Near term miner Antilles to boost profits, reduce risk with gold doré production

Antilles to boost profits, reduce risk with gold doré production.

- Antilles to expand La Demajagua mine development to produce gold doré from its gold-arsenopyrite concentrate

- Move will increase profitability while addressing difficult market for arsenic-rich gold concentrate

- Experienced Chinese roaster operator sought to provide capital for expansion

- Focus remains on bringing Nueva Sabana gold-copper mine into production by Q2 2025

Antilles has expanded the scope of its proposed La Demajagua gold project in Cuba to include the production of gold doré to increase profitability and de-risk mine development.

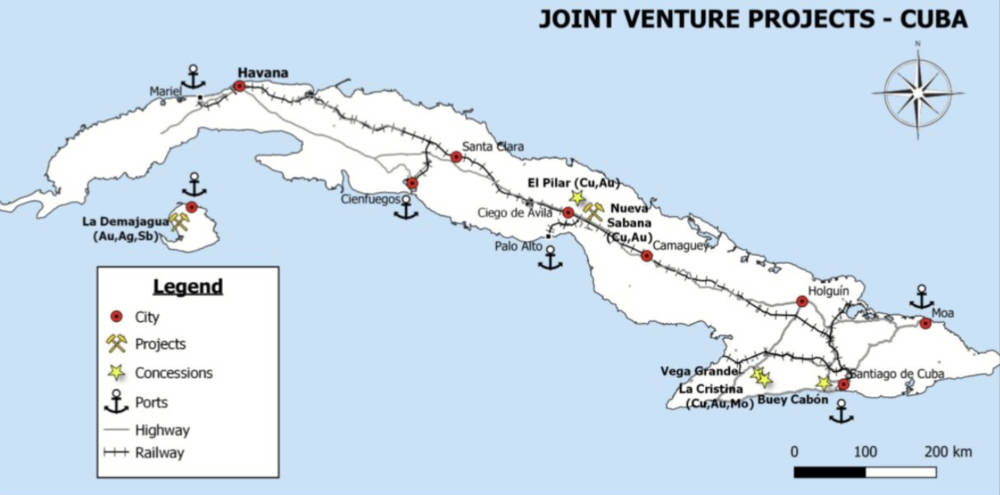

La Demajagua – Antilles Gold (ASX:AAU) second mining development project – is a proposed open pit mine on the Isle of Youth in southwest Cuba.

It has a current resource of 905,000oz of gold equivalent for the first stage open pit. It was originally intended to produce about 80,000oz of gold equivalent per annum in ~50,000tpa of a 32g/t gold arsenopyrite concentrate and ~6000tpa of concentrate containing 49g/t gold, 46% antimony, and 2,200g/t silver.

This was expected to deliver net present value (NPV) and internal rate of return, both measures of a project’s profitability, of US$195.6m and 27.9% respectively from life of mine (LoM) revenue of US$880m using a conservative gold price of US$1,800/oz.

Along with the proposed Nueva Sabana mine, which is based on the El Pilar gold-copper oxide deposit that overlays a large copper-gold porphyry system in central Cuba, the resulting cash flow will be partly invested into exploration of major copper targets.

These include the El Pilar copper-gold porphyry system and three highly prospective properties within the Sierra Maestra copper belt in southeast Cuba.

Locations of Antilles’ joint venture projects in Cuba. Pic: Supplied (AAU).

From concentrate to doré

Antilles and its equal joint venture partner – Cuban government mining company GeoMinera – have now decided to expand La Demajagua to produce gold doré from the open pit mine’s gold-arsenopyrite concentrate.

Since pre-development activities for the project started, sales to China have become uneconomic as a consequence of new taxes being imposed on imported concentrates with high arsenic content, and Russian POX plants are no longer accessible due to sanctions.

Additionally, the commodities trader that the joint venture company, Minera La Victoria, has been dealing with advised recently that due to reducing availability of excess processing capacity in plants outside of China, it cannot commit to purchasing 100% of the mine’s output of gold-arsenopyrite concentrate.

To address the difficult market for gold-arsenopyrite concentrate, MLV plans to build a concentrate processing facility at the mine site based on a 75,000tpa two-stage fluid-bed roaster that will oxidise 50,000tpa of La Demajagua gold-arsenopyrite concentrate, and 25,000tpa of gold pyrite concentrate imported from regional mines.

An associated 100,000tpa CIL circuit will allow production of additional doré from 25,000tpa of oxide gold ore from the La Demajagua deposit that can be mined separately from the predominantly sulphide ore.

This plan to produce gold doré will be established by the DFS for the expanded project, and is expected to be around 125,000ozpa for the nine-year open pit LoM and could potentially continue with underground operations to follow for a similar period.

The ~6,000tpa of gold antimony concentrate that will also be produced by the mine is readily saleable.

Higher profitability to offset diluted shareholdings

The JV has started negotiations with a Chinese engineering group with extensive experience in designing and constructing roasters in order to obtain a turnkey proposal for the proposed plant.

While metallurgical testing is required prior to finalising this proposal, the capital cost of the proposed plant and CIL circuit is expected to be between US$40m and US$45m.

To meet this additional expenditure, diversified Chinese financial services and investment management group Richlink Capital has been engaged to assist MLV arrange for a suitable Chinese company with experience in operating roasters, to provide capital by subscribing for 30% to 40% of its shares at a price that reflects the market value of its projects.

Should this proposed investment proceed, both Antilles and GeoMinera will have their shareholdings diluted though the increased NPV for the expanded project is expected to maintain, or even improve each partner’s share of NPV.

Construction of the expanded La Demajagua project is also expected to be delayed though it is expected to be fully permitted and development-ready by the end of 2024.

“The concept of adding the production of gold doré to the La Demajagua project will not only increase its profitability but will de-risk the mine development in a market where it is becoming increasingly difficult to place all of its annual production of gold arsenopyrite concentrate through reliable, long term offtake arrangements,” executive chairman Brian Johnson said.

“The expanded project will increase the financial returns for the project and should be attractive to potential investors in Minera La Victoria.

“It is anticipated that the additional capital that will be sought by MLV from an Investor for a one third shareholding would be in the order of US$50 million (~A$75 million) based on a large discount to the NPV of MLV’s assets.

“The amount ultimately negotiated for any investment will provide an indication of the market value of Antilles Gold’s diluted shareholding in MLV.”

He added that in the interim, the JV will focus on commencing construction of Nueva Sabana with commissioning targeted for Q2 2025.

For more on Antilles Gold (ASX:AAU) , listen below to hear Christian Grainger, exploration director at Antilles Gold chat with Barry FitzGerald about their projects in Cuba.

This article was developed in collaboration with Antilles Gold, a Stockhead advertiser at the time of publishing.

This article does not constitute financial product advice. You should consider obtaining independent advice before making any financial decisions.

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.