Monsters of Rock: Chinese steel output falls to 3.5 year lows, weighing on ASX miners

Pic: Monty Rakusen/Image Source via Getty Images.

China’s National Bureau of Statistics released its October statistics yesterday and industrial figures were better than expected.

Industrial growth rebounded as energy shortages eased, Capital Economics senior China economist Julian Evans-Pritchard said, with retail sales growth up from 4.4% year on year to 4.9% year on year and industrial production growth up for the first time in eight months from 3.1%YoY to 3.5% YoY.

But looking under the bonnet the message was less rosy for the big iron ore miners.

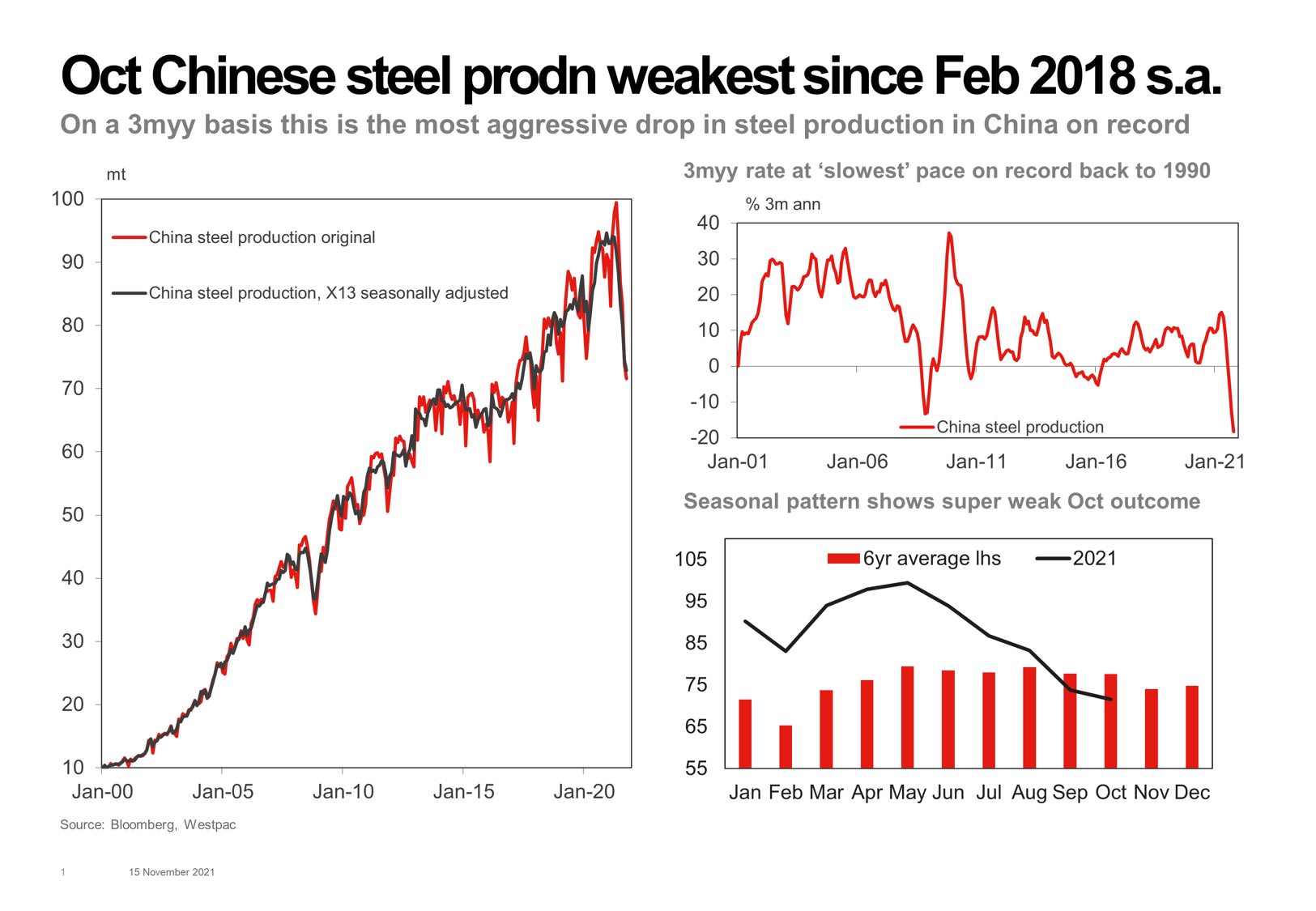

Crude steel production fell to its lowest level in October since February 2018.

Steel mills in the Asian nation, which accounts for well over 50% of the global steel market, slid to 71.5Mt last month, down 23% year on year and far below highs of 99.5Mt produced in May.

Those statistics dragged on iron ore futures – prices were already below US$90/t at the start of trade – with the big miners slipping into the red after an indifferent start to the trading day.

BHP (ASX:BHP) was off 0.64%, with Rio Tinto (ASX:RIO) down 0.4%.

Champion Iron (ASX:CIA) was flat while Fortescue Metals Group (ASX:FMG) came back to a 1.21% rise having climbed higher in morning trade.

Mineral Resources (ASX:MIN), which also mines lithium and provides mining services alongside its iron ore exports, was up 3.34%.

Monster share prices today:

Property sector could weigh on metal producers

China has sought to enforce steel restrictions on environmental grounds, cutting the industry’s outputs at a rate not generally thought possible by market watchers.

But we also have a sneaking suspicion the country, unable to wean itself off the iron ore mainlined into its veins from its trade frenemy in Australia the same way it has with things like coal and lobster, was hoping to take a (successful) bite out of historically high iron ore prices.

It should be noted that at current prices of ~US$90/t majors like BHP and Rio, who have extremely low costs in the teens for each tonne of iron ore sold, are still making decent bank.

It remains to be seen what policies China’s Government will have around steel output beyond 2021.

A broader concern is the state of the Chinese property market, which accounts for about 30% of steel demand in China and remains moribund despite Evergrande pulling a Houdini act to weasel its way out of a default situation last week.

“Property investment cooled further, with real estate developers cutting back on new housing starts last month,” Capital Economics’ Evans-Pritchard said.

“Property sales also softened and are now down 21.6% y/y on a monthly basis. This is pulling down prices for new homes, which fell by 0.3% m/m, its largest contraction since February 2015.”

Related Topics

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.