Sub-par supply is driving magnetite prices up. Which ASX small caps are killing it with their iron game?

There's a bunch of ASX juniors getting loft with their small irons to meet our energy requirements. Via Getty Images.

- High-grade magnetite is intrinsic to our clean energy transition

- The material is key to lowering CO2 levels at the industrial level

- Cyclone Metals has a giant of a magnetite deposit up in Canada

A few little birdies on the back 9 a while ago told this Stockhead that stable, almost institutional hematite supply, largely from WA’s Pilbara region, would eventually have to make some space for magnetite ores that can be processed into higher grades – vital to cleaner smelting processes in steelmaking.

Responsible for ~8% of the world’s CO2 emissions, the majority of steel production is still coal-based and commonly relies on low-grade hematite iron ore somewhere between the 55-62 percentile range.

It’s the +65% Fe grades that are required to reduce carbon emissions, and they come from magnetite deposits that can be processed into pellets and utilised in direct reduced iron (DRI) manufactured by using natural gas (and hopefully soon to be) hydrogen to extract the oxygen from high-quality ores.

Rightly or wrongly, the skeptics are still present when it comes to utilising higher-capex magnetite in steel production.

“The transition away from coal-based steel-making is a reality, but it will take some time and there remain significant uncertainties,” Rio’s head of steel decarbonisation Simon Farry told Bloomberg earlier this week.

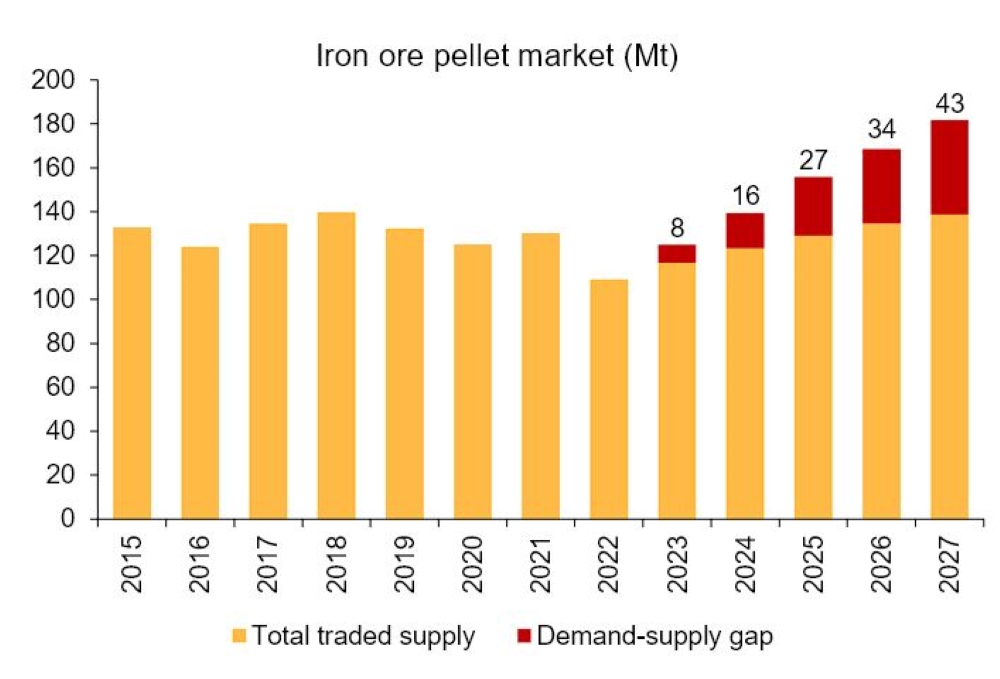

However, that clock is ticking and demand for high-grade ore is on a significant upward trend.

Wood Mackenzie anticipates the deficit in high-grade iron ore supply could reach up to 200Mtpa by 2050. To put this into perspective, that’s about one-fifth of China’s current annual iron ore imports.

The prevailing wisdom within the sector is that magnetite concentrates have now become more economically attractive, driven by an escalating imposition of CO2 taxes and inherently elevated energy costs due to ongoing market and geopolitical machinations.

Yes, they require more capex, making them a less preferred option in the short term, but that’s all changing though as we transition into our greener, cleaner world.

China, Europe and the US are all pushing the envelope for high-grade Fe pellets as we transition to lower carbon-emitting industrial practices.

“The return of European blast furnace capacity in 2023 (13Mt announced so far) along with improving Chinese demand amid sintering restrictions in some parts of the country back our view that pellet premiums have bottomed and are likely to rise this year,” say Macquarie analysts.

