Monsters of Rock: Gold equities baffle against rising bullion as reporting season begins

Even our super intelligent space gorilla is baffled by the valuation of gold equities. Pic: Getty Images

-

- Gold equities have struggled to keep up with rising gold prices, creating a potential valuation gap for investors

- But RBC warns gold prices could moderate in the months ahead

- Spartan surges on rank day for ASX metals and mining sector after hitting high-grade gold at Pepper

RBC’s Alex Barkley says continued strong spot prices will be key to keeping the value proposition in the Aussie gold sector, which is still trailing a stunning run in bullion prices fuelled by war and slowing inflation.

Australian dollar gold prices are up over $3725/oz, a 20%+ increase YTD, and in touching distance of US$2400/oz.

Barkley says gold equities in RBC’s coverage universe are up only 8%.

That’s rough buddy.

Some of that is stock specific. The development of the McPhillamy’s project in NSW has been removed from RBC’s Regis Resources (ASX:RRL) forecasts after a capex increase that was nothing short of disastrous.

But otherwise gold prices should support stronger outcomes despite the impact of wet weather on operations in the March quarter (already largely flagged by Gold Road (ASX:GOR), Northern Star (ASX:NST), Capricorn (ASX:CMM) and more.)

“We find select value on our base case forecasts, and more broad-based upside should the higher spot price be maintained. Key forecasts changes include removing McPhillamy’s from RRL forecasts,” Barkley said.

“This leaves a simplified, unhedged and high-earning WA miner with an 18% FY25E FCF yield. For Bellevue Gold (ASX:BGL) we incorporate an operating multiple into our valuation. Despite lifting near-term costs we still find an 11% FY25E FCF yield.

“RRL and BGL are both rated Outperform, as are high quality NST, which remains the go-to ASX gold exposure, and De Grey Mining (ASX:DEG), which has near-term news upside and long-term gold leverage.”

Spot prices transform miners’ valuations

By and large, how you feel about the value proposition of gold producers, who have seen rising costs eat margins in recent years, depends on how bullish you are on gold prices.

RBC has upped its Q2 forecast by 8% to US$2150/oz, with Q4 unchanged at US$2075/oz and US$2140/oz in 2025.

“Support for gold has come from physical demand, central bank buying and geopolitical risks,” Barkley said.

“However, demand elasticity and any transition of geopolitical risks could ease these demand factors.

“In combination with increasingly hawkish rate expectations; we see near-term potential for gold to lose some of its recent gains.”

Barkley thinks a degree of skepticism around gold prices is baked into equity valuations. At RBC’s long-run price of US$1700/oz ($2300/oz at a 75c exchange rate), its valuations are priced at 1.2x NAV.

At spot, however, those same stocks are priced at a cheap 0.7x.

“Using our constructive FY25 gold price of US$2030/oz (A$3110/oz) we find decent value among our producing Outperform-rated stocks,” Barkley said.

“We forecast FY25 EV/EBITDAs for NST 6.2x (3yr av. 7.4x), RRL 3.6x (3yr av. 4.0x), and BGL 5.5x despite its only entering production and having a low ongoing capex requirement.

“We expect reasonable FY25E cost control and generally modest capex to present some strong FCF yields in our coverage: with RRL 18%, Ramelius (ASX:RMS) 15% and BGL 11%.”

Spartan delivers monster hit

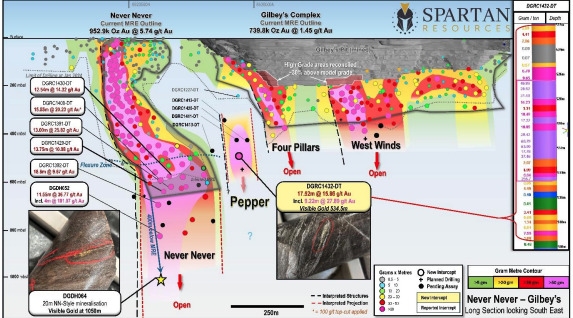

Speaking of gold, the Pepper discovery at Spartan Resources’ (ASX:SPR) Dalgaranga gold project looks set to pour salt in the wounds of the previous owners of the ground.

The hit features some 17.52m at 15.86g/t gold from 522m deep including a 9.22m intercept at 27.89g/t.

It’s just 90m south and along strike from the 952,000oz Never Never deposit, the emergence of which turned Spartan into a $500 million-plus stock last year.

Up almost 8% as of 2.45pm AEST, Spartan is now capped at almost $600m. It’s an incredible turnaround given the company collapsed once and needed a recap early last year to invest in the Never Never discovery once it was found.

Incredibly, it was just a stone’s throw from a 2.5Mtpa processing plant that had been milling low-grade mullock previously.

Pepper appears to be an entirely distinct but also high-grade shoot, and comes after drilling last week showed mineralisation at Never Never likely continued for 400m below the high-grade orebody.

Spartan’s boss Simon Lawson said the positioning of Pepper was such that a future mining scenario would likely see a box cut from the previously mined Gilbey’s open pit straight by Pepper on the way to Never Never, making it a favourable position in relation to future drill drives and declines.

LME rules pump … nickel?

A broad sell-off hammered the ASX today following a Wall Street wipeout overnight, with only a handful of miners feeling the love of investors.

Copper miner Sandfire Resources (ASX:SFR) was up 1.10% at the closing bell today, AEST.

It came after the LME and Comex both announced plans to cancel warehouse purchases of Russian metal, reversing an LME decision from last year.

The reaction to sanctions could reduce available tonnes of copper, nickel and aluminium, all of which count Russia as a major producer.

Nickel prices hit a recent high of US$18,364/t overnight, with zinc up 1% to US$2735.50/t.

The materials sector fell 2.03% as of closing time AEST, with the big iron ore miners all crunched.

Today’s Best Miners

Sandfire Resources (ASX:SFR) (copper) +0.66%

Spartan Resources (ASX:SPR) (gold) +9%

Yancoal (ASX:YAL) (coal) +2%

Silver Lake Resources (ASX:SLR) (gold) +0.2%

Today’s Worst Miners

Resolute Mining (ASX:RSG) (gold) -10.2%

Deep Yellow (ASX:DYL) (uranium) -8.8%

Boss Energy (ASX:BOE) (uranium) -5.8%

Gold Road Resources (ASX:GOR) (gold) -5.4%

Monstars share prices today

ASX 300 Metals and Minings Index today

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.