Sustainable steel-making might be a way off but this is what the transition could look like

Pic: Schroptschop / E+ via Getty Images

Interest in green steel is growing. It was high on the agenda at COP26 and Australia has already flagged low emissions steel as a key step in our net zero by 2050 plan.

The US and EU have agreed to address and lower the carbon intensity of the steel and aluminium industries.

Last month, South Korean steel-making giant POSCO said it was considering Australia as a ‘regional strategic base’ for its green steel and hydrogen projects, and has already signed a hydrogen partnership deal with Origin Energy (ASX:ORG).

And this week green steel tech pioneer Professor Veena Sahajwalla was named NSW Australian of the yearfor her invention of Polymer Injection Technology, or ‘Green Steel’.

Magnetite Mines (ASX:MGT) non-executive director Mark Eames says the increased interest in green steel has grown because the industry generates around 8% of global carbon emissions.

“In the last 12 months, people have started looking at ways to produce low emission steel and the reality is there isn’t an obvious steel-making technology, which is commercial, and in use anywhere in the world today, that can make zero emission steel,” he said.

“So, we’re really at the start of what’s going to be quite a long journey.”

Hydrogen for more sustainable steel-making

Hydrogen is definitely looking like the popular option.

Rio Tinto (ASX:RIO) joined forces with BlueScope Steel (ASX:BSL) to investigate the production of low-emissions iron feed using hydrogen last month.

Fortsecue’s (ASX:FMG) Future Industries is working to create Australia’s first green steel project and also last month GFG Alliance announced plans with Santos (ASX:STO) around a new green hydrogen production facility, electric arc furnace (EAF) and direct reduced iron (DRI) plant to transform its Whyalla steelworks in South Australia.

“Basically, they’re taking an existing blast furnace, which is coke-based, and then they’re injecting some hydrogen in the bottom and that reduces some of the fuel from other carbon-based fuels, so it does help reduce the emissions but only a little bit,” Eames said.

“There’s going to be a number of technologies like that around optimisation, that are going to gradually reduce emissions by 10, or 20, or 30%.

“Optimisation is the first step, and then we’re going to have to find ways of making steel without generating emissions.

“It could be that you have a fully hydrogen-based steel making process, and probably the top contender for that is using hydrogen in a direct reduced iron plant instead of gas.”

“There is no way around hydrogen,” says Markus Krebber, CEO of @RWE_AG, adding that green #hydrogen is the only technology able to “decarbonise those industries which cannot electrify like steel, but also some parts of the chemical industry”. https://t.co/bG1XbBwjP3

— ITM Power Plc (@ITMPowerPlc) November 17, 2021

But hydrogen is expensive

But Eames says hydrogen is quite expensive and that as a result steel is going to become a lot more expensive. CRU research manager Paul Butterworth agrees.

“CCS is expensive, is not universally applicable and could only capture a proportion of emissions from a traditional integrated plant if costs are to be contained,” Butterworth said.

“But hydrogen is expensive. Even at $2/kg, which is an aspiration (and difficult to achieve in my view).

“Hydrogen price is ~$17/GJ (lower heating value), whereas metallurgical coal today is ~$5/GJ. So, the main reductant in the process would be at least 3x higher cost and probably more.”

More high-grade iron ore needed

So, what kind of iron ore will be needed as the world looks to produce sustainable steel?

Eames says there’s a growing consensus in the industry that higher grade ores are needed to make lower emission steel, which is exactly what it aims to produce from its Razorback project in South Australia.

“People are realising that regardless of whether we use carbon in the form of coal or gas to reduce the iron – or whether we use hydrogen – essentially to reduce emissions, the iron ore used needs to move to higher grades,” he said.

“And the problem with that is the industry has been moving to lower grades.

“The average grade of ore out of places like Australia and Brazil has been declining over the past 20 years, largely because the higher-grade deposits are being exhausted.”

Butterworth said that generally higher-grade ores require less energy to process, but some of the process routes being proposed – such as the use of a smelter where the quality of DRI being melted is less of an issue – means that lower grade ores should be applicable.

“However, the higher the grade the better, so beneficiation is likely to expand and this would be favourable for iron ore resources that are more amenable to beneficiation,” he said.

Blast furnace optimisation could be part of the transition

Eames says there’s a 15–20-year period where radical progress needs to be made.

And he’s not alone in this prediction. Last month Fastmarkets index manager Peter Hannah told Stockhead’s Josh Chiat that the steel industry actually produces more carbon dioxide than it produces steel at the moment.

“So, to bring that down and actually meet the decarbonisation targets, first of all, you’re going to need a period of optimisation of the existing blast furnace technology, where the blast furnace is going to need to consume more higher grade product,” Hannah said.

“And then eventually, in maybe a few decades, you will see a big shift towards direct reduction, which absolutely requires material of very high grade.”

“However, Li expected that demand for high-grade iron ore will gradually increase with intensifying environmental curbs, low-carbon requirement and more blast furnaces at mills.” #ironore #grade #steel #steelmaking @ReutersCommodshttps://t.co/pbgP3utuiR

— MagnetiteMines (@MagnetiteMines) November 14, 2021

Low emission steel is going to cost more

While blast furnace optimisation does not provide a net zero solution, Butterworth said it will be part of the transition.

