Major growth spurt: Europe’s biggest lithium resource just supersized

Vulcan stands tall after upgrading resources at its Zero Carbon Lithium project. Pic: via Getty Images.

- Zero Carbon Lithium’s standing as Europe’s largest lithium resource has been bolstered

- Resource increased from 26.6Mt LCE to 27.7Mt LCE

- Vulcan on track to complete key bridging study and field development plan by November

- Studies will pave the way for project financing phase to begin

Vulcan has extended its lead over other lithium projects in Europe after upgrading resources at its Zero Carbon Lithium project by more than 4% to 27.7Mt LCE.

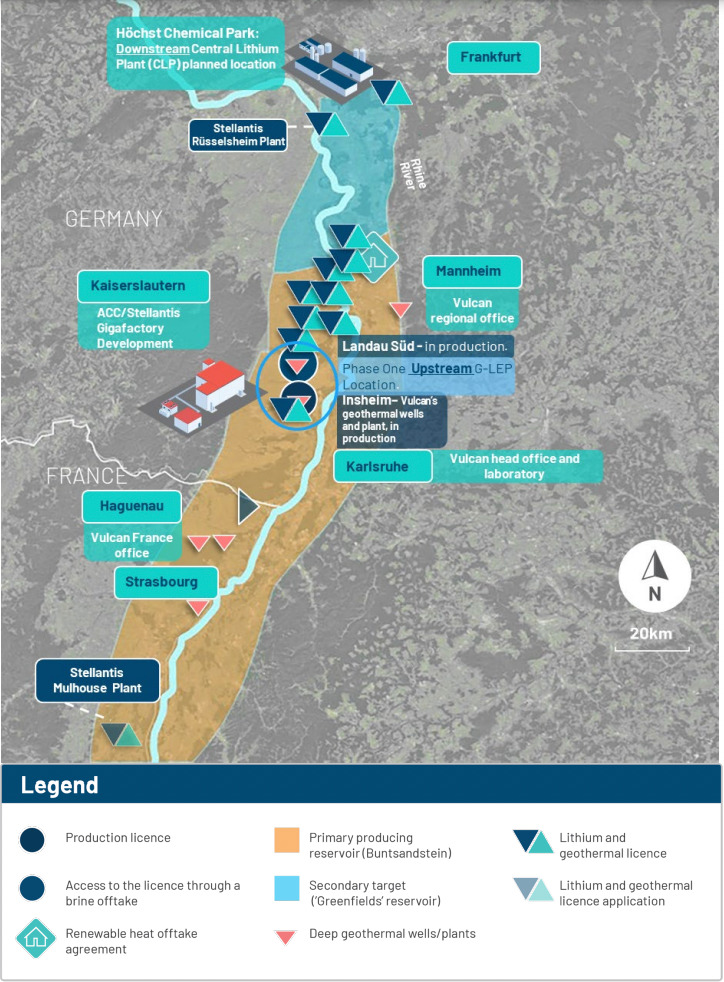

The unique Zero Carbon Lithium project in Germany’s Upper Rhine Valley will be the world’s first producer of both renewable geothermal energy and enough lithium hydroxide for 1 million electric vehicles per year.

Both products will be sourced from the same deep, hot brines, which separate it from other lithium brine projects.

Vulcan Energy Resources (ASX:VUL) has already lined up offtake agreements including one with European automotive giant Stellantis – the owner of the Opel, Peugeot, Citroen, Fiat and Chrysler car brands, whish is also the company’s second largest shareholder.

Additional offtake agreements have also been reached with some of the largest battery, cathode and EV producers in Europe, such as Volkswagen, LG Energy, Umicore and Renault.

Earlier this month, the company acquired the Luftbrücke licence in Frankfurt which increases the total Zero Carbon Lithium project area by 13% to 1,790km2, secures the ground around the planned Central Lithium Electrolysis Optimisation Plant (CLEOP) and gives it a new set of potential industrial customers.

Vulcan is currently on track to become ‘finance-ready’ – or ready to pursue debt financing in earnest – in November this year once the key Bridging Study and environmental and social impact assessment are completed.

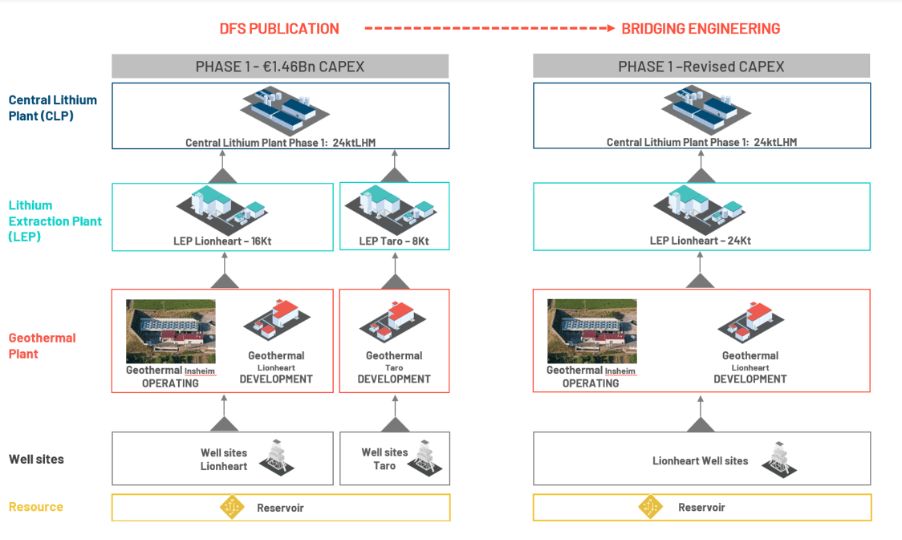

Larger resource reduces upstream risk for Phase 1

Vulcan has now incorporated new sub-surface work to increase the Zero Carbon Lithium resource in the Phase 1 Lionheart area – already Europe’s largest – up from 26.6Mt LCE (lithium carbonate equivalent) at 174mg/l to 27.7Mt LCE at 175mg/l.

High confidence Measured and Indicated resources in the key Upper Rhine Valley Brine Field (URVBF) have also increased by more than 11% to 11.2Mt LCE at 179mg/l, which will feed into the ongoing Bridging Study.

The Bridging Study has already identified several key value improvements that were not identified in the Definitive Feasibility Study from February.

These include further economies of scale through reduction of the planned two lithium extraction plants and two geothermal power plants to a single central extraction plant and power plant with the same capacity.

It will also mature current key deliverables and engineering definition to target a Class 2 estimate and Level 3 schedule, which will be further validated by key potential EPCM contractors for the Phase One project execution.

This article was developed in collaboration with Vulcan Energy, a Stockhead advertiser at the time of publishing.

This article does not constitute financial product advice. You should consider obtaining independent advice before making any financial decisions.

Related Topics

Related Stories

UNLOCK INSIGHTS

Discover the untold stories of emerging ASX stocks.

Daily news and expert analysis, it's free to subscribe.

By proceeding, you confirm you understand that we handle personal information in accordance with our Privacy Policy.