“Aside from FMG’s Iron Bridge project which will produce high grade (67% Fe) iron ore suitable for pelletising, which is scheduled to come online this quarter, there are few relatively advanced pellet feed projects globally.”

Recently, however, FMG downsized its production forecast from 7Mtpa to 5Mtpa, opening the gap wider for entrants to the market.

Buoyant Chinese consumption

China is bucking the forecasts by keeping its iron ore imports steady and even improving on monthly shipments compared to the same time last year, say analysts at Fitch, citing that Fe stockpiles are weaker in the Middle Kingdom than previously predicted.

“During January to August of 2023, mainland Chinese imports of iron ore surged by 7.4% y-o-y to a record high of 775.7Mt. Total iron ore inventory at mainland Chinese ports as of September 15 were 11.4kt, compared to 13.4kt on January 6 2023,” Fitch says.

“Despite mainland China’s uneven economic growth and a still failing property sector, blast furnace steel production and thus iron ore demand have shown a defiance of all odds, through support from non-property sectors including shipping, machinery, automakers and infrastructure.

“From January to August 2023, China produced 712.93mt of crude steel, up 2.6% from the same period in 2022. We expect some more upside to iron ore prices in Q4 2023 ahead of the winter holidays as steel mills continue restocking.”

Favourable sentiment in the futures market is bolstering iron ore prices in both Singapore and China’s Dalian exchange. Fitch remains optimistic about the potential for the Chinese stimulus to reignite activity in the property sector.

The green steel push and Chinese consumption is increasing demand long term and that momentum has spurred the Australian iron ore sector to engage proactively in the emerging high-quality iron ore market, with a focus on magnetite both domestically and abroad.

Stronger for longer

Here’s a few ASX small caps that are looking to chip into the more carbon-friendly steelmaking supply chain:

Cyclone Metals’ (ASX:CLE) Block 103 magnetite project in Canada can produce 69.5% Fe concentrate, and at a whopping 7.2 BILLION tonnes, is a monstrous undeveloped magnetite resource.

The project is nestled in the Labrador Trough, one of the largest iron ore belts in the world which hosts 99% of Canada’s iron ore production and the only one which benefits from open access rail and port infrastructure.

Extensive metallurgical testwork has been conducted by the company, recently demonstrating a capability to produce high-quality Fe magnetite concentrate.

In September, CLE embarked on an extensive program of comprehensive metallurgical testing using bulk sediment samples, aimed at demonstrating the seamless production of a premium 69.5% Fe magnetite concentrate.

The company is confident that it can showcase its magnetite concentrate to steel clients as soon as next year.

CLE says there’s also early indications that direct shipping ores (DSO) could exist at Block 103 as it’s adjacent to Tata Steel’s own 2Mtpa DSO operation.

“Exploration activities are planned for Q2 2024 to identify and quantify this opportunity, which could deliver early cash flows for a modest capex outlay,” the company said.

In South Australia, Magnetite Mines (ASX:MGT) is looking to bump into global DRI demand with its Razorback project that’s gathering steam.

The company says it’s receiving increasing interest from steelmakers, commodity traders and private equity groups to form a JV for the development of the project where it plans to produce 68.5% DR-grade iron ore.

MGT aims to produce 5Mtpa from its 6 billion tonne iron ore project and recently rattled the tin for $6.2m to finalise its mining lease proposal with the state government as well as support the completion of engineering work and other capital costs.

Iron Road (ASX:IRD) is looking at developing a 12Mtpa magnetite project at its Central Eyre Iron project – also in South Australia – where a proposed green hydrogen and ammonia development at nearby Cape Hardy could potentially complement production.

Meanwhile, Hawsons Iron (ASX:HIO) is in pursuit of magnetite in WA, with Stage 2 exploration analysis showing prospective, near-surface magnetite mineralisation at its namesake project.

Also in WA, Creasy-backed CZR Resources (ASX:CZR) has found potential for its 450-880Mt Ashburton magnetite project. An 11km-long, outcropping magnetite schist only 20km from its Robe Mesa flagship.

A recent review resulted in an exploration target of 450Mt – 880Mt at 24-30% Fe, generating a magnetite concentrate of 65-68% Fe at a 25-30% mass yield.

CLE, CZR, IRD, HIO, MGT share price charts

At Stockhead we tell it like it is. While Cyclone Metals is a Stockhead advertiser, they did not sponsor this article.

Related Topics

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.