“The technologies currently being proposed for decarbonisation of steel are known, and we could probably start to build low emission steel mills tomorrow if we really wanted to,” he said.

“The problem is the cost. Low emission steel will cost more, and so steel prices need to be higher to encourage the investment.

“We estimate that a carbon price of ~$230/tCO2 is needed to lift the cost of traditional technology sufficiently to make investment on low emission technology viable.

“This implies lifting costs by ~$450/t steel.”

So what does the future hold for steelmaking?

Looking ahead to next year, Butterworth said he suspects we will see further announcements by steel mills regarding exploratory investments in green steel developments (electrolysers, DRI plants etc), as well as announcements of further collaborations between mills and or miners.

“Our current view is that the carbon price in Europe is not expected to rise significantly next year, but a little further out it should start lifting as the market for EUA tightens,” he said.

“When this happens, this should start to stimulate further moves in Europe.”

But he said that the transition would take decades given the investment required and the need to build out low carbon electricity to produce hydrogen.

“Traditional steel-making will need to exist side by side with low carbon,” he said.

“The world cannot have a fully low carbon steel sector today, or even in the next decade; it is just not possible from an investment, infrastructure perspective.

“My calculation suggests that the European integrated sector (~95 Mt production), which represents ~$50 billion in plant, property and equipment assets, would need to invest ~$100 billion in new hydrogen-based equipment, but a further $230 billion would be needed to be invested in renewable energy and further investment would be needed in integration, grid strengthening etc.

“It is a massive ask and will not happen soon, and certainly not without either a higher carbon price, much higher fossil fuel costs or subsidy.”

Razorback could cater for demand

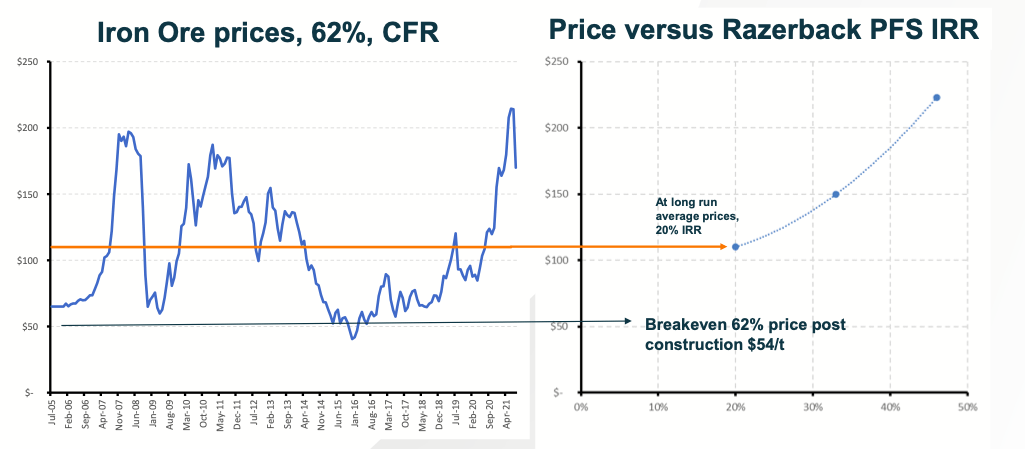

Eames said that the Razorback project will be among the world’s highest-grade producers, producing around 3Mtpa of a 68% concentrate grade – and is expected to garner a substantial premium over the benchmark 62% fines price.

“Some observers say that that means that the whole iron ore industry is going to have to shift from lower grade ore bodies, where essentially you dig and ship the material without much processing, to higher grade products which are going to require heavily processed iron ores,” he said.

“And that’s exactly what Magnetite Mines is seeking to do. We’re seeking take a low grade in situ ore body and use magnetic separation technology to create a very high-grade product.”

Eames said there’s going to be a big shortage of high-grade ores and surplus of low-grade ores if we’re going to produce sustainable, low-emissions steel, which he expects over time would increase demand – and the price.

“We completed a pre-feasibility study in early July, that demonstrated that the project was attractive at long run iron ore prices and gave us the confidence to move into the definitive feasibility study phase which is well underway now,” he said.

Renewable power adds to ESG credentials

The company plans to tap into South Australia’s renewable energy grid, which is currently 60% powered by wind and solar – a figure only likely to grow by the time Razorback is expected to produce iron ore in 2024.

And just this week MGT submitted a formal application to ElectraNet for a proposed 132 kilovolt (kV) transmission line to be built from Robertstown to the project site.

“We’ve got some particular advantages at Magnetite Mines, because not only are we aiming to produce a high-grade product, but we’re planning to use electricity from the Southeast Australian grid and from the South Australian part of that grid,” Eames said.

“We think the combination of a high-grade product, combined with a higher renewables component in our energy supply is going to give us attractive ESG credentials.

At Stockhead we tell it like it is. While Magnetite Mines is a Stockhead advertiser, it did not sponsor this article.

Related Topics

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.