Old and busted: tin. New hotness: tin the ‘EV metal’

Picture: Getty Images

The tin market is trying to rebrand itself as ‘the forgotten EV metal’.

It’s a view that gained traction after heavyweight Rio Tinto (ASX:RIO) nominated the base metal as the one most likely to be impacted by new technology, such as electric vehicles, because of its use as an electric contact material.

This study is now used by many explorers and miners to support the ‘tin as a tech metal’ thematic.

Tin is primarily used as a solder component for electronic circuit boards and microchips — which accounts for about half of its global consumption.

It basically holds things together.

But as a battery metal, it’s still a pretty unsexy one compared to something like lithium or cobalt (before things went pear-shaped).

It’s not a big industry, only about three times the size of the cobalt market.

Regardless, tin prices are now above $US21,000 per tonne – up 60 per cent over the past 3 years.

Visible tin stocks are very, very low, and the consensus is that there’s a real supply issue going forward — regardless of the EV story.

And for Australian miners and explorers, the exchange rate is their friend; that $US21,000/t works out to be about $30,000/t in local currency.

Good prices and a positive outlook has prompted a number of explorers to dust off their Australian projects.

There are about 41 tin projects in Australia at various stages of exploration, development and production.

- Subscribe to our daily newsletter

- Join our small cap Facebook group

- Follow us on Facebook or Twitter

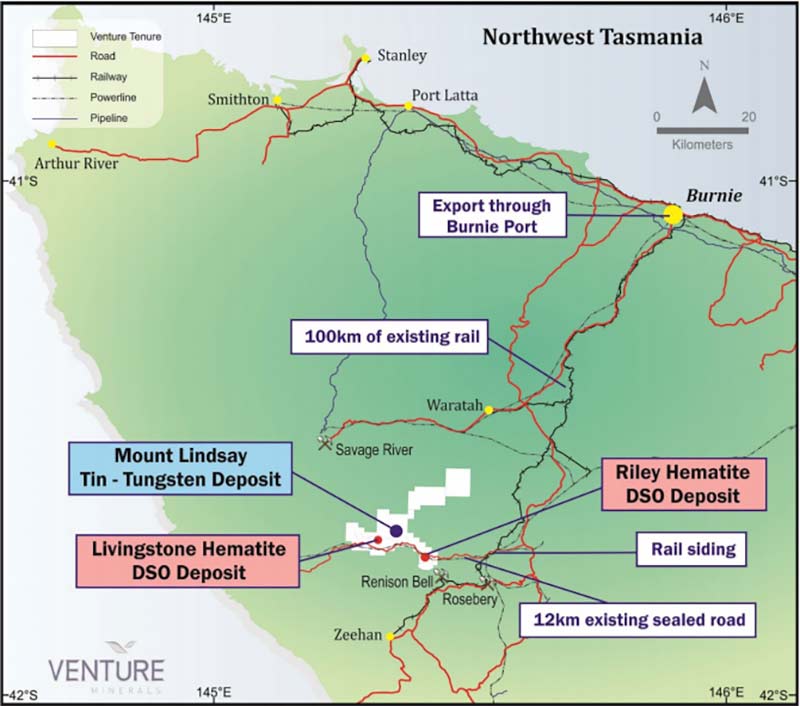

Venture Minerals (ASX:VMS) wants its Mt Lindsay project in Tasmania to be one of the next off the starting block.

Venture mothballed its advanced Mt Lindsay open pit project when tin prices plummeted earlier in the decade.

But last year, in response to high demand from the fast-growing EV market, the company kicked off a scoping study on the high-grade part of the tin and tungsten resource.

Managing director Andrew Radonjic says tin might not be sexy (yet) but “steady wins the race”.

“Tin probably hasn’t been as volatile as those metals [lithium cobalt],” he told Stockhead.

“[And] the Australian dollar has been a good hedge. Our neighbours Metals X are making [good money] at the Renison tin mine.

“Their cash costs are probably less than $15,000 per tonne at prices of $30,000/ tonne.”

There aren’t any major global miners playing in the space either, and a lot of production comes from ‘unethical’ sources in third world jurisdictions.

Mr Radonjic says there’s a lot of project lenders out there today who are looking for ethically, responsibly produced tin.

It’s becoming more and more prevalent,” he says.

“I’m hearing it more and more.”

“For [those projects] you need to go to first class jurisdictions like Australia and Canada.”

This underground scoping study is due for release in the March quarter this year.

Because the company is leveraging off the work done previously it can get these studies done for a modest amount.

“Importantly we can get the capex down to something like $50 million,” Mr Radonjic says.

“That’s fundable.”

It also helps that tungsten prices have also increased by 60 per cent since February 2016.

And here’s a potential bonus: Venture has a fully permitted iron ore mine just down the road, called Riley, that can recommence operations very quickly.

It’s not big, but since last December, the 62% iron ore price has risen almost 40 per cent in US dollar terms, making the project a potential cashbox for Mt Lindsay development.

Mr Radonjic expects things to move very rapidly post-scoping study.

“We will need to do some more metallurgical test work on the adjusted circuit, but it will go to feasibility very quickly because of that all the work we have done previously.”

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.