Resources Top 5: Cheap gold stocks have their moment in the sun, Solis soars 170% on Brazil lithium buy

Pic: Via getty

- Dual listed Solis Minerals 170% and counting since announcing purchase of the Jaguar lithium project in Brazil

- $15m capped, 3.1Moz gold stock Toubani Resources says it is undervalued compared to peers

- Impact Minerals defines large 10km long, 2km wide rare earths soil anomaly

Here are the biggest small cap resources winners in early trade, Thursday June 1.

SOLIS MINERALS (ASX:SLM) (TSX.V: SLMN)

(Up on no news)

Dual listed SLM is up 170% and counting since announcing the purchase of the Jaguar lithium project in Brazil yesterday.

At Jaguar – located in Bahia state — the company says there are rock chips grading up to 4.95% Li2O along a 1km long, 50m wide spodumene-rich pegmatite body.

Drilling will kick off this month.

“Brazil is fast becoming a significant player in the hard rock lithium space,” former Delta Lithium (ASX:DLI) boss and current SLM exec director Matt Boyes says.

“Solis’s primary objective is to quickly position itself by acquiring highly prospective underexplored projects in the northeast of Brazil.

“The Jaguar pegmatite hosts confirm LCT-bearing pegmatites with some of the coarsest and most abundant spodumene occurrences I have seen.

“These tenements in what may be a new lithium province are a fantastic addition to our already large tenement position in the northeast of Brazil, and with drilling to commence immediately.”

Big buddy and major shareholder Latin Resources (ASX:LRS) will provide “exploration guidance and country experience”, SLM says.

LRS is currently drilling to expand the size of its 13.3Mt @ 1.2% Li2O inventory at the Salinas project in Minas Gerais, Brazil.

SLM is up 350% year-to-date. It had ~$1.8m in the bank at the end of March.

TITAN MINERALS (ASX:TTM)

(Up on no news)

TTM has three main copper-gold projects in mineral rich Southern Ecuador: Dynasty, Linderos and Copper Duke.

The current focus is ‘Dynasty’, a large, high grade ~2.1moz and growing gold project, which also contains 16.8Moz of silver.

The mineralisation at Dynasty – which runs +9km long and +1km wide — remains open in all directions says TTM.

In April, drilling at the Cerro Verde, Kaliman and Brecha-Comanche prospects kicked off.

TTM says significant epithermal gold and porphyry gold-copper mineralisation across all three prospects remains open both laterally and at depth.

The $70m capped stock is down 30% year-to-date. It had US$2.3m in the bank at the end of March.

POLARX (ASX:PXX)

(Up on no news)

The Northern Star (ASX:NST)-backed elephant hunter has two flagship assets: the Humboldt Range gold-silver project in Nevada, and the Alaska Range copper-gold project in south-central Alaska.

The junior soared after scoring one of the biggest gold hits of 2022 at Humboldt Range’s Star Canyon prospect, which is just ~3km from the currently operating 5Moz Florida Canyon mine.

Some less than stellar follow-up drilling results announced in February saw the share price fall just as fast.

An IP survey kicked off late May across the nearby Fourth of July and Black Canyon prospects, which will take 10 weeks to complete.

IP surveys can detect changes in electric currents caused by different rocks and minerals beneath the surface and are often used by explorers to dial in on drilling targets.

“The regionally low-grade gold mineralisation encountered to date by PolarX is hosted in similar geology to the nearby Rochester Mine (400Moz Ag, 3Moz Au) and neighbouring Spring Valley project (4.1Moz Au),” it says.

“The Spring Valley project has the potential for large-scale bulk tonnage mining.

“It is expected that high-grade veins may also exist within these large-scale targets at Black Canyon and Fourth of July as demonstrated by previous drilling by PolarX and grab samples from historical artisanal workings at both projects.”

The $30m capped stock is down 15% year-to-date. It had $1.7m in the bank at the end of March.

