our top-of-the-street EV penetration view (UBS estimates close to one in two new cars sold by 2030 will be an EV) cascade into our

demand assumptions for nickel, lithium, graphite and the other battery commodities,” Shaw said.

“While this will impact each commodity differently, our headline demand forecasts generally have us top of consensus with regard to our price outlook.”

Among the big Australian miners UBS says ultra-diversified South32 (ASX:S32) and beaten down goldie Northern Star (ASX:NST) as its top picks, with BHP (ASX:BHP), Evolution (ASX:EVN) and OZ Minerals (ASX:OZL) neutral.

It has a buy on Newcrest (ASX:NCM) and buys on the iron ore heavy Rio Tinto (ASX:RIO) and Fortescue Metals Group (ASX:FMG).

UBS picks share prices today:

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.