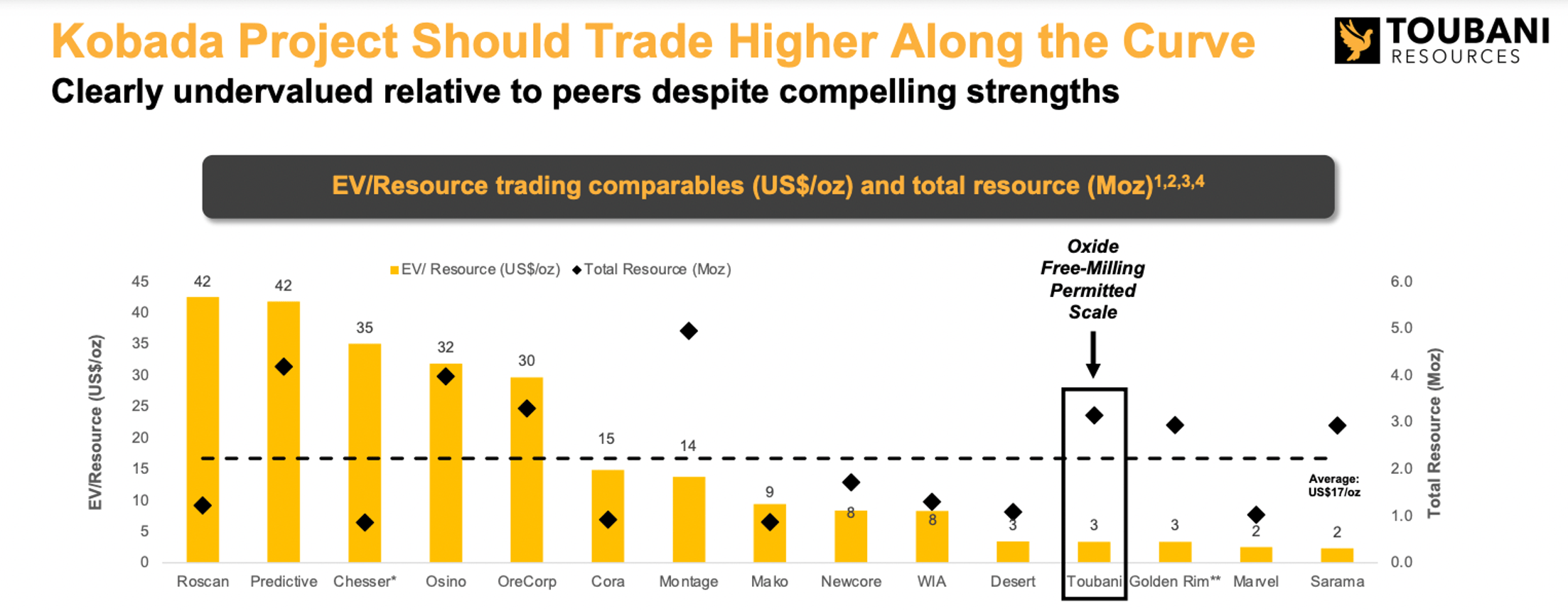

TOUBANI RESOURCES (ASX:TRE)

The Canadian explorer jumped ship to the ASX late November last year with the advanced 3.1Moz Kobada gold project in Mali.

This 4.5km-long resource ticks some important boxes; it is shallow, oxide dominant (softer ore), free-milling and potentially just one of multiple discoveries to be made at the project.

With ~$110m already spent on exploration and studies no significant resource drill-out programs are required ahead of a final investment decision, pencilled in for 1H 2025.

TRE is currently updating a 2021 feasibility study which outlined a +100,000oz per annum operation at US$972/oz AISC over the first 10 years, delivering a pre-tax NPV of $US506m and an IRR of 45%.

NPV and IRR are a measure of a project’s potential profitability; the higher they are above zero, the better.

The $15m capped stock is flat year-to-date, and reckons it is undervalued compared to its peers:

It had $2.2m in the bank at the end of March.

IMPACT MINERALS (ASX:IPT)

IPT has defined a large rare earths soil anomaly 10km long and up to 2km wide at the Arkun project in WA’s South West.

The Horseshoe prospect (it looks like a horseshoe on magnetics) “occurs in the contact zone of an intrusion adjacent to a major regional fault, a prime location for REE”, IPT says.

Field checking and rock chip sampling are now required to identify specific drill targets.

“Horseshoe is just one of numerous REE anomalies we have identified in roadside sampling, and so we look forward to further results from infill soil surveys that are underway,” IPT MD Mike Jones says.

“This and other recent discoveries in the region suggest that southwest Western Australia could also become an REE province like the Gascoyne Province and the Albany-Fraser Belt near Esperance.

“We are happy to have such a significant ground-holding in this region.

“We are also interpreting the soil geochemistry results for nickel-copper-PGM and lithium and look forward to announcing those results when completed.”

The $44m capped stock is up 40% year-to-date. It recently raised $4m via placement at 1.2c per share.